A straightforward explanation for market resilience is the continued strong corporate earnings and AI optimism for the future driving market optimism. Earnings per share for S&P 500 companies look strong, and of the 22 that have reported so far, 68% of them have exceeded EPS estimates. The magnificent 7 account for 25% of the S&P 500’s profits and have been the main contributors to the market's rapid growth rates over the past two years. UBS argues that these growth rates are now ‘normalizing’ however the adoption of AI creates optimism for solid growth rates in the future. (UBS, 2025).

The optimism over AI is very substantiated, helping boost productivity across many businesses. AI writes 30% of all code at Microsoft saving them $500 million a year in operating expenses while ServiceNow saved $100 million in hiring costs by automating workflows with GenAI. The integration of AI has now been solidified and productivity is starting to pick up and is certainly a solid driving force of US equities. Bubble or not, there is no arguing that market confidence in tech remains rock solid. Even Trump’s “One Big Beautiful Bill” is an underappreciated tailwind, as research and development spending and favorable tax law changes encourages capital expenditure, driving optimism for business profits in the future (JPMorgan, 2025).

Markets also reflect (to some extent) the economy, and the US economy seems to hold strong. The US is a consumption led economy, with services generating 81% of GDP and 69% of consumer consumption. An event which contracts service consumption is very difficult and has only been done twice in that past two decades in 2008 and 2020. Macroeconomic indicators remain strong with unemployment consistently low at 4.2% and inflation relatively tame at 2.7%. Households are getting stronger: debt to net worth is near all-time lows, 50% below 2008. These indicators only forecast higher earnings by companies due to strong consumption and investment – fueling an already optimistic market (UBS, 2025).

But wait, what about Trump’s tariffs?

Unlike tariffs in 2017 where consumers bore 80-90% of the cost, US companies are now absorbing some of the costs to maintain market share, due to higher margins, meaning tariffs are likely to only burden consumers by a third. Furthermore, companies are remaining profitable; 78% of companies exceeded EPS (earnings per share) expectations in Q1 2025 and General Motors (after reporting a $1.1bn hit) exceeded estimates for EPS due to higher revenues due to improved international profits (JPMorgan, 2025).

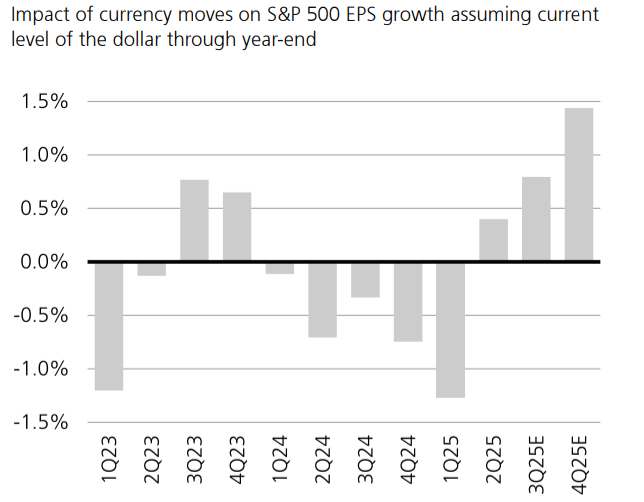

Also, a weaker dollar has an inverse relationship with the S&P 500’s profit; generally, for every 10% change in the US dollar results in an increase of 2.5% in profits, meaning this helps counter-act slumped demand brought about by tariffs (though this varies from sector to sector). AI productivity boosts are vital though in counteracting the increased costs and is so far being successful in mitigating the negative effects of Trump’s tariffs. However, the dollar is forecasted to rise in Q3 and Q4, which could perhaps reduce export demand and reduce profitability (UBS, 2025).

So, for the time being, markets overall are optimistic and seem no sign of stopping with what looks like only the beginning of the AI revolution. Trump has probably picked the perfect time to offload an effective tariffs rate of around 15-20%, with productivity boosts, AI optimism and a weaker dollar dampening the long-term impacts on markets and the economy.

However, what explains the lower volatility we are seeing? Markets reflect investor psychology just as much as they reflect real economic data and the way Trump has been projecting his policies has been muddling with the markets.

This market phenomenon may be deemed a uniquely ‘Trump phenomenon’. The Economic Policy Uncertainty (EPU) index (which measures key words in articles) is currently at record highs (indicating high uncertainty) while the VIX index (measuring volatility used as a “fear” index) remains relatively tame. In theory, market uncertainty increases the power information overload and cognitive biases causing irrational behavioral responses from investors such as herding and anchoring or even overconfidence which can deviate prices from their true values. Historically, the VIX index seems strongly correlated to the EPU index . However Trump’s offices specifically pose a divergence of these two indexes as shown in the figure below.

We’ve all heard about ‘information failure’ when economic agents have imperfect information to base their economic decisions, resulting in market failure. However, we may be seeing information overload; Steven Bannon, Trump’s former adviser, puts this media strategy as “flooding the zone,” essentially bombarding the public with information which when applied to the stock market – confuses price signals and makes it difficult for investors to confidently price assets. This results in a lag in market pricing and, as no single event is deemed decisive enough to create big changes in the market, volatility remains tame. This is evidenced by a study from Booth Business School in 2017, which finds that White House messaging was “unreliable and difficult for investors to interpret,” explaining the divergence between the uncertainty and volatility indexes (Parikh, 2025). However, traditionally, ‘information overload’ tends to increase volatility as, like market uncertainty, it boosts investors’ cognitive biases such as confirmation bias and increasing to perception of risk, meaning risk averse investors are more likely to sell at the first sign of trouble. This contradiction is just one way Trump ‘muddles’ markets.

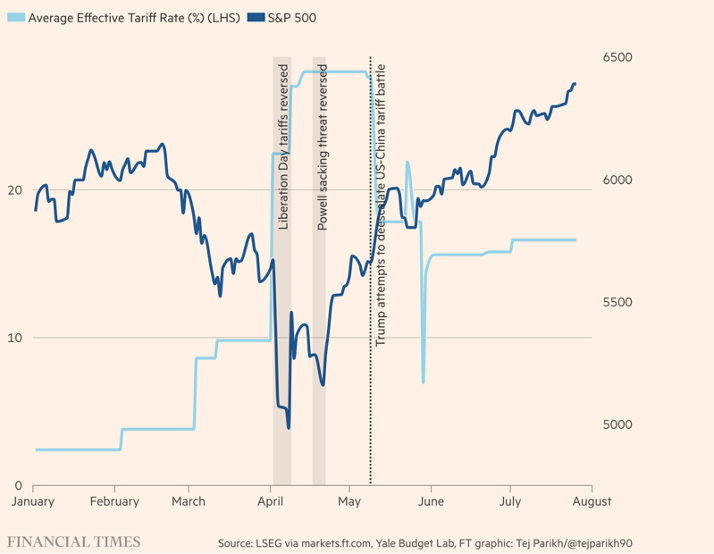

There are very interesting psychological impacts in the way in which Trump gives out information which creates market resilience; Trump has recently been a fan of reserving “bad” policies or even reversing some of his own policies or threats such as reversing liberation tariffs and reserving Powell’s sacking threat. Investors are what’s called ambiguity averse, meaning they prefer known risks to unknown ones and weigh losses more heavily than gains, meaning avoiding a loss is almost psychologically equivalent to a win. Neil Dutta, head of economics at Renaissance Macro Research says, “the walking back of a threat is better for stocks than the threat itself,” a very interesting insight into human psychology, how we process news and how that’s reflected as market resilience. Sharp increases in the S&P 500 are shown below, evidencing this idea.

So, as FT reporter Tej Parikh suggests, Trump has successfully “muddled the markets”, playing an interesting psychological game to muddle price signals and make it difficult for markets to adequately price assets. This combined with general market optimism posed as being very “solid” creates an impression of market resilience.

At the end of his article, Parikh warns “flooding the zone” only delays a reckoning, so is Trump only delaying the inevitable?

Rick Rieder, a chief investment officer at BlackRock claims the US has become the “world’s most shock resistant economies,” having the ability to bounce back from even the most uncertain conditions. As of now, investors are too muddled by stock market optimism and Trump’s uncertainty to make bold decisions of the stock markets. It’s inevitable that markets will react somewhat to Trump’s actions, as he recently did with his firing of the Bureau of Labor Commissioner Erika McEntarfer, but it hardly affected S&P gains (only by 1% or so). Investors seem so desensitized to Trump’s uncertainty that investors turn a blind eye to his more worrying policies if they don’t reduce companies’ future profits too heavily.

However, economic indicators are starting to falter; inflation is rising and revisions in employment growth suggest a steep cooldown – Trump firing the head to the US Labor Statistics with someone “more competent and more qualified” exemplifies this. As Financial Times columnist Janan Ganesh argues, “life for the US President goes downhill from here”.

The question whether markets will react to these faltering economic indicators is another question - will it be counteracted by AI optimism? I think, yes. Markets have weathered much more considerable disruptions to react to lower employment growth rates and increasing (though marginally) inflation. I believe while economic indicators will worsen, the damage will be contained, and markets will remain resilient.

The bounce back of many companies I think is far more prudent in explaining the S&P 500’s resilience which I think will continue. Companies’ adaptability despite tariffs and market uncertainty along with the rise of AI and the productivity boom far outweigh Trump’s uncertainty as AI is here to stay; Trump should be gone by 2029.