Soft commodities consist of products that are grown instead of extracted. Examples include coffee, cocoa, sugar, and wheat - essential food products that are sought heavily by a majority of the global population. However, these commodities need specific weather conditions, predominantly high temperatures and moderate rainfall. However, the world has warmed by an average of 1.1 degrees Celsius compared to pre-industrial times, meaning that weather events have become more erratic and unpredictable, such as the example of Brazil experiencing severe droughts from 2020 onwards. This has caused prices to rise since production is weakened by extreme weather, creating a significant dilemma for buyers of these commodities (e.g., Nestle is a major buyer of cocoa). A method to hedge this risk is forward and futures contracts, which enable buyers of soft commodities to help alleviate this threat to their production costs.

Future and forward contracts are financial instruments designed to enable investors to purchase or sell a good at a future date. This alleviates risk volatility, caused by potential price rises or falls, which could harm both buyers and sellers. Yet, whilst similar in purpose, futures and forward contracts vary from each other. Future contracts consist of trading on an exchange system where the prices fluctuate based on market forces. This contrasts with forward contracts, where it is a private agreement between two parties, where the commodity is agreed to be purchased at a future date at a specific price. This is known as an Over The Counter (OTC) Trading agreement, where there is no financial intermediary, as in this scenario, an exchange system.

These financial derivatives are essential when trading soft commodities, since the supply of soft commodities can be affected significantly by weather patterns, pests, and diseases that can worsen harvest quality. Furthermore, growing specific crops such as cocoa and sugar in tropical regions can make these products extremely volatile due to more significant weather events, such as extreme flooding or devastation caused by hurricanes, for example. For farmers who sell their produce, future and forward contracts enable them to maintain income security, which is vital for them, especially as the majority of soft commodity farmers are located in less developed countries, where there are weak labour regulations that can keep income levels low compared to their wealthier counterparts in more developed countries.

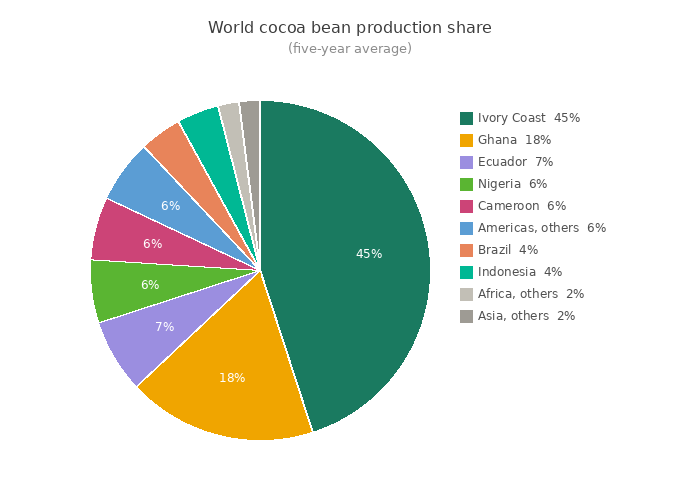

Examples include the Ivory Coast, the country that is a dominant global supplier of cocoa production as shown in Figure 1. Here, cocoa production supports 8 million people, and many of these farmers who produce cocoa are local and small-scale. Studies have shown that there are irregular weather patterns in West Africa, as a result of anthropogenic global warming. This can affect crop yield significantly due to reduced production from weak rainfall, as well as soil degradation caused by excessive rainfall, which can also increase black pod disease and insect infestations. This has increased instability in global cocoa markets, hence increasing the usage of forward contracts by Ivory Coast farmers to ensure that income is maintained at a predetermined price, where their produce is sold to buyers via cooperatives, as the price is fixed by the government. This also benefits its buyers (for example, those who purchase a significant amount of cocoa beans from the Ivory Coast), which can help increase price certainty, allowing Nestlé to stabilise input costs.

However, the price volatility of soft commodities varies day by day, and at any moment of the day, the price of cocoa or sugar could change significantly, especially if there are unforeseen weather events such as flash flooding, which can weaken production. Hence, to hedge against this risk, commodity trading houses (examples include Cargill, Louis Dreyfus, Olam) are often used to purchase soft commodities, store them, and then sell them to companies such as Nestlé, which would demand a reliable all-year-round supply. By storing soft commodities in warehouses, they often use futures and forward contracts themselves to secure the price of their stored commodities, which companies such as Nestle rely on as their source of production for their final products. This can be vital when accounting for climate risk, where higher prices would lead to trading houses absorbing the shock by using their stored produce to supply the companies that seek it. Then they can use future contracts, where they can hedge the price risk and ensure that they are purchasing at a fixed rate in the future, which may be lower than the market price. This can ensure that the price being passed onto Nestlé is not significantly higher and is not likely to affect their market prices negatively.

Using financial derivatives is challenging for farmers in less developed regions, such as Guatemala and the Ivory Coast, who may have limited expertise in the function of the exchange trading systems that are used to buy and sell soft commodities. However, the usage of forward contracts is utilised by the Ivory Coast government, who use them to set farm-gate prices, which are fixed prices to ensure farmers earn a return on their production and helps to shield from global price volatility, which cocoa has a significant reputation for.

However, setting prices early in future contracts can bring additional problems, such as the price being set below global prices that can change at any moment, where the return for farmers could be limited. Future contracts assume a certain output, which can be difficult to meet if climate change weakens harvest output, creating delivery risk. For farmers in forward contracts, they are price takers, not makers, since price is regulated by the government, illustrating that the price set by the national authorities could be too low to maintain living standards. It is estimated that many cocoa farming households in the Ivory Coast earn below the World Bank extreme poverty threshold ($2.15/per day per person, 2017 PPP), highlighting how the income earned does not help increase their living standards. This can highlight the market inefficiency of price setting, where prices may be set as low as possible to remain globally competitive.

Whilst future and forward contracts have similarities in hedging the risk against price volatility, they are notable differences. Forward contracts tend to be more flexible since they are privately negotiated agreements between the two parties, who can fix every detail of the transaction, including the quantity, time of delivery and place of delivery to meet their demands, whereas futures are standardised and thus do have such flexibility. The liquidity of futures results from the fact that their standardised features allows for anonymous trading on the exchange, whereas forwards cannot be traded anonymously because they are private contracts negotiated individually. The perfect example of the ability of forwards to meet a specific need in the real world is the Ivory Coast cocoa system, where the Conseil du Café-Cacao (the government price regulator) enters into a personalised forward contract with the trading house Cargill, fixing the quantity of cocoa of Ivorian origin to be delivered at a later date, which would be impossible with standardised contracts of ICE (Intercontinental Exchange) cocoa futures that deal in deliveries of only 10 tonnes each at a time.

The world will likely experience more extreme weather patterns as the global average temperature rises 1.5 degrees Celsius above pre-industrial times, which is likely to lead to longer and more intense droughts and floods, potentially affecting price volatility further. This is much like the case in Figure 2, where Ghana’s cocoa production has dropped sharply due to poor weather conditions negatively affecting its harvest. It could be argued that further rises in global temperature could weaken supplies further, and this could lead to a likely general rise in prices in the future if it is more costly to produce soft commodities in a warmer world. Furthermore, the price rises are likely to be more significant, which can make hedging against them more expensive in the future. Additionally, financial derivatives cannot prevent physical shortages, so this likely consequence of global warming will have to be alleviated by ensuring that soft commodities farming can adapt to the warmer world, such as through having a sustainable irrigation system or growing drought-resistant varieties.

Overall, financial derivatives have been a vital solution to manage price volatility across soft commodities, which is notoriously significant due to extreme shifts caused by changing weather conditions. However, with weather patterns becoming more extreme, it would be more apparent to ensure that every farmer across the globe has access to these derivatives, since many of these farmers live in areas with weak regulation and a financial system. Therefore, these derivatives could highlight the essential role of soft commodity farmers and how their production is important in a world that is becoming increasingly dependent on soft commodities.