Markets have always tried to price the future. From interest rate swaps to volatility indices, investors have long relied on financial instruments that translate uncertainty into prices. Prediction markets extend this logic beyond traditional assets by assigning explicit probabilities to real-world outcomes such as elections, policy decisions, and geopolitical events.

Once confined to academic experiments and niche online communities, prediction markets are now attracting attention from professional traders and financial institutions. Several macro-focused desks monitor these markets during periods of political and monetary uncertainty, using them as supplementary signals rather than standalone forecasts (Bloomberg Opinion).

This article examines how prediction markets work, how they are being used across regions, and why Wall Street is increasingly paying attention despite unresolved regulatory and structural challenges.

The core premise of prediction markets is simple but powerful - prices aggregate dispersed information. When individuals with capital disagree about the probability of an outcome, the market price reflects the weighted average of those beliefs.

Early evidence suggested these markets could be surprisingly effective. Studies comparing election prediction markets with polls found that market prices often adjusted faster to new information and were at least as accurate over full election cycles (Financial Times). Despite this performance, adoption remained limited due to low liquidity, fragmented platforms, and unclear legal status.

That dynamic has begun to shift. Over the past five years, platforms have introduced standardised contracts, continuous trading, and clearer settlement rules. These features mirror the structure of derivatives markets rather than betting exchanges. The result has been a perceptual shift: prediction markets increasingly resemble small-scale financial markets rather than speculative side projects.

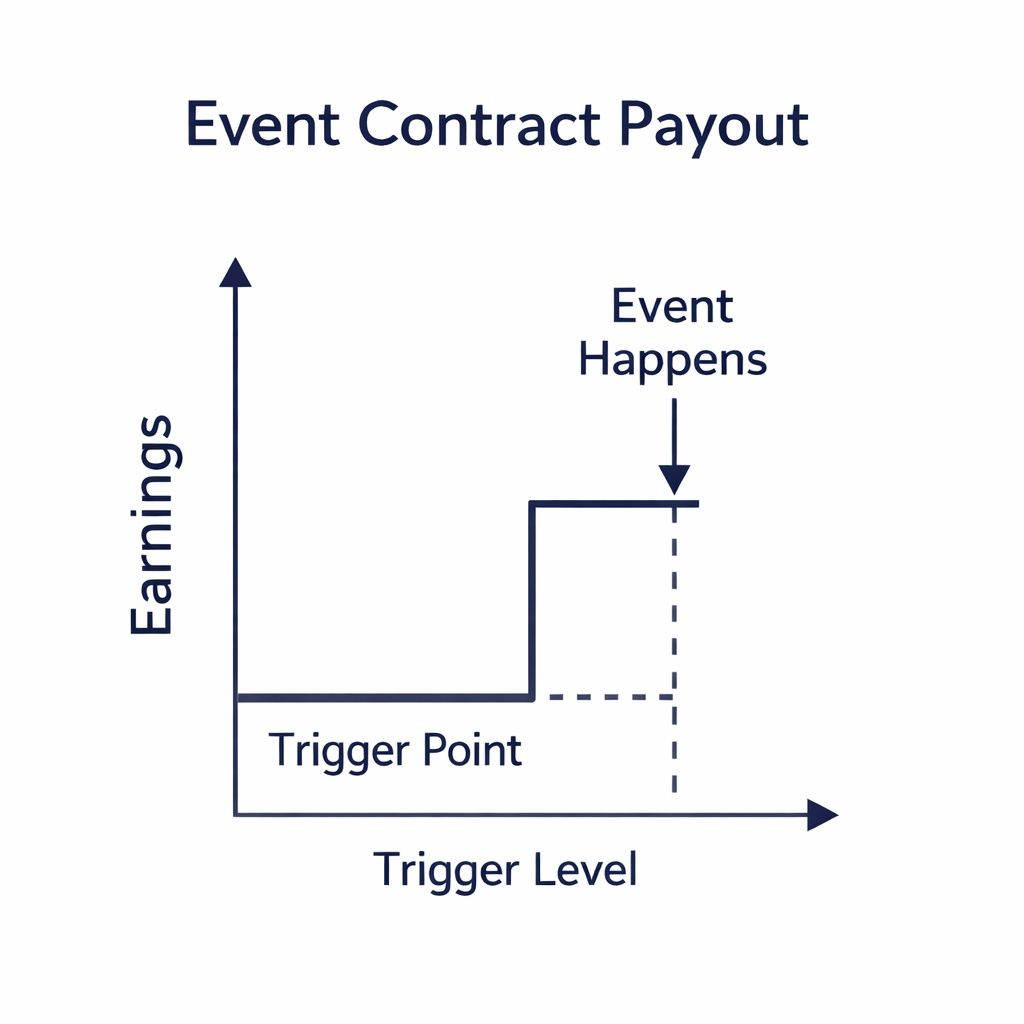

Prediction markets trade binary or range-based contracts that pay out if a specific outcome occurs. A contract trading at 0.62 implies a 62% market-implied probability.

What matters is not the contract itself, but how it trades. Prices update continuously as new information arrives. Liquidity is supplied by active traders and market makers, while volatility spikes around known risk events such as elections, inflation releases, or central bank decisions (Financial Times).

This structure creates familiar incentives. Participants are rewarded for being early and accurate rather than persuasive. For professional traders, this mirrors the logic of macro and event-driven trading, even if the underlying events differ from traditional assets.

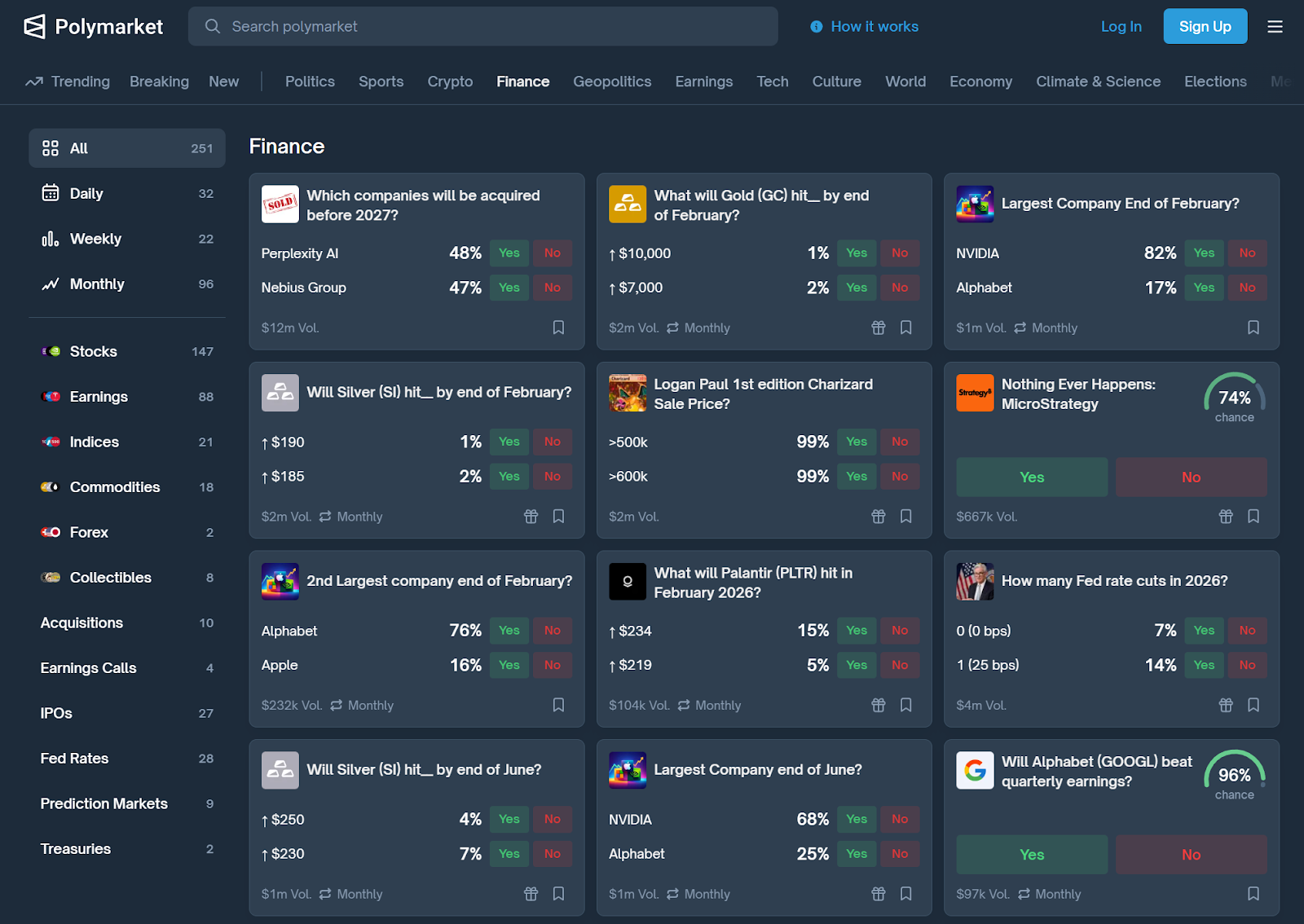

Polymarket has become the most visible global prediction market, particularly for elections and geopolitical events. During the 2024 US election cycle, trading volumes surged into the tens of millions of dollars per day, with prices reacting in real time to court rulings, debates, and polling releases (Bloomberg).

Higher liquidity reduced the influence of individual traders and made prices harder to manipulate. As a result, Polymarket prices were frequently cited by commentators as real-time indicators of political sentiment. However, Polymarket operates offshore and outside US regulatory frameworks. This limits direct institutional participation and introduces legal and compliance risks despite its growing relevance (Financial Times).

Kalshi represents a contrasting model. Regulated in the United States as an event-contracts exchange, it offers markets tied to economic outcomes such as inflation prints and Federal Reserve decisions. Since receiving regulatory approval, trading volumes have grown steadily but remain smaller than offshore platforms, reflecting tighter constraints on contract design (Bloomberg).

Together, these platforms highlight the sector’s central tension. Scale and flexibility often come at the expense of regulatory clarity, while compliance enables legitimacy but limits growth.

Prediction markets are not confined to the United States. Offshore platforms dominate global activity, benefiting from regulatory arbitrage and broader international participation. In parts of Asia and emerging markets, prediction-style contracts increasingly appear within crypto ecosystems tied to sports, political events, and commodity outcomes.

These markets often serve as informal sentiment indicators where traditional financial instruments are limited. However, according to a study, lower liquidity and weaker oversight increase susceptibility to manipulation and sudden price dislocations. For financial institutions, this reinforces a cautious approach. Global markets may offer informational value, but uneven quality and jurisdictional fragmentation make standardisation difficult.

Institutional interest is driven by information rather than speculation. In an environment shaped by geopolitical fragmentation and uncertain monetary policy, traders increasingly seek tools that quantify uncertainty rather than predict direction.

Several hedge funds and macro desks monitor prediction market prices alongside rates markets, options-implied volatility, and FX positioning (Bloomberg). These markets do not replace traditional analysis, but instead provide a complementary signal on collective expectations.

The prevailing stance is observation rather than participation. Institutions are watching how these markets behave under stress before committing capital or infrastructure.

Regulation remains the decisive factor shaping the future of prediction markets. In the United States, the CFTC has adopted a restrictive but clear stance, allowing limited event contracts while blocking broader political markets

In the United Kingdom, prediction markets sit uneasily between gambling regulation and financial market oversight, creating uncertainty around permissible products (UK Gambling Commission regulatory framework). Offshore jurisdictions remain more permissive but face enforcement risk as participation grows.

This fragmented landscape explains why institutional involvement remains limited despite rising interest. Until regulatory classification is resolved, prediction markets are likely to remain adjacent rather than integrated.

Prediction markets are not a replacement for traditional forecasting. They are, however, increasingly difficult to dismiss. Their evolution points to a role as supplementary informational markets that translate uncertainty into prices in real time.

Wall Street’s interest reflects this measured view. Institutions are observing, experimenting, and learning without fully committing. Whether prediction markets become part of mainstream finance will depend less on technology and more on how regulators ultimately define their purpose. In my opinion, they will serve primarily as informational markets that aggregate dispersed geopolitical and policy expectations into a single, continuously updated price signal. While regulatory uncertainty and structural limitations will constrain their full integration into mainstream finance, their ability to quantify uncertainty in real time makes their growing relevance difficult to ignore.