.png)

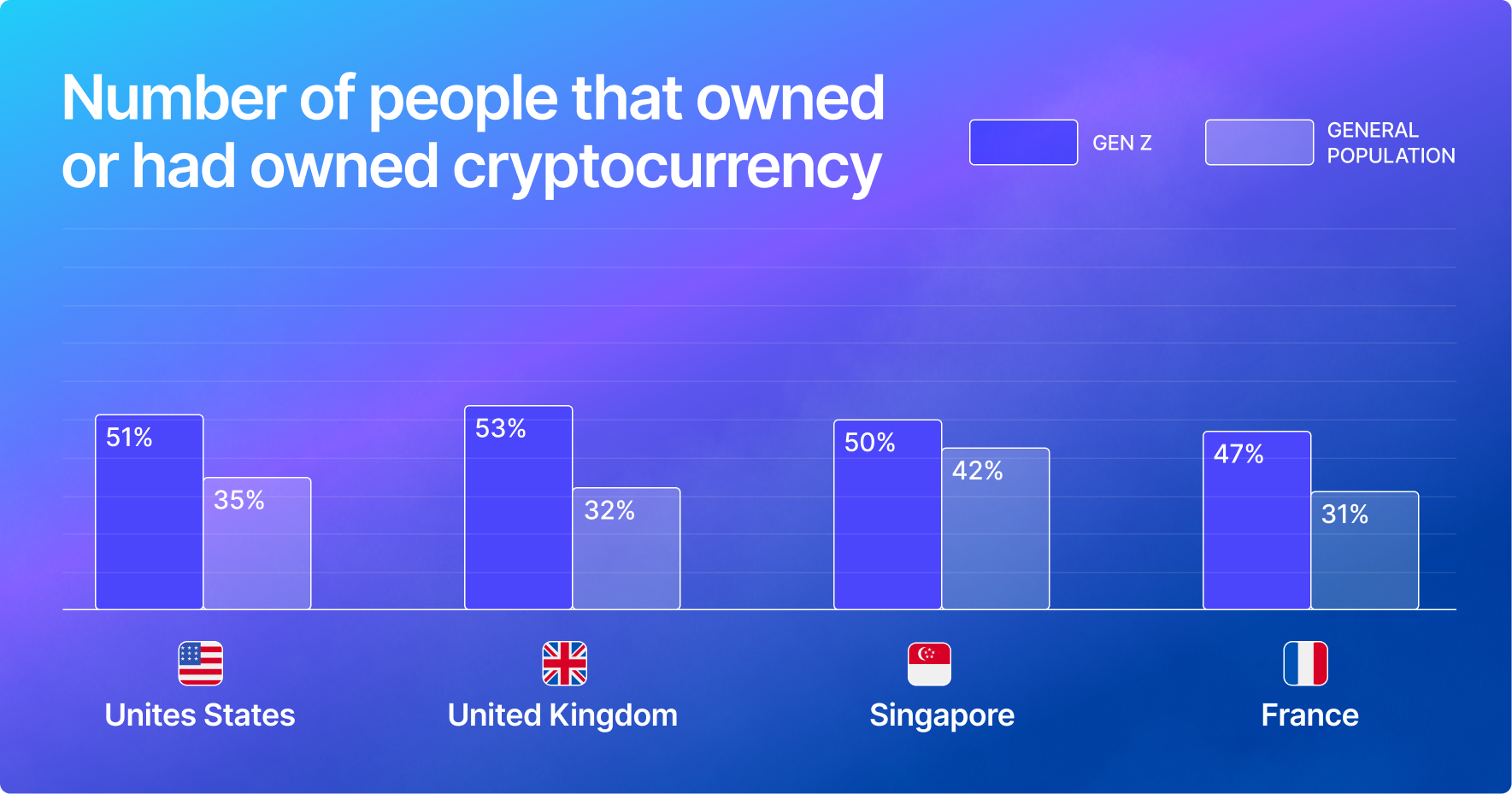

That uncertainty is now being tested by a generational shift in investor behaviour. Gen Z has come of age alongside mobile banking, digital trading platforms, and frictionless online payments. A recent Gemini survey reports that over half (51%) of Gen Z respondents own or have owned cryptocurrency, compared with 35% of the general population. For many, holding a digital asset feels no more unusual than owning a share in a listed company.

Research co-published by the CFA Institute and the FINRA Foundation also shows that Gen Z investors rely heavily on social media, online searches, and family for investment information, far more than on traditional financial professionals. This is thought to explain why this age group tends to invest at such high rates in both crypto and equities.

Clearly, for this generation, digital assets are viewed less as a novelty and more as a familiar extension of modern investing. As Gen Z begins to accumulate meaningful levels of wealth, its expectations are starting to exert pressure on an industry long defined by restraint and incremental change.

Younger clients are approaching wealth management with different expectations from those of previous generations, in particular regarding digital access and transparency. For example, research from Accenture suggests that more than 70% of younger investors expect a “digital-first relationship” with advisers, which includes greater visibility over portfolios and access to a broader range of investment products.

This suggests a clear shift away from the traditional, adviser-led model of wealth management, in which product choice and portfolio construction were largely determined behind closed doors. Advisers now face growing pressure to explain why certain assets are excluded and to offer structured, regulated access where appropriate, rather than blindly following blanket restrictions.

For all the attention surrounding digital assets, most wealth managers remain instinctively cautious. The industry is built around a disciplined, long-term focus on capital preservation, which naturally makes it slow to embrace assets that are volatile, difficult to value, and still vulnerable to changing regulations. From the typical wealth adviser’s point of view, crypto introduces a range of risks that extend beyond price volatility, encompassing everything from client suitability, custody, and key-management concerns, to regulatory uncertainty and even potential reputational damage.

Part of the adviser’s role is also to apply rational judgment on behalf of clients, which may be especially relevant for this generation of investors. Research indicates that younger investors are more willing to take above-average financial risks, with over half of Gen Z investors admitting to having invested solely due to fear of missing out (FOMO). This further explains why many wealth managers may approach crypto-related enthusiasm with a degree of scepticism.

Whilst individual investors may be willing to absorb losses in pursuit of upside, a wealth manager following the same strategy would soon be out of business. Wealth managers are accountable not only for returns, but for the manner in which those returns are generated and the risks taken along the way.

Where individual investors may choose to experiment, advisers operate within far tighter constraints, such as capital-preservation mandates and the risk of client complaints. Therefore, it seems caution reflects less a reluctance to engage with digital assets than a recognition of the obligations that define the profession.

In most wealth management firms, market enthusiasm alone rarely determines what enters a client’s portfolio. In practice, investment committees ask a straightforward set of questions: can the asset be priced reliably, sold when required, explained clearly to clients, and accommodated within existing risk limits? This tends to set a very high bar for inclusion, with assets that fail these tests typically excluded regardless of headline returns.

Historically, crypto has struggled to meet these requirements. Even where firms are open to limited exposure, as we have seen with major names such as Goldman Sachs and Morgan Stanley, allocations remain tightly capped and confined to regulated products. Advisers are not paid simply to chase returns, but primarily to protect capital and manage risk. Meaning that even assets with high upside may be deemed unsuitable if their role in preserving wealth over time cannot be clearly justified. The acceptability of digital assets is less about belief in the asset class itself and more about whether they can be made to fit within rules designed to limit risk.

In recent years, digital assets have entered portfolios through a small number of clearly defined routes, and exposure has been largely confined to the largest and most established tokens. First, regulated spot ETFs and ETPs have become the preferred entry point, typically offering exposure to Bitcoin or, to a lesser extent, Ethereum.

Products launched by firms such as BlackRock and Fidelity allow advisers to offer Bitcoin or Ethereum exposure without the operational risks of direct custody, such as private key management or cybersecurity breaches. These vehicles sit comfortably within many firms’ compliance rules, and are typically treated as modest, satellite allocations, and are often used in response to direct client requests.

Second, some wealth managers also permit access to crypto-linked funds or listed trusts for a limited group of high-net-worth clients. Vehicles such as Grayscale’s bitcoin trust have historically been used as a proxy where ETFs were unavailable, albeit subject to tighter suitability checks and liquidity considerations.

This leaves a narrow set of digital asset products with any realistic prospect of widespread adoption in portfolios. Adoption has come not through conviction, but through compromise, with exposure permitted only where it can be controlled and regulated.

At the same time, client pressure is beginning to broaden the range of digital asset products available to wealth advisers. A surprising number of lesser-known tokens, including Solana, XRP, and even Dogecoin, are available through ETFs, highlighting the extent to which the range of available products has already widened. For now, however, wealth managers continue to draw a clear line between what can be packaged and what is deemed suitable, leaving these products, alongside staking strategies and unregulated altcoins, largely outside client portfolios.

Yet as the composition of advisers’ client bases evolves, so too may the boundaries of what is considered an acceptable long-term investment. The question for the industry is not simply whether crypto and tokenised assets are here to stay, but how long the wealth management industry can afford to keep them at arm’s length.