.png)

• Market backdrop: AI stocks have driven strong S&P 500 performance, but elevated P/E ratios mean investors must assess the true long-term value AI can generate.

• How to assess AI sectors: Five focus areas and twenty performance metrics help identify where AI adoption is most investible and sustainable.

• Most attractive long-term sectors: Customer support AI, AI coding assistants, and cybersecurity AI currently score highest for durable growth and returns.

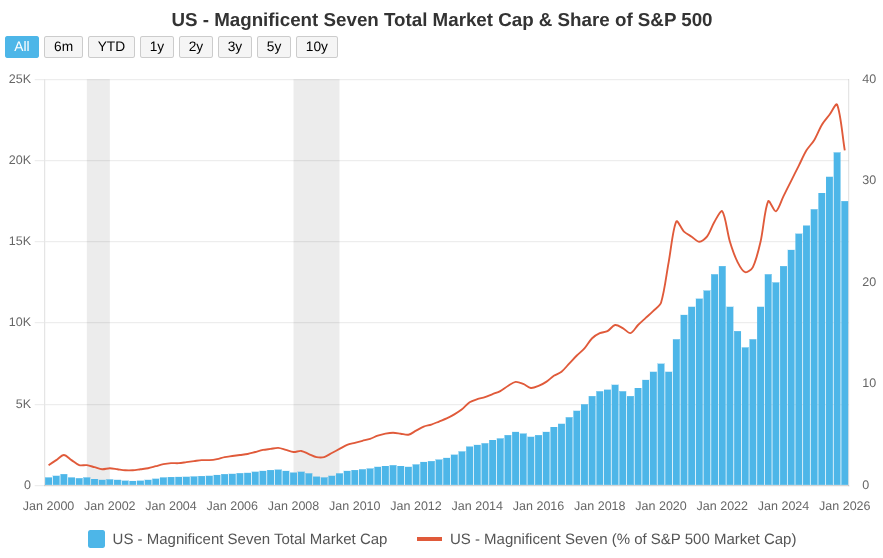

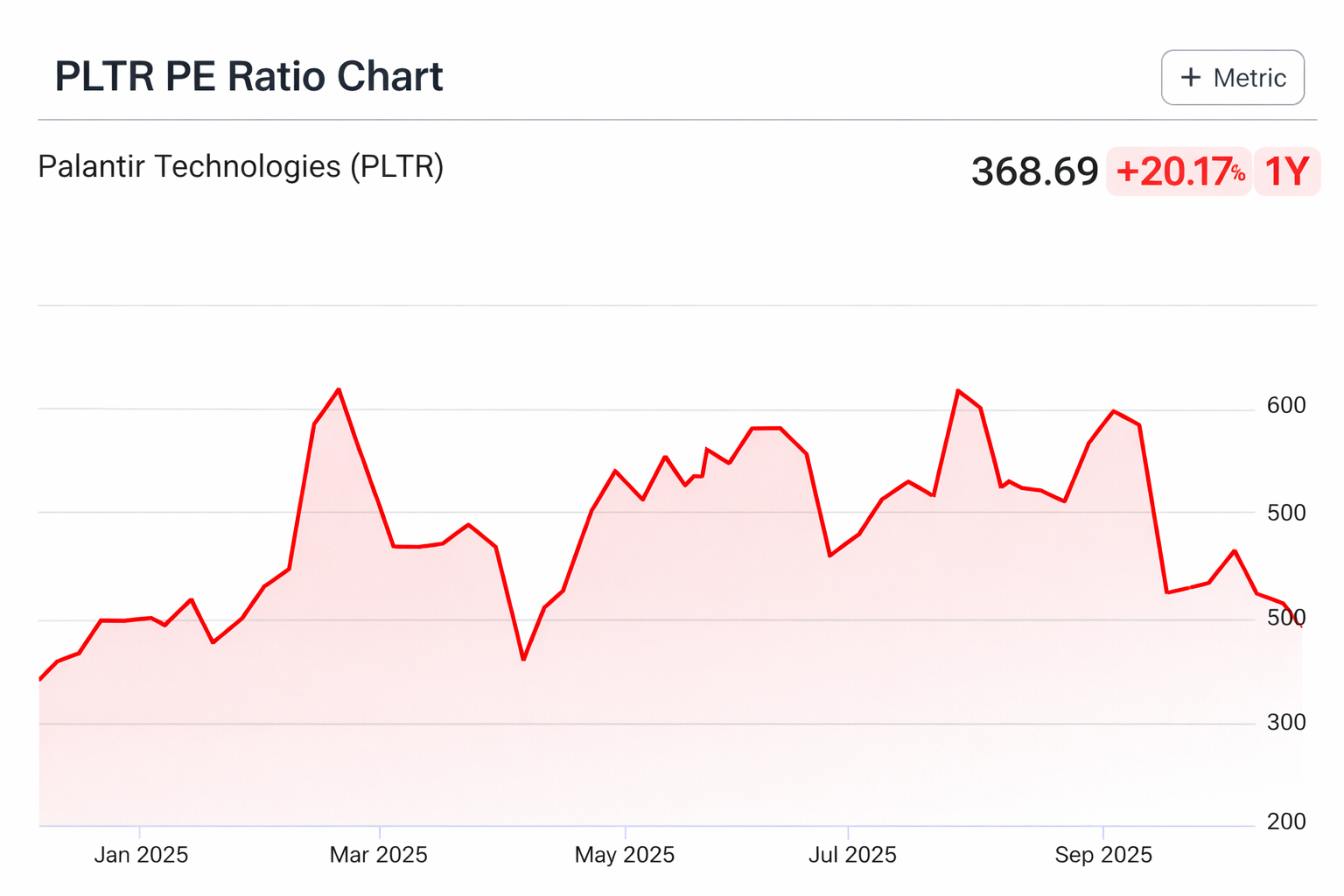

One could definitely say that the AI market is rather buoyant: the Mag7 (Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta and Tesla) had a median P/E ratio of 36 as of 22nd October (Reuters), and 44% of S&P 500 capitalisation was taken up by AI firms as of 24th October (Bank of England), a remarkable level of concentration. While a P/E ratio of 36 is lower than the median dotcom firm at the peak of the dotcom bubble, some outlier firms have produced truly wild financials. For example, Palantir, a firm that creates software platforms for data analysis, has a P/E ratio of 357 (Yahoo Finance).

It is important to note that Palantir’s AI capabilities are impressive: it operates an extensive Artificial Intelligence Platform (AIP) that has been integrated with its existing technical infrastructure, notably its Foundry data platform and Apollo software deployment system. This allows Palantir to serve the operational needs of many sectors. That being said, it would take the firm at least four consecutive years of 50% revenue growth for its P/S ratio to revert to levels where mega-cap technology companies typically trade (IG). Even with the high utility clients receive from Palantir’s AI services, that level of growth will undoubtedly be hard to come by.

The overall financials of the core AI market, along with extremities such as Palantir, have fuelled speculation around the AI market being a bubble. This concern has not just come from casual investors: JPMorgan’s Jamie Dimon has said that some of the money poured into the AI industry will ‘probably be lost’ (BBC), while Google’s CEO Sandar Pichai suggested last Tuesday that the $1 trillion AI investment boom has 'elements of irrationality' (BBC).

Therefore, it is becoming increasingly crucial for investors to differentiate between uses of AI that are, to put it bluntly, a fad, and uses that create value for a broad range of clients. Just as geopolitical gestures by national governments don’t always reflect the reality on the ground, the financials in the AI market currently do a poor job at indicating what small businesses and non-tech multinationals actually consider when investing in new technologies.

Given the high P/E ratios present in the AI industry, investors need to urgently build understanding of where returns will lie if stock prices return closer to underlying fundamentals. This article uses the following two criteria to determine whether a given AI sector can be resilient to any upcoming turbulence.

1) AI sector is genuinely value-creating for the wider economy

This should be a long-term prerequisite as interest in using AI disseminates more broadly across the economy. Multinational, regional, and local businesses that are not at the cutting edge of the technology ecosystem will be much more conservative with the money they want to put on the line for AI. They need certainty in the value creation of a new technology because they are unable to improve it themselves.

2) Leading companies within the AI sector can build strong, defensible moats that can fend off competitors and sustain long-term profitability

For investors, long-term profitability is essential for high returns. If firms are able to lock in consumers and defend their unique edge, then they capture a higher proportion of a growing market over time, generating significant profit growth. Conversely, excessive price competition of the nature that you see in the Chinese EV market is not optimal.

Having both 1) and 2) in a market or firm is essential for an investor. You don’t want to invest in a market that tends towards monopolistic behaviour, but suffers from low innovation and value-creation as a result. Equally, you don’t want to invest in a market that appears highly innovative, but is so competitive that an unprofitable “race to the bottom” occurs.

This article focuses on the following factors to gauge the ability for a given AI sector to adequately fulfil 1) and 2).

Gauge for 1). Does this AI sector meaningfully improve how work gets done? Is this improvement achieved through speeding up processes, enhancing output quality, or both? Does its introduction change day-to-day workflows in a way that augments existing labour and capital instead of replacing them?

Scalability

Gauge for 1). Can this AI sector scale cheaply? Can it grow consumer adoption rapidly after a certain level of public interest? Does its usability naturally improve as scale increases?

Downstream effects

Gauge for 1). Does this AI sector enable broader economic or value-chain improvements beyond its immediate use case? Could its adoption unlock second-order productivity gains in important industries?

Defensibility

Gauge for 2). Can leading players in this AI sector maintain an advantage that rivals will struggle to erode? Does the structure of its market favour durable winners rather than fast commoditisation?

Customer lock-in

Gauge for 2). Once adopted, does the AI sector tend to become embedded in a way that makes customers reluctant to leave? Does continued use make the product more valuable over time, strengthening user dependence?

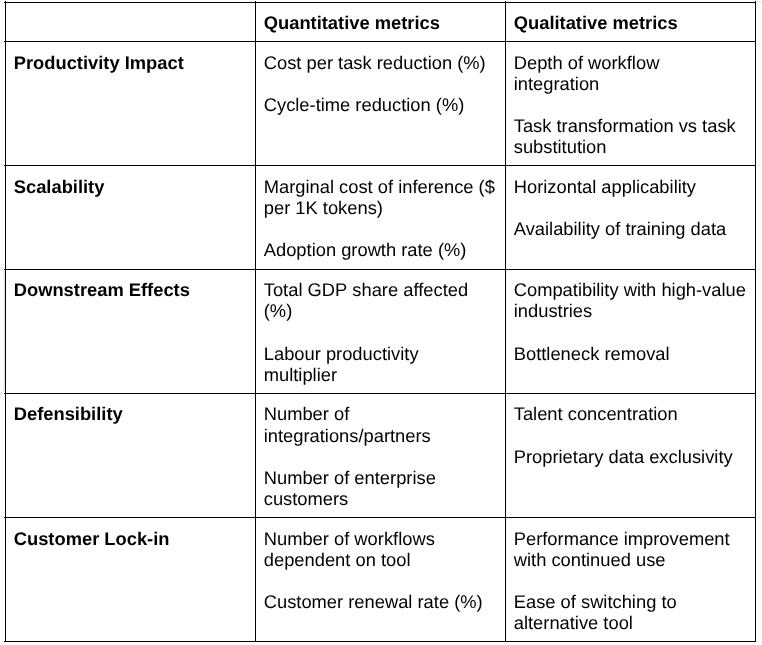

This article uses 20 metrics to measure the benefit of investing in a given AI sector. These metrics have been selected as to be easily researchable and simple for readers to understand.

As shown below, each of our 5 “value drivers” are measured using 4 metrics, 2 of which are quantitative and 2 of which are qualitative. This ensures our analysis has the necessary breadth for us to lock out AI sectors that may be very strong in one aspect but severely lacking in another.

Each of these 20 metrics is given a score out of 5, using specialised score criteria for each metric (provided in the appendix). Adding up these scores gives a total score out of 100.

We can now move on to our list.

Customer support AI leverages technologies like machine learning (ML) and natural language processing (NLP) to assist contact centre employees, automate enquiry processing, and ultimately provide faster, more personalised service. The largest customer support AI players at present are Zendesk, Intercom, HubSpot, Freshworks and Ada.

Strengths

1) Customer support AI produces a very high cycle-time reduction of 40%. This more than makes up for the cost firms incur through using these new systems, which has driven a 23% YoY growth in adoption. Although this growth rate could be higher, it still implies potential for long-term returns.

2) The depth of workflow integration is very high. Customer support AI can autonomously route inquiries, extract data from disparate systems, and trigger multi-step customer support processes.

3) It has horizontal applicability across many industries, including multiple high-value ones. Many sectors, from banking and travel to retail and telecoms, are leveraging AI to streamline customer support. This means that even some lower-performing brands still have a broad space to expand into, buoying growth. Therefore, any poor targeting from investors could be less punishing to relative returns than the other two AI sectors mentioned in this article.

4) Customer renewal rate is exceptionally high, often at >90%. This should help to maintain high adoption growth rates for the most successful firms. Knowing that customers will only leave very slowly makes forecasts of future customer numbers more reliable, meaning these firms have enough certainty to push forward ambitious projects.

Weaknesses

1) The total share of GDP directly affected is only 0.3%. This caps “easy-to-gain” revenues at a lower boundary than is ideal. While there is still room for rapid annual growth in the coming years, growth may decrease markedly afterwards.

2) The talent requirements for utilising customer support AI are not particularly high. Contact centres still require humans for more complex and emotionally nuanced interactions, and most new recruits don’t require a degree. This means the workforce remains very replicable, so it is unlikely that contact centres leaning on AI will automatically deliver higher growth through capturing talented workers.

Summary

Customer support AI has significant strengths in cycle-time reduction, workflow integration, horizontal applicability, and customer renewal. Very high scores in these areas (5/5) have driven customer support AI to 3 on our list. However, it is important for investors to understand the low share of GDP directly affected by this technology and the lack of specialised talent required to use it.

AI coding assistants provide code suggestions, autocompletion, and bug detection, primarily for software engineers. They can also assist with tasks like generating functions, writing documentation, and refactoring code. This allows developers to focus more on the creative aspects of software development. The largest AI Coding Assistant players at present are GitHub Copilot (Microsoft), Amazon CodeWhisperer and Gemini Code Assist (Google).

Strengths

1) There is a very large pool of potential enterprise customers, at over 77,000. This means that top firms could record rapid revenue growth by capturing these clients.

2) There is a high concentration of exceptional talent among a small sect of tech firms and research institutions. There is particular demand for multilingual and multi-modal engineering skills, so any firms that are able to capture workers with both of these abilities should become highly efficient and innovative.

3) Top coding assistant brands have a strong ability to build a sustainable moat. They are often able to collect and retain unique, high-value interaction and code-use data that competitors cannot easily replicate.

4) There is evidence of cross-sector adoption, including in multiple high-value industries. JPMorgan and Goldman Sachs use AI code assistants in their Fintech departments. In the healthcare industry, the Mayo Clinic integrates code generation tools.

Weaknesses

1) While AI coding assistants significantly speed up specific workflows, often by 20-30%, the ones affected are a low proportion of the overall workflows present in software engineering. This means that overall cycle times are only reduced by 8%, which is markedly lower than that of the other two AI sectors mentioned in this article.

2) There is a relatively low number of total integrations/partners, at 31 for GitHub. This means ecosystem depth is still developing, and vendors remain early in building mature, multi-platform systems.

Summary

AI coding assistants have significant strengths in the number of enterprise customers, talent concentration, training data exclusivity, and cross-sector adoption. Very high scores in these areas (5/5) have driven AI coding assistants to 2) on our list. However, investors need to understand the technology’s limited cycle time impact so far and the underdeveloped integration/partner ecosystem.

Cybersecurity AI uses algorithms to automate threat detection and respond to security incidents in real time. It increases the productivity of human security teams by offloading routine tasks, allowing them to focus on more pressing challenges. The largest cybersecurity AI players at present are Palo Alto Networks, CrowdStrike, Fortinet, Check Point Software Technologies, Darktrace, SentinelOne, and Vectra AI.

Strengths

1) Cybersecurity AI produces a very high cycle-time reduction of 30%. This more than makes up for the cost firms incur through purchasing the new technology, which helps to drive a respectable 32% YoY growth in adoption.

2) Its integration into company workflows can be very deep. The technology helps with threat detection, policy automation, incident response, access management and compliance, among many other purposes. These workflows are cumulatively essential for the basic functioning of an organisation.

3) There is a large pool of potential enterprise customers, estimated as being over 20,000. This means that top firms could record rapid revenue growth by capturing these clients.

4) There is clear compatibility with high-value industries. The technology’s ability to automate large-scale threat detection and securitize complex systems is applicable across many industries.

Weaknesses

1) The total share of GDP affected is only 1.2%. This caps potential revenues at a lower boundary than is ideal. While there is still room for rapid annual growth in the coming years, it is possible that growth may decrease markedly afterwards.

2) The estimated customer renewal rate is only ~71%. This demonstrates significant leakage of customers, and could point to more subtle performance issues not fully captured in our statistical framework.

Summary

Cybersecurity AI scores very highly (5/5) on more metrics than could even be mentioned in the strengths section, suggesting unparalleled upsides for investors. This makes it the best AI sector to invest in according to our framework. However, investors need to understand the limits to growth and keep a keen eye on customer renewal rates.

AI is an exciting space: cost reductions and model improvements for everything from AI forecasting to video generation have been truly dizzying. This has been the underlying driver behind rapid stock market growth and comfortable investor returns. However, even adjusted for this, leading financial indicators are starting to look unsustainable. Accordingly, this article should act as a guide for how investors should look for profit potential in the AI market.

The Smart Money Show concludes that the best AI sectors to focus on for long-term returns are customer support AI, AI coding assistants, and cybersecurity AI. We recommend that investors keenly track any leading companies in these spaces and make their own judgment on which ones will capture their respective markets.