The housing market in 2025 can be summarised with one phrase - slow and steady. A 0.8% in general prices as of November represented a resumption to normality, away from the volatile periods of the post-pandemic boom and the mini budget-dip. Nevertheless, the gentle increase signals weaker sentiments prompted by uncertainties on the outlook of the UK economy and tax environment.

The 2025 market can be further categorised as a buyer's market, where supply has exceeded demand for the majority of the time, limiting upward pressures on housing prices. The trend is counterintuitive to the fact that housing has not been more affordable in the last three years; average fixed rates on mortgages continue to hover around 4% and are likely to ease further in the coming months. Halifax’s Amanda Bryden explains the affordability paradox through the psychological effects of record-level nominal house prices on prospective homebuyers. Compounded with rising costs for everyday essentials, households ultimately have less disposable income available for a new property.

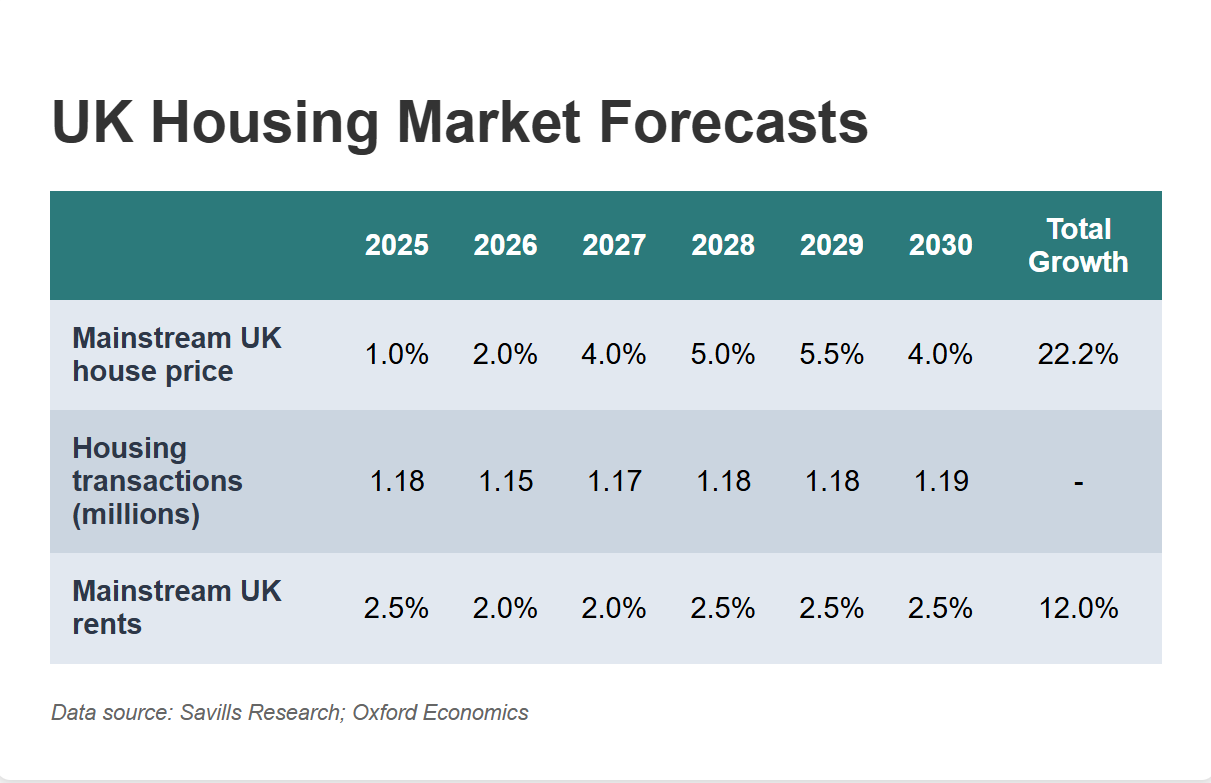

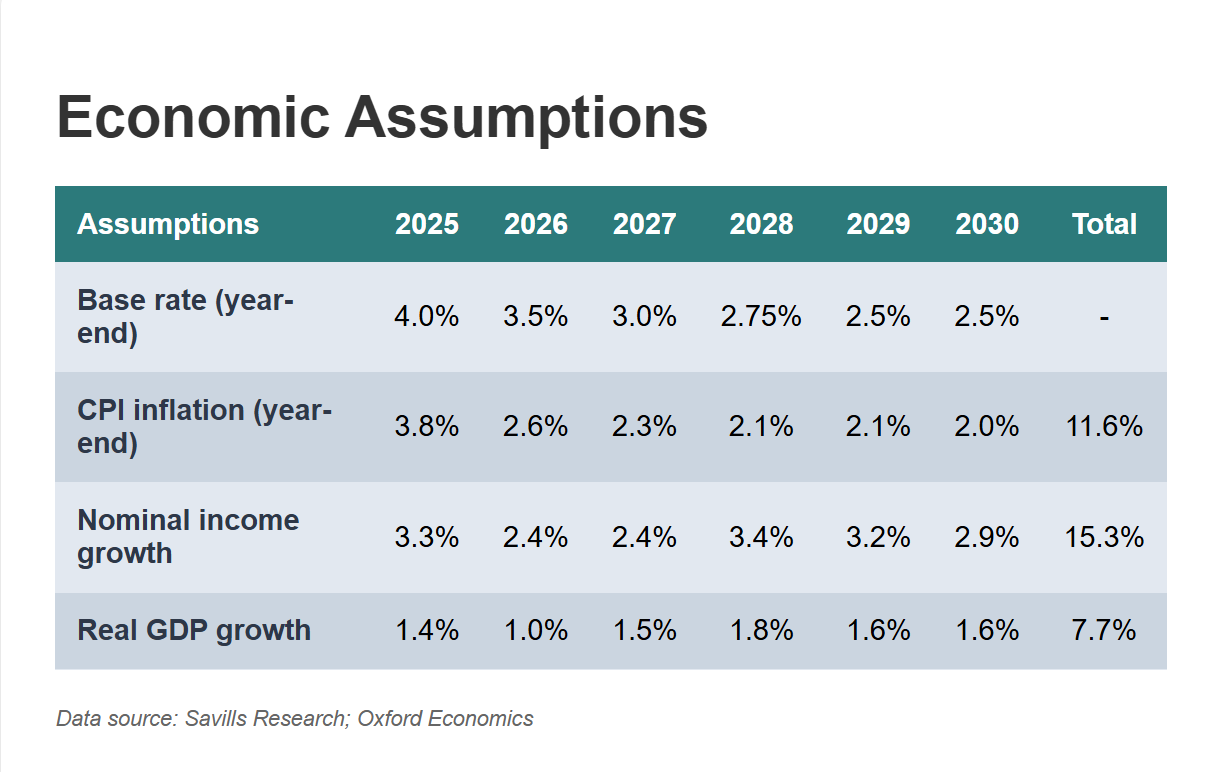

Savills’ recent halving of the predicted growth in house prices in 2026 supports an argument for the continuation of weak property price growth. This is fundamentally based on an assessment of the wider British economy and the estimated sector-specific impacts. The persistence of inflation, with the latest figure of 3.8% YoY in October 2025, has reduced confidence in the materialisation of rate cuts. Oxford Economics now expects just a 50 bps cut by the end of the year, lower than their previous forecast of 100 bps. This means that the cost of mortgages will not decline as quickly as consumers have expected, resulting in reduced transaction activity. They have also forecasted a weakening labour market in 2026, creating slightly higher unemployment and falling wage growth. Both indicators suggest weaker buying power in the future, which could negatively impact the prospect of a strong housing market. If house prices were to increase by 2.0% in 2026, as proposed by the projection, we would have to accept that they continue to fall in real terms, given that inflation and wage growth are both projected to be higher.

Assessing the changes in housing prices in real terms, however, hinges on the concurrence with this particular set of economic data predictions. If, in fact, Inflation in 2026 is lower than expected, then it will most likely lead to a lower year-end base rate and possibly higher nominal income growth. Hence, it is within reason to suggest that house prices may be stronger than expected if key economic indicators exceed mainstream projections. A cityrise article affirms this analysis, citing improved rental stability and lower borrowing costs. Moreover, if the current suppression of buyer activity is the result of uncertainty, we may also hope for improvements on this front once the budget has been announced.

Beyond 2026, Savills forecasts 22.2% growth over the five years to 2030, returning to the average from the last twelve years, even amidst loosened regulations on mortgage applications and continued cuts to interest rates. Cook expressed that “In truth, only a significant unforeseen source of market disruption would change this position.”However, the overall projected improvement in the UK economy means there is capacity for positive real house price growth after 2026, aided by the continued undersupply of new homes, which will also maintain upwards pressure on real prices. Once the prospect of real price growth is secured, it is argued that a revival of buyer activity is extremely likely, seeing as their confidence in the future value of their asset significantly improves.

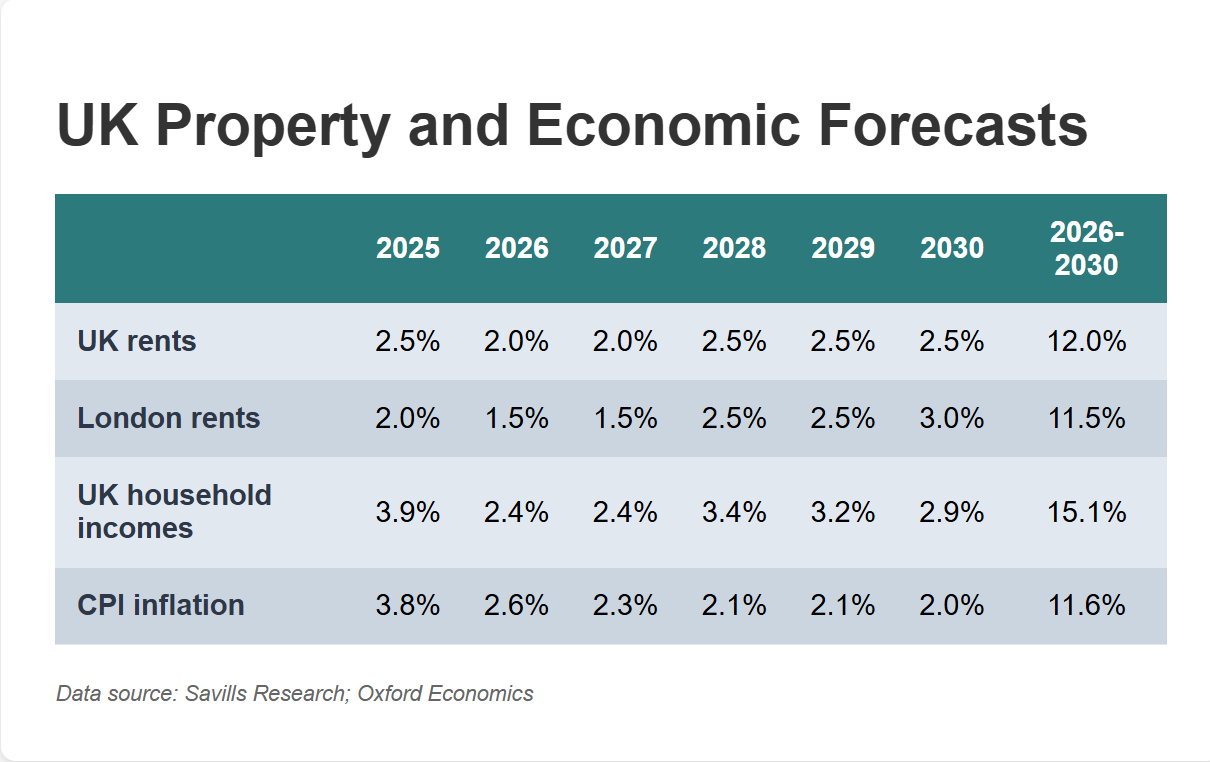

OBR’s November 2025 post-budget forecasts largely align with the narrative, suggesting an average annual real GDP growth of 1.5% in 2026-2030. CPI Inflation figures also show consistency with the dataset, returning to the BoE’s 2% target in 2027 after a projected rise of 2.5% in 2026.

Optimism around the housing market gives rise to investment opportunities in equity markets. Price growths, especially those led by increased demand, are going to increase the volume of transactions across the board. Naturally, a service provider such as Rightmove (RMV.L: LSE) would benefit from this. The stock slid over 30% from an all-time high in August 2025, largely due to unfavourable monthly price movements, and especially from the recent halving of the 2026 forecast. However, this creates a real opportunity to capture the current undervaluation. Its commitment to interact with artificial intelligence in service optimisation may also lead to higher profit growth in the long term, furthering the argument of taking a long position.

Among the critics of the “Mansion Tax” is Nick Sanderson, CEO of Audley Group, who said “, Opting to play with taxes at the top of the housing market is inherently risky. The top of the ladder is often the driver of market movement…” The policy states that £2,500 extra will be charged on properties valued at over £2 million starting from April 2028, rising to £7,500 for properties over £5 million. This move would deter prospective buyers from premium housing, particularly in areas where house prices have grown significantly. Though the expected reduction in transaction volume may have a psychological effect on the wider market, the policy itself has no material influence over most purchases in more affordable areas.

The Chancellor’s plan of reducing the cash ISA allowance to £12000 reaps a greater impact on the housing market, primarily through diminishing the incentive to save. This directly translates into a decrease in funds available for mortgage borrowers. Brokers commented on the importance of cash deposits to building societies in sustaining holiday lets, expat mortgages and adverse credit. Therefore, we may expect tighter lending and higher mortgage rates despite the downward trend of the bank rate. Nevertheless, whether transactions are dampened would depend on the extent to which savings flow into other assets, such as the stock market. The impact will be less significant if the money displaced simply flows into taxable savings accounts.

Though indeed, housing supply depends much on the expected volume of transactions in the future, the 2025 Planning and Infrastructure Bill is set to inject some vigour into homebuilding. In short, this legislation aims to remove previous restrictions imposed by the planning system, including streamlined infrastructure consents and simplified environmental rules. Therefore, the OBR anticipates a strong rebound in housing from 2027 onwards, reaching 305,000 homes a year by 2029-30. If fulfilled, this will be the highest level in the past decades, potentially easing the price increases in mainstream housing.

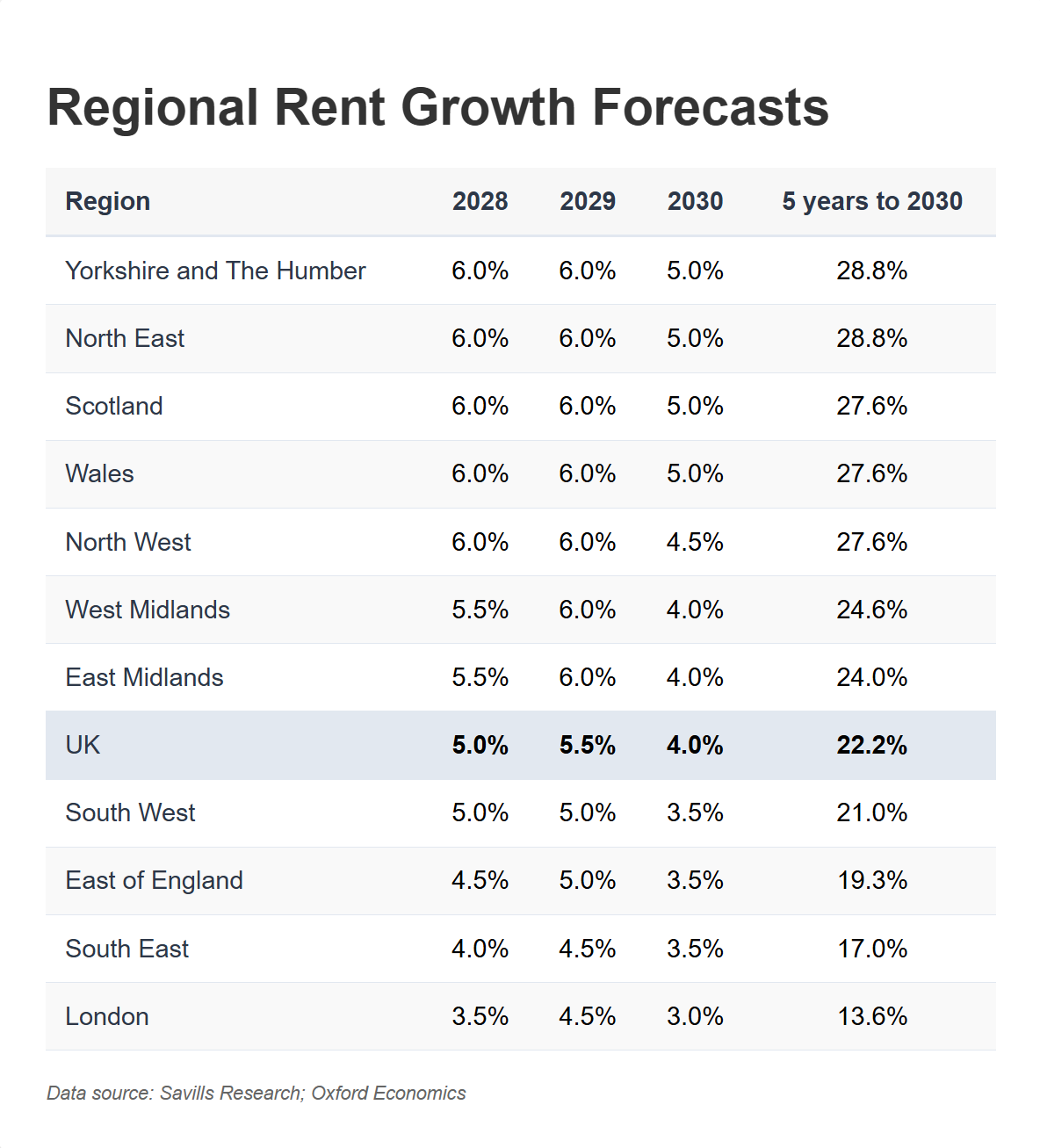

Another way of assessing the housing market is through the lens of regional performance. According to Dan Hill, a research analyst at Savills, “regional performance is largely influenced by where we are in the housing market cycle”. Without diving into another rabbit hole, we may interpret ourselves as being situated in a contraction phase of the market, where more affordable regions outperform the UK average.

This is clearly expressed in the figure above, where London and the South East, known for their relative expensiveness, have less room for price growth; affordability remains central to the discussion. Moreover, Savills forecasts property values in the North West to sit just 15% below the national average, down from 30% in 2020. Meanwhile, average prices in London will fall from 70% above the average to merely 33%. This offers real insights to investors looking to purchase property, emphasising location rather than timing.

Moreover, we can attribute the outperformance of the North West, Midlands, and Yorkshire to the extensive regeneration schemes and transport links, leading to the expansion of economic activity and employment. Thus, cities such as Manchester and Liverpool may continue to deliver excellent rental yields and strong long-term growth potential.

Speaking of variables that might deter buy-to-let transactions, the recent Renters' Rights Act tops the list for the variety of disincentives it presents to current landlords and prospective buyers. For instance, all private rental contracts will be rolling month-to-month or less, while allowing tenants to end contracts with two months' notice. This augments the instability and uncertainty of returns, reducing confidence in supplying a rental property. The security of a rental contract is further undermined by a mandate limiting up-front payment to a month’s rent, encouraging instances of abandonment. More importantly, the landlord’s price-setting ability has significantly decreased through the ban on bidding wars and a ceiling on rent increases. Therefore, it is likely that the supply of rental properties will decrease among smaller landlords who cannot keep up with the policies.

This is accompanied by a structural shift in the rental market, where smaller landlords are selling up to larger and more professional ones. This is expected to ramp up now that the Renters’ Rights Bill has become law, supported by lower rates and higher rents. Ultimately, tighter regulation and taxation will limit the growth of this sector, sustaining the problem of an undersupply in the private rented sector (PRS).

Finally, the proposed increase in property income tax and savings tax within the Nov 2025 Budget would bring further contractionary pressures on supply conditions. Though the increase itself is modest, it essentially equates to a percentage decrease in rental profits, sending a negative signal to those wishing to enter the market as a landlord.

Keeping in mind the theme of a supply-demand imbalance, we should expect continued modest rises in rents across the country, even when assuming demand conditions stabilise (mainly driven by expectations on future incomes and migration).

Womble Bond Dickinson’s head of the financial institutions sector presented BTR’s move “from a niche investment strategy to a central pillar of housing delivery.” What was once an experimental sector a decade ago has now attracted investment from a broad range of institutional capital.

The third quarter of 2025 saw over £800 million invested in UK BTR, bringing the total to £2.6 billion in the current year (in line with 2023 and ahead of 2024). Transactions funding development, a method in which the revenues of the property pay off building costs, continue to drive investments. In 2025 to date, 79% of transactions have been for the development of new homes. However, to match 2024 levels (£5 bn), we will need 49% of the annual investment to come from Q4.

The UK BTR stock stands at over 139,000 completed homes, representing a 14% increase nationally compared to Q3 2024. This is accompanied by 52,500 homes under construction and a further 106,500 in the planning pipeline.

Development challenges remain a prominent issue, visualised through lagged completions for seven consecutive quarters. This is particularly severe in the capital, where BTR construction is expected to decline by 29% in 2025. 96% of developers cite the Building Safety Act as a constraint, expressing the lengthiness of the “Gateway approval” process, which may now take up to a year. Regarding government regulations, there are also significant local inconsistencies in design codes and infrastructure levies. Thus, BTR’s viability depends much on its location.

Moreover, factors such as inflation in construction costs, supply chain constraints, and labour shortages, engender risks that erode project profitability–especially on these debt-funded developments. Therefore, this is a market in which new entrants and smaller developers may struggle to compete.

Nevertheless, the article presents a positive outlook for BTR development, noting a growing role for alternative financing models, including private equity and public-private partnerships. Government-backed funding (e.g., through Homes England) and local authority pension funds are equally important sources of “patient” capital aligned with long-term housing needs. This is one way to de-risk the delivery of BTR housing projects, though it requres careful legal structures for the years to come.

From a societal perspective, BTR is a potential solution to expanding rental supply in urban areas. Since developments are more stable and professionally managed, it is also likely to boost the overall quality of rental housing. However, questions about accessibility, affordability, and the role of institutional capital must be considered when evaluating the optimality of BTR. If investors, the government, and developers can align on quality and sustainability, BTR could play a meaningful role in addressing the UK’s housing crisis. It is therefore in the government’s interest to ease regulatory frameworks, helping the sector to deliver on its promise. Overall, given increasingly flexible financing structures and planning regulations (Planning and Infrastructure Bill), it is reasonable to have considerable optimism about the continued growth of UK build-to-rent housing.

We have covered much ground in this piece, from mainstream analysis to individual discussions on the rental and BTR markets, where a recurring theme of “cautious optimism” emerges as we look to the five years ahead. Although the 2026 outlook is influenced by more uncertainty around economic activity and regulations, a broader analysis with the timeframe of 2026-2030 reflects a healthier trend of growth in both demand and supply for the housing stock. The idea has been reinforced by the recent budget, outlining a more certain future in growth, inflation, and taxation. In particular, build-to-rent developments deserve positive attention for their ability to expand housing supply and transform rental markets, encouraging cooperation between public and private actors in aid of the expansion of the sector. Hence, much can be said in favour of investment opportunities concerning property development and platforms facilitating housing transactions for a medium/long-term horizon. Nevertheless, one must be mindful of the complexities surrounding the market.