For years, blockchain promised to change finance. Now that promise is turning into infrastructure. Today, the world’s largest financial institutions are shifting real activity on-chain, taking traditional assets like bonds, money market funds, and private credit and placing them onto tokenised platforms.

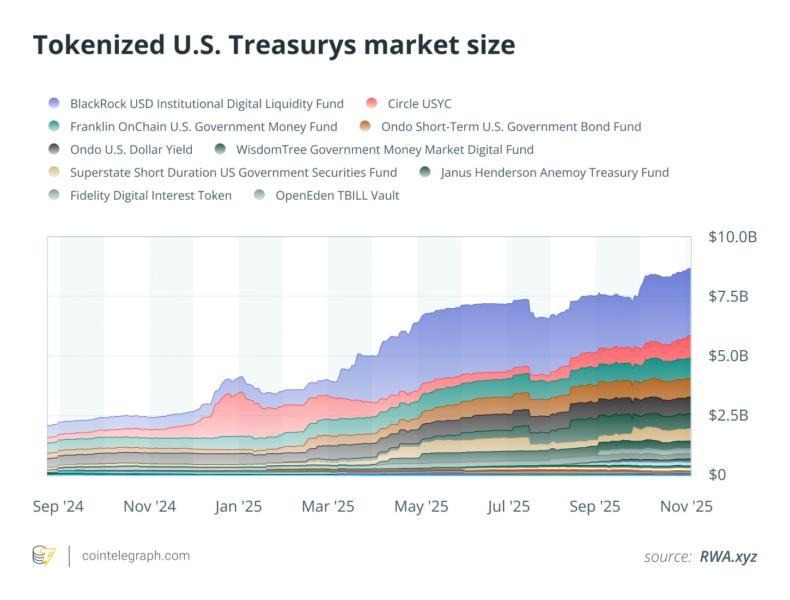

Tokenisation, the process of converting real financial assets into digital ones, is beginning to reshape how markets operate. Major firms are running large-scale projects: BlackRock’s tokenised fund has already passed $500 million, and J.P. Morgan’s blockchain network moves billions in tokenised payments every day.

Even though most people still aren’t interacting with tokenised assets themselves, adoption is accelerating behind the scenes. What started as small tests inside banks has grown into real market activity, with more institutions exploring how far this technology can go.

The shift is no longer theoretical; it is unfolding quietly at the core of global finance.

The depths of this technology are still being tested. Key questions remain, such as how regulators will respond or whether it will genuinely change the way markets function. However, what is clear is that the financial world is entering a new phase, where the move from traditional systems to digital, on-chain infrastructure is becoming increasingly difficult to ignore.

Tokenisation is the process of turning real financial assets into a digital version that exists on a blockchain. The asset itself does not change; the way ownership is recorded and transferred does. Instead of relying on paperwork, outdated bank systems, and slow settlement processes, a tokenised asset transfers instantly between two parties using a digital record.

A simple way to think about it is that tokenisation does for financial assets what mobile tickets did for events. The concert is still the same, and your seat is still the same. But the ticket now lives online, making it easier to check, transfer, and verify. Tokenisation applies this same logic to funds, bonds, and cash.

Take BlackRock’s BUIDL fund. Instead of giving investors a paper statement, it gives them a digital token that represents how much of the fund they own. The investment itself is the same. They still own the same assets as before. The token is simply a faster, more efficient way to show and transfer ownership.

Put simply, tokenisation does not alter the asset itself. It modernises how ownership is recorded and transferred, making everyday financial products quicker and easier to move within a digital world.

While tokenisation can be applied to almost anything, the biggest momentum today is around real-world assets, also known as RWAs. These are traditional financial products such as government bonds, money-market funds, private credit, or real estate. They have existed for decades, generate predictable returns, and form some of the most heavily traded and widely used assets in global finance.

Banks are not trying to reinvent finance. They are upgrading the infrastructure behind assets people already use. RWAs are an ideal starting point because they are familiar, stable, and heavily regulated. Tokenising them does not introduce new risks. It simply modernises the way they move.

A helpful analogy is the postal service versus email. The message stays the same, but email delivers it faster, more reliably, and with fewer steps. Tokenising RWAs works the same way. The asset, whether a bond, a fund, or a loan, is unchanged, but the issuing, transferring, and settling process becomes significantly more efficient.

This shift is already visible in some of the world’s largest financial institutions. BlackRock’s tokenised money-market fund has surpassed $500 million, giving investors a digital token that tracks their share of the fund. The underlying asset still holds a basket of cash, U.S. government securities, and repurchase agreements. But instead of waiting for transfers to push through slow, bureaucratic systems, ownership updates automatically on the blockchain, cutting manual processes within large firms. For something as widely used as an MMF, even modest efficiency gains create meaningful impact.

J.P. Morgan is making similar progress through its Kinexys network. Kinexys can be thought of as an express rail line for banks to move assets quickly and in sync. Traditional banking depends on a maze of separate systems where one transaction can pass through several stages, only settle during market hours, and take days to confirm. Kinexys replaces this with a shared digital ledger where value moves and settles at the same time. This matters for tasks that rely on precise timing, such as short-term lending when cash and collateral must switch hands instantly.

Even the repo market – one of the largest and most important parts of global finance – is being tested on-chain. These transactions involve institutions swapping cash and government bonds, often overnight. Tokenising this process aims to remove settlement delays and reduce the number of intermediaries involved.

All of this is happening behind the scenes, with most investors barely noticing. But within the plumbing of global finance, tokenising RWAs is quickly becoming one of the most serious and fast-moving uses of blockchain technology.

Tokenisation matters because it lets financial markets operate at a speed that matches the modern world. Many of the systems used to move money today were built decades ago, when transfers took days, paperwork travelled by post, and global trading was limited. Tokenisation upgrades this outdated infrastructure rather than replacing it.

Instant settlement is one of the largest advantages. In traditional systems, banks need time to confirm balances and update internal records when assets change hands. Tokenised assets settle the moment they are transferred, with every party seeing the same updated record at the same time. This removes delays, reduces errors, and cuts the manual steps that slow transactions.

Transparency also improves. With a shared digital ledger, everyone involved in a transaction views the same information at the same moment. This reduces disputes, eliminates mismatched records, and provides a clearer audit trail. In markets where billions move each day, a single reliable source of truth makes operations far smoother.

Tokenisation can lower operational costs as well. Traditional processes rely heavily on repetitive administrative work. Digital systems automate much of this, shrinking the number of steps involved. Over time, this saves institutions significant sums, especially in high-volume areas like repo markets or cross-border payments.

It also makes ownership more flexible. Tokenised systems can divide large assets into smaller digital units, making them easier to trade or transfer. The underlying value of the bond or loan does not change, but the ability to move fractional pieces can improve liquidity and expand access.

Tokenisation also moves markets closer to operating around the clock. Traditional systems shut outside business hours and often pause over weekends. Digital ledgers do not. Value can move whenever needed, which is especially useful for global institutions operating across time zones.

All these benefits point to the same conclusion. Tokenisation is not reinventing finance. It is fixing systems that have fallen behind modern technology. By making markets faster, clearer, and easier to operate, it offers a meaningful upgrade to the infrastructure that supports global finance.

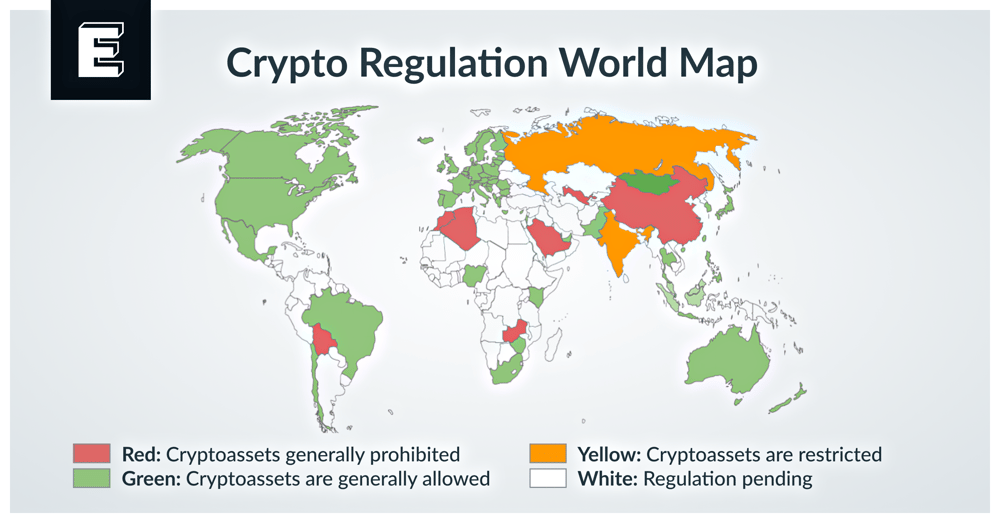

Regulation is the main factor that will decide how far tokenisation can expand. Financial markets operate under strict oversight, so regulators want digital assets to settle safely, remain easy to audit and fit within existing legal frameworks. This is why RWAs such as bonds and money-market funds were the first to be tokenised. They are stable, predictable and straightforward for regulators to evaluate.

Singapore is leading the shift. The Monetary Authority of Singapore’s Project Guardian has already tested tokenised bonds, funds and foreign-exchange transactions with major banks, giving regulators real evidence of how these markets behave on-chain. In the U.S., tokenised assets fall under existing securities laws but lack a dedicated framework. Europe’s MiCA rules are clearer, though several key details remain vague. This creates a patchwork of inconsistent approaches that slows global adoption.

These gaps feed directly into the main risks, with liquidity being the biggest. Tokenising an asset does not guarantee an active market of buyers and sellers. Interoperability is another challenge. Banks are building separate systems that cannot communicate, risking a landscape of isolated digital networks that are no better connected than traditional finance.

There is also concern that tokenisation could end up reinforcing the power of a few large institutions instead of creating a more open and transparent system. The final uncertainty is scale. Tokenisation has performed well in controlled pilots and private networks, but it still needs to prove it can handle the volume and stress of global markets. Until regulatory standards are clearly defined, most progress will continue behind the scenes.

The direction is clear, but the speed of adoption will depend on how quickly regulators and institutions can agree on the rules that shape the next phase of financial infrastructure.

Adoption is still happening out of sight, and the next phase of tokenisation is likely to develop through steady, practical upgrades rather than dramatic disruption. Most changes will sit in the background: faster settlement, cleaner record-keeping and digital rails quietly replacing older operational processes across institutions.

Shared digital networks will become more important as banks try to move away from isolated systems. Projects like Kinexys point to a future where institutions connect through common infrastructure, allowing value to move in real time rather than through fragmented systems. If this approach becomes standard, it would push markets toward more continuous and coordinated operation.

Tokenisation could also make certain markets more flexible. By splitting assets into smaller digital units, institutions can structure exposure with far greater precision. This won’t transform retail access, but it can make large, high-volume markets run more efficiently.

Cross-border finance is another area that could see meaningful gains. Today, global transactions move across incompatible systems and competing time zones. As more regions adopt tokenised infrastructure, even partial connectivity between networks would reduce friction in settlements and improve coordination, without requiring new laws or radical regulatory reforms.

The future of tokenisation looks less like a replacement of the current financial system and more like a gradual migration toward digital infrastructure that works quietly behind the scenes.

Tokenisation is moving from theory to practice as banks and asset managers use it to streamline how financial assets move. The benefits so far are subtle but real. Transfers settle faster, records are cleaner, and digital systems are starting to replace older manual processes that once slowed operations down.

What happens next depends on scale. These early improvements need to hold up under heavier volumes and stricter regulatory demands. Clearer rules, common standards, and broader participation will determine how far tokenisation can go. Even so, the trajectory is already visible. Institutions are quietly building a digital layer beneath existing markets, making the system more connected and more efficient without changing the assets themselves.

If adoption keeps growing at this pace, tokenisation won’t feel like a dramatic overhaul. It will feel like a natural upgrade. Markets will begin to operate with the speed and accuracy people now expect in a digital world, not because the financial system was rebuilt, but because its foundations were modernised piece by piece.