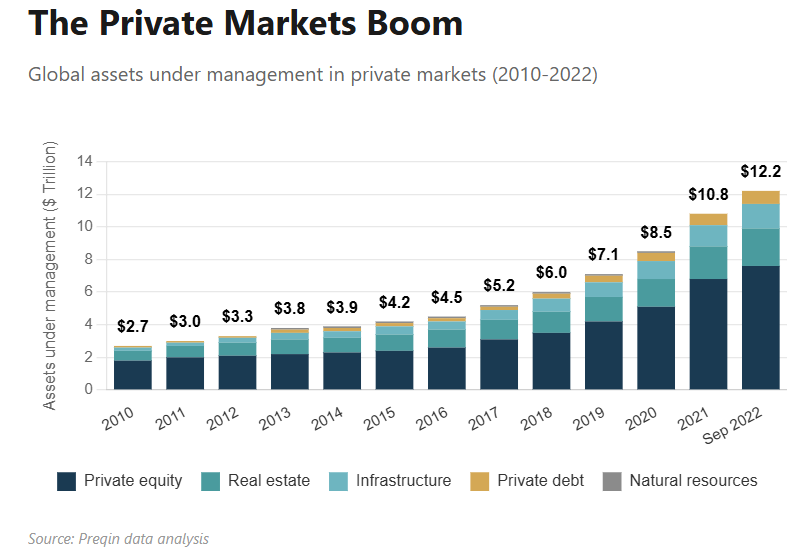

Private markets refer to investments in assets that are not listed on public exchanges. According to Russell Investments, this includes six main asset classes: private credit, private equity, venture capital, private infrastructure, private real estate, and natural resources. Due in large part to their high minimum capital requirements, long investment horizons, and illiquid nature, these assets have traditionally been predominantly within the focus of large institutional investors, including insurers and sovereign wealth funds. However, private markets have seen a great rise in appeal amongst a range of institutional portfolios in recent decades, with Inviva Investors reporting that “56 per cent now allocate ten per cent or more of their portfolios to Private Markets.” This trend has been driven primarily by the illiquidity premium, alongside the diversification benefits and broader opportunity set private assets can provide.

A broader change in the way institutional investors construct their portfolios is reflected in the growing allocation to private markets. Due to their long-term liabilities, pension plans and endowments are in a good position to invest money in illiquid assets in exchange for greater expected returns. Private markets have grown in appeal as a long-term investment option as traditional asset classes have encountered difficulties recently, such as decreased bond yields and increased volatility in public equity markets. Industry research supports this trend. According to surveys, “more than half of institutional investors expect to increase private market allocations over the next two years.” This growing appetite reflects both return considerations and changes in the broader investment landscape. This expansion has also been fuelled by structural shifts in public markets, where fewer businesses are opting to list and many stay private for longer periods of time, thereby reducing the range of opportunities accessible to investors in the public market.

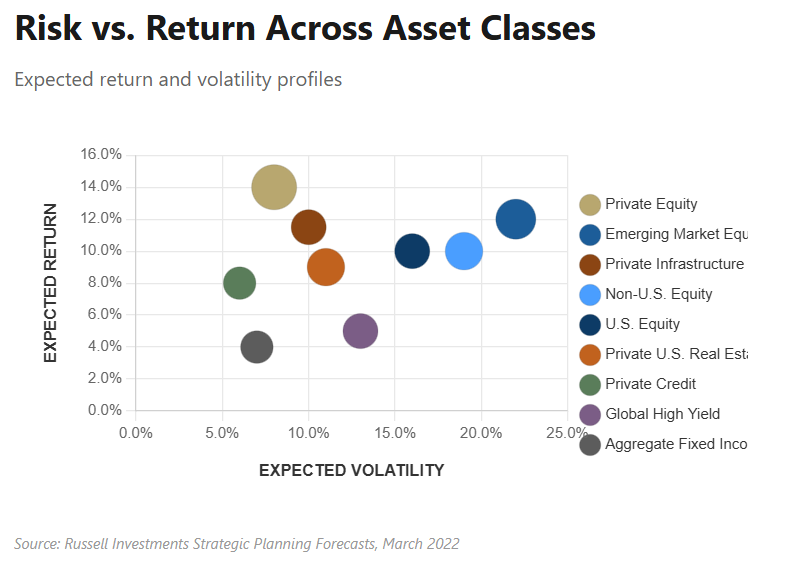

One of the primary reasons institutional investors allocate to private markets is the potential for enhanced long-term returns, largely driven by the illiquidity premium. Compared to similar public market assets, investors who commit capital over longer periods of time are rewarded with higher expected returns. Research published by the Investment Association supports this, finding that “between 1988 - 2022 private equity produced average returns of 15.2%, compared to 7.7% in public equity”. Likewise, private credit offered a similar disparity, with average returns being 9.2% from 2004-2022, compared to “5.3% in European High Yield and 2.2% in Global Investment Grade Bonds.” This return premium serves as justification for long-term investors, including pension plans, to accept illiquidity in order to get greater long-term returns.

Similarly, valuation and transparency are more limited than in public markets, with assets valued infrequently and often based on models. Combined with the wide dispersion of returns, particularly in venture capital, where many firms fail and only a few succeed, this underscores the need for diversification across sectors and strategies.

In conclusion, private markets have become an increasingly important component of institutional portfolios, offering enhanced long‑term returns and meaningful diversification benefits that can stabilise performance during periods of public market volatility. The illiquidity premium, combined with access to a broader opportunity set, provides strong justification for their inclusion, particularly for investors with long‑term liabilities such as pension schemes. Yet, these advantages must be weighed against challenges of illiquidity, valuation opacity, and wide dispersion of outcomes. As such, robust governance, careful liquidity planning, and diversification across strategies are essential to managing these risks. Ultimately, private markets earn their place in portfolios by strengthening resilience and diversifying opportunities over the long term.