This article discusses Trump’s proposed policy to prevent institutional investors from purchasing single-family homes (SFH), along with other complementary policies to make housing more affordable.

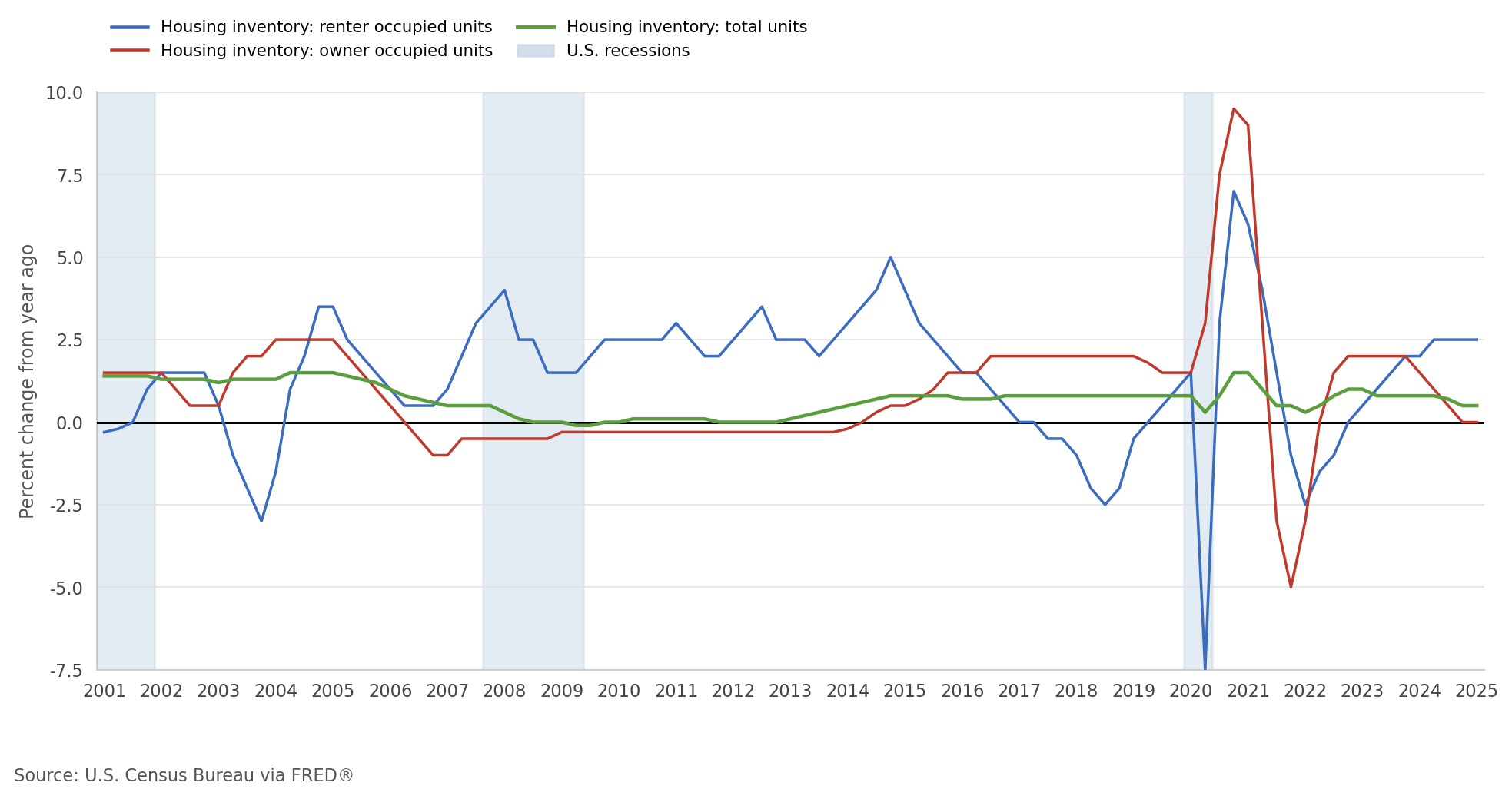

“America will not become a nation of renters,” were Trump’s bold words at the World Economic Forum in Davos, Switzerland, the flagship geopolitical conference attended by world leaders and top academics. This bold claim, as with many of Trump’s claims, has some validity hidden under a masquerade of exaggeration. Currently, approximately 35% of SFHs are renter-occupied, a slight increase from 30% following the 2008 Global Financial Crisis. Figure 1 represents this trend.

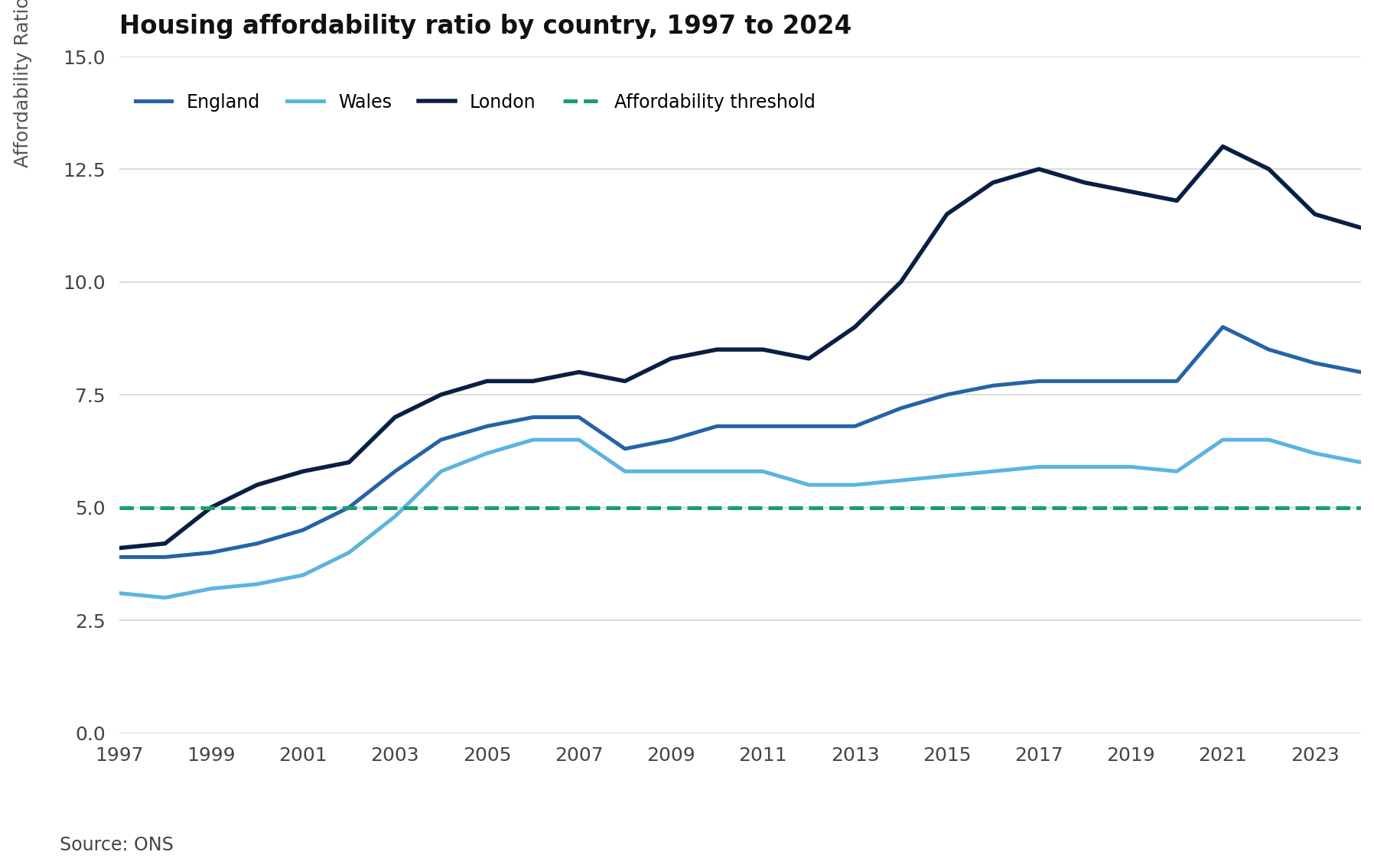

Nonetheless, the housing crisis worldwide is undeniably real and worsening for many households. This is illustrated neatly with the rise in the UK housing affordability ratio shown in the graph below. While many competing reasons can help explain this reduction in affordability, the inevitable effect is lower-income households being forced to rent, whilst investor landlords benefit from rising rent yields.

Trump’s call to prevent this is to scapegoat what he calls "institutional investors” from purchasing SFH. The logic is simple. Large institutions, such as pension funds or private equity firms, invest in properties, which creates a stable store of value and revenue stream. The increased demand raises the prices of house prices, and subsequently rent prices, squeezing out low-income households who want to buy houses and making it harder to rent.

There is some evidence that institutional investors dominate the markets for SFH. For example, in Georgia, Florida, and North Carolina, institutional investor-owned homes constituted about 25%, 21% and 18% of the single-family rental market, respectively. However, as a whole, large institutions own about 3% of the SFR housing stock, per a 2024 analysis by the Government Accountability Office. Therefore, the impact of reduced demand for SFH as a result of this policy will likely be minimal at best.

Even worse, the effect may actually be counterintuitive. Lori Goodman of the Urban Institute argues that firms aren’t buying homes in the way Trump projects. Instead, many firms are choosing to invest in build-to-rent (BTR) projects: properties designed specifically for renters. Its appeal is due to the steady income stream, coupled with a rising asset value, which creates a non-volatile, high-quality investment with a long-term return. Hence, disincentivising these projects could reduce the supply of housing, a factor which could result in higher rent prices.

Policies to punish buy-to-let investors are not new. In 2022, the Netherlands allowed municipalities to impose a buy-to-let ban, aiming to reduce rents and increase homeownership (similar to Trump’s objectives). A team of Dutch researchers investigated the impact of this in Rotterdam, where the local government banned investors from purchasing homes in specific neighbourhoods.

“The ban has successfully increased middle-income households' access to homeownership, at the expense of buy-to-let investors. However, the policy also drove up rents in affected neighbourhoods, thereby damaging housing affordability for individuals reliant on private rental housing, undermining some of the intentions of the law,” wrote the researchers in their paper.

Therefore, this case study demonstrates how imposing bans on buy-to-let can achieve the goal of increased homeownership while exacerbating inequality by raising rental prices. Trump’s policy fares similarly to this, though not as radical, and therefore the impact could be similar, especially on low-income households.

As debt is inevitably an obstacle for many families to buy houses, Trump has directly addressed this by proposing a 10% interest rate cap on credit cards. He claims:

“[Families] have no idea they’re paying 28%, they’re a little late on their payment, and they end up losing their house. It’s terrible.”

While this could be interpreted as a comment on households’ financial literacy, the policy combats the exorbitant interest rate on credit. The average interest rate in November stood at 20.97%, according to the Federal Reserve, and a 10% cap would save Americans $100bn annually - a considerable way to reduce the cost of living crisis. Brian Shearer, director of competition and regulatory policy at Vanderbilt Policy Accelerator, argues that firms can use their high profit margins to absorb this reduced interest rate.

However, the reduced return for banks would result in lower lending, which JPMorgan Chief Financial Officer Jeremy Barnum concluded would be

“very bad for consumers and very bad for the economy”.

The reduced profitability for banks unsettled investors, resulting in shares of JPMorgan Chase and Bank of America, the top two U.S. lenders, dropping 2.5% and 1.6%, respectively. Barnum further mentioned it would “have the exact opposite consequence to what the administration wants”.

Trump also has proposed an idea to use households’ 401k (a retirement savings plan) to fund a downpayment for a house. This would reduce the loan-to-value ratio for mortgages and help families get lower interest rates, a quite logical solution to increase affordability. However, Allison Zelman of the Roosevelt Institute argues that this surrenders to the unaffordability of housing, without actually addressing the root causes:

“It exemplified the crux of his administration’s economic philosophy: Don’t fix broken markets, just let Americans gamble away their futures to participate in them”.

I fundamentally agree with Zelman’s argument; Trump seems to promote policies which help the issue indirectly, rather than address the issue straight on. Yes, a 10% cap would mean families would have higher disposable income and using a 401k helps save extra cash to put as a downpayment towards a house. But none of these actually reduce the prices of houses, or improve the income-to-house price ratio that has been rising ever since the 2008 Global Financial Crisis. If you want to solve the housing crisis, you can’t avoid building more homes.

What Trump has failed to address with his new policies is that the housing crisis comes down to a supply and demand issue. Most solutions to housing crises focus primarily on increasing the housing supply. In the case of some successful countries, this comes down to relaxing restrictions on planning permissions and typically government-subsidised building schemes.

One case study for affordable housing is Japan. Compared to rents in Sydney or Tokyo, they are about $500 less, and the median dwelling price is $680,000, compared with $1.156m in Sydney. One possible explanation for this is that houses are much smaller in Tokyo; the average size is 94.85 sq metres compared to 252 sq metres in Australia.

Nonetheless, Japan’s planning system is a perfect example of a simple system that promotes across-the-board development, as opposed to laboriously granting permission for each house. In Tokyo, there are 12 zones, each defined by the ‘nuisance level’ they allow and range from residential to industrial sites. This makes it much easier for the supply to respond quickly to increasing demand, as pretty much anything can be built, as long as it doesn’t exceed that zone’s nuisance level. This creates a system of highly dense housing, driven by rising land values and shown in the picture below.

However, relaxing planning permissions is easier said than done. A systemic issue facing the UK right now is NIMBYism (Not in My Backyard). If a large-scale housing project occurs in your neighbourhood, two things will happen. Firstly, you suffer the nuisance of builders for five days a week for months on end. More importantly, after the housing project is over, the increase in local supply has a downward pressure on the price of your house, reducing your wealth as a household. While Tokyo effectively banned NIMBYism by establishing its 12 zones, it still remains a large problem in countries such as the UK. Victoria Vyvyan, the President of the Country Land and Business Association, mentions that,

“Nobody wants to concrete over the countryside, least of all us, but for decades governments of all colours have treated it as a museum, risking the sustainability of communities and failing to generate the conditions necessary for growth.”

It is a simplification that the US administration has ignored simple supply and demand issues, but these new policies can learn a great deal from simplifying planning permissions and providing an incentive for building houses.

It is a simplification to suggest that Trump’s administration has completely ignored fundamental supply and demand issues. Still, the scapegoating of large ‘institutional investors’ as the root cause for this housing crisis is wholly misdirected. If the objective was purely to abolish this “nation of renters”, one possible solution is to extend the definition of “institutional investors” from a firm that owns 1000 houses to individuals who own more than 10 houses. I’d argue that this would have a far greater impact by redirecting wealth towards other forms of assets, making it more effective at reducing housing prices.