.png)

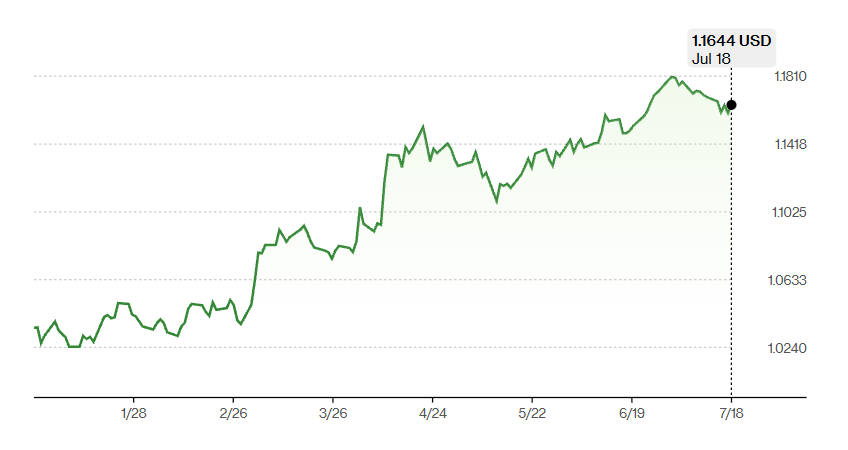

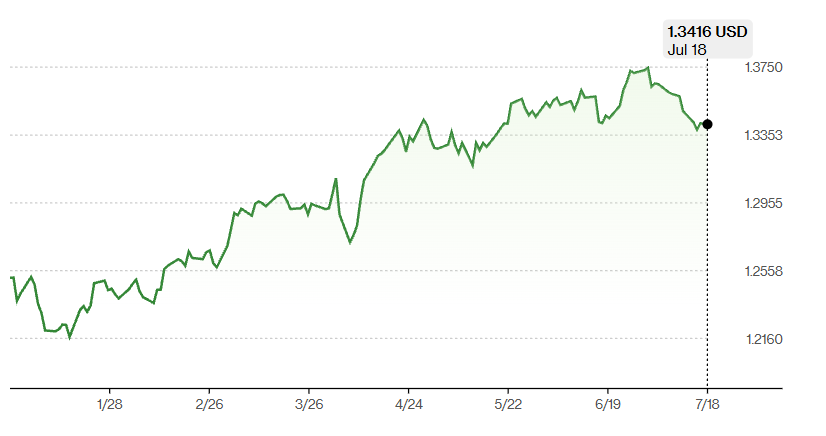

On January 3rd 2025, USD surged to a two-year high against EUR and an 8-month high against GBP. This was off the back of strong US jobs market data, which added to investor confidence from resilient growth statistics and hopes for Fed rate cuts. However, this strength was to be short lived - since then, GBP/USD has risen by 8.9%, EUR/USD by 13.5% YTD. This clearly suggests underlying issues that the US economy faces and could mean the start of a shift away from the US market leadership of the last 130 years, with there even being discussion over whether it should remain as the world’s reserve currency.

A multitude of factors have caused highly volatile Foreign Exchange markets over the previous 6 months. From tariffs, to wars and uncertainty over Fed rate cuts, the Bond and FX markets have portrayed this most evidently. This has led to expectations that confidence in the US cannot be sustained as it has been in previous years, which have seen up to $26 trillion of foreign ownership in US assets. Capital outflows from the US do not help falling USD, whilst promised investment and fiscal packages have strengthened EUR.

This report aims to address some of the issues affecting the dollar, especially in comparison to other global currencies, and assess possible outcomes.

EUR/USD has moved in one direction this year, with EUR making large gains of 13.5% YTD. This is due to multiple factors, including interest rate expectations in the two regions alongside falling business and investor confidence within the US economy.

Interest Rates:

EUR/USD has experienced a large amount of volatility due to interest rate expectations, uncertainty over the US economy coupled with stronger Eurozone data. These have improved the outlook for the Euro, and consequently Europe, in the coming months despite the constant threat of tariffs from Trump.

The ECB has been cautious about cutting interest rates due to fears over sticky inflation. The inflation data for the Euro area in June 2025 is expected to be 2%, which indicates an overall downward trend towards the ECB’s target of 2%. This bodes well and suggests that the two cuts which were made in 2025, each of 25 bps, have worked as the rate at which cuts occur has slowed down after aggressive cutting (eight cuts since June 2024).

Due to this strong data, there has been more bond issuance, with €90bn in the H1 2025 and €70bn more set for the second half, driving up demand for EUR as investors look to buy new bonds. I believe this has been a key factor in the recent strength of the Euro and will help to continue this rally through 2025, as tensions ease across the world and investors are looking to take on more risk in the hopes of higher returns.

Simultaneously, at the start of 2025 the Fed signalled they were looking to cut interest rates twice in the year. Since then, Trump has attempted to force the Fed into cutting rates at a quicker pace and by larger amounts to help combat the rising inflation the US is facing due to his tariffs. However, the Fed isn’t backing down and consequently, cuts previously priced into the markets are not being realised. This means that US yields are rising, as bonds reflect that rates will be higher for longer. Coupled with US bonds often being regarded as a ‘safe haven’ for investors, bonds have seen a rise in price as investors rush to seek stable investments amid the tariff uncertainty. This has led to a yield gap between the US and German 10-year bonds, for example. which is currently sat at 1.77% in favour of EUR. (The US/German bond spread is often a good indicator of Europe as a whole, as Germany is the dominant economy within the Eurozone and so acts as an insight into how the market is pricing the US versus Europe.)

This may lead to less investment in more risky assets in the US and more into safer options such as Gold or safer bonds. This will affect USD as there will be less demand for dollars due to no new investment opportunities to produce high yields, in comparison with riskier European assets.

On the other hand, US yields are continuing to rise, which may make them more attractive in comparison to European bonds. This, coupled with an already weakened dollar, may lead to more attractive investments for European investors as it is now cheaper and more accessible to enter into longer-term, higher yield bonds before rate cuts reduce future returns. This is because they will be able to lock in that higher rate at a lower cost, should rates not fall. In the very strong likelihood that they do change over the next few months, those 10–30-year bonds can be sold at a higher price anyway - a win-win.

GBP has rallied against USD, 7.2% YTD. Despite headline inflation rising to 3.6% in mid-2025, up from 3.0% in January of this year, the Bank of England is planning, and has already executed, rate cuts as core inflation eases, growth slows, and global monetary policy is turning dovish. However, sticky services inflation and resilient wage growth mean the BoE will cut rates very gradually, likely only once or twice by year-end adding to the two cuts that have already occurred this year.

With two Fed rate cuts expected, but by no means guaranteed, the UK has seen a narrowing of the yield gap this year, which has almost completely been eliminated, creating a vastly different scenario in comparison to the Euro.

On 2-year gilts, there is a 0.0% UK–US spread, and only a -0.1% spread on 10-years. With the UK and US yields now virtually identical, the traditional yield advantage of USD assets has disappeared, which may benefit the UK in a couple of ways:

Firstly, it increases trade competitiveness as businesses face less volatile FX swings. This is thanks to a more stable currency, due to fewer speculative hot money flows, helping UK businesses. I believe that this will prove extremely beneficial for the UK as the Government attempts to restart growth within the economy, as rates are being cut and FX stabilises. This will fill businesses with confidence to invest in new ventures and take on risks which they may not have been willing to take on a couple of years ago. This will further increase the strength of the Pound as there will be greater demand for GBP for foreign countries to import British goods and services.

Secondly, investors can now focus more on credit quality, liquidity, and inflation risk. These all benefit the UK as Treasury bonds were recently downgraded from AAA to AA1, which may begin to cast doubt over the reliability of US Treasuries, thus, investors may look to mitigate risk and diversify their bonds. With the threat of inflation within the US, Treasury bonds may become less attractive and coupled with the lack of a premium over Gilts, there is now less of an attraction to Treasuries, which further reduces demand for USD, weakening it. However, I do not think this may have as large an impact as others are predicting. This is because the US is still a global dominant force with Treasuries maintaining their position as much lower risk than other bonds on the market.

A third effect, which may be felt by both sides, is the ability of Central Banks to act in a more aggressive way, should they wish to. This is because there is no risk over a severe weakening of the currency and allows for rates to be used to tackle other issues without the fear of adverse effects on the currency.

However, there are two sides to yield convergence. While it promotes stability and policy flexibility, it also reduces the incentive for foreign investors to favour either currency, potentially slowing capital inflows. For the UK, this removes pressure on the pound and allows for gradual rate cuts, in the hopes of boosting growth over the next couple of years. For the US, it means Treasuries may need to offer non-yield-related advantages, like safety, to stay attractive.

Conflicts like Israel-Gaza and Russia-Ukraine have also had unavoidable consequences for global markets. These events will have strengthened USD and driven up demand for dollars. This is due to flows into Gold and US Treasuries, which are often seen as a safe haven during times of unrest, due to substantial trust in the US Govt., reserve currency status and high market liquidity. This contrasts with GBP and EUR, which usually struggle during periods of uncertainty and may only benefit after tensions ease.

However, 2025 has changed things.

Falling trust in the US and Trump, due to scepticism about his next moves, has significantly weakened trust in the US. This was reinforced by his threats to pull out of NATO and stop funding the war in Ukraine. Instead of his hoped-for result of European countries rushing to buy US weapons, they turned to Europe and other parts of the world, aided by Germany’s €500 bn fiscal package containing an emphasis on defence industry(a key example is Rheinmetall AG, a German ammunition producer up 204% YTD). This shows how Europe has started to back itself, with the rest of the world following. This has led to increasing inflows into Europe driving up demand for EUR, and in doing so causing outflows from the US.

Even this year, the US has been seen as less of a haven as confidence falls and investors look to hedge risk elsewhere. This is shown in the figure below, where demand for dollars and inflows have fallen significantly, compared to the previous 50 years.

.jpeg)

I believe that there will be a more fundamental shift and re-allocation of portfolios with a greater portion designated for European assets, as the ECB is cutting rates and creating fiscal packages, leading to greater growth within the Eurozone region, thus attracting new investors and inflows.

Overall, I believe that there has been a fundamental shift this year in how the world regards the US and the dollar. It has lost a lot of trust, which is largely due to Trump and his erratic nature with his policies, alongside various wars and events in 2025. This does beg the question of whether the USD will remain as the reserve currency, especially when down 13.5% and 7.2% YTD against the Euro and the Pound, at the time of writing.

Whilst I don’t think these highs will remain and that the Euro and Pound may lose some strength, there is also the case of a new dollar cycle. This could well be another blow that initiates the shift moving the reserve currency away from the US Dollar. Whether that is the Euro or an Eastern power will be heavily contested and is a shift that will occur over the long term,not something that will change overnight. This is due to entrenched deals and investments that limit global liquidity. The US is facing both internal and external issues it must fix, such as inflation, rising debt and a weakening jobs market. Therefore, I would not be surprised to see no rate cuts until towards the end of the year so tariff impacts can fully play out and the Fed has a better understanding of how the markets have reacted, and how best to boost employment.

Consequently, I believe long positions in USD will prove beneficial in the long run, especially as the Fed will eventually cut rates and some stability and order will return to US markets.