The Strait of Hormuz is a Middle Eastern chokepoint situated between the Persian Gulf and the Gulf of Oman, with it being the only sea passage from the Persian Gulf to the open ocean. Situated between Iran in the north and the UAE and Oman in the south, it has been in sharp focus since the conflict in the Middle East erupted on the 28th February. Iran has ordered that no ships can pass through the Strait of Hormuz, as the nation has significant leverage on the chokepoint due to its longer coastline and in control of the 7 out of 8 islands in the chokepoint. According to the energy consultant firm Kpler, 16-18 million barrels of crude oil flow through each day, and flows of LNG through the Strait consist of 20% of seaborne supply, thus illustrating the essence of the chokepoint to global energy supply and consumption. Yet, the closure has ceased crossings by ships, reducing the supply of global oil and natural gas and thus increasing prices significantly over the last week.

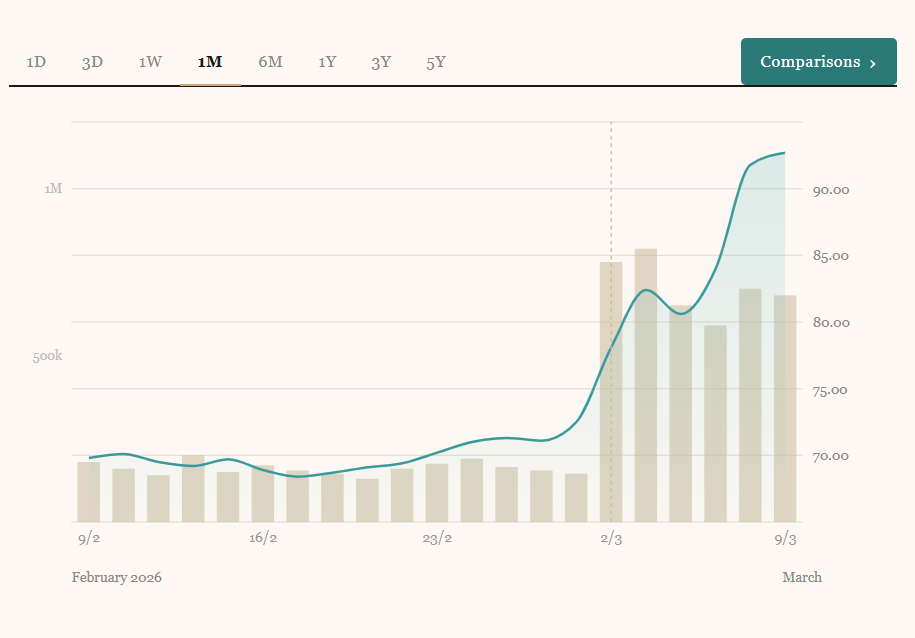

Following the closure of the Strait, the price of Brent crude oil has increased significantly to above $100 on Monday 9th March with fears that it will increase further as shown in Figure 1. 5 of the 7 largest oil reserves are situated in the Middle East, where nearly half of the world’s oil reserves and exports come from. With reports of Iran attacking ships containing oil since its reported closure, many countries in the Gulf region such as Kuwait and Iraq have cut oil production due to the closure of the Strait causing a loss of access to world’s oil markets. This has notably led to a widening in the Brent/WTI spread, which is the price difference between the two main global oil benchmarks with WTI (West Texas Intermediate) priced lower due to it being landlocked and most refineries being suited to Brent oil. Since, a majority of buyers purchase Brent crude oil, this increase in widening compared to much smaller sizes of widening ($2-$5) in normal times, is a cause of concern especially if it increases further, with Qatar suggesting that it could reach $150, a tail risk, where this definitely would have adverse effects on the global economy.

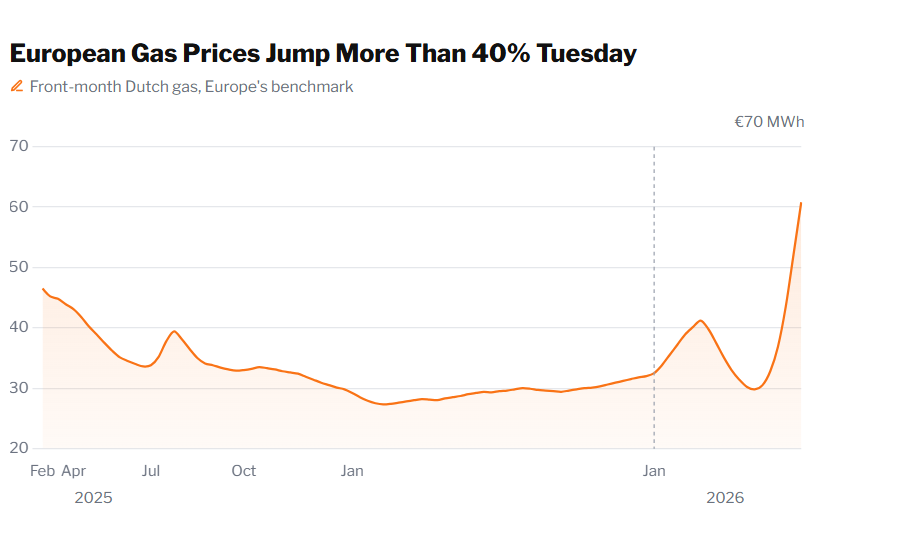

The closure of the chokepoint has not just led to a rise in oil prices, but also the price of natural gas. Using TTF (Dutch Gas) as part of the European benchmark, there has been a sharp increase in gas prices, with prices rising to €60 MWH. This has culminated in the closure of the QatariEnergy facility, which closed last week due to an Iranian drone attack, where it produced a fifth of global LNG supply. As a result, this reduction of supply has raised fears of a further increase in the price as the conflict continues, with a forecast from Goldman Sachs suggesting how TTF could increase up to 130% from the start of the war, which would put it at the same price level as the initial war of the Russian-Ukrainian conflict. This is especially vulnerable for Europe, which in 2022 had replaced gas imports from Russia with seaborne LNG from Qatar. This weakness of changing dependency is also significantly worse for Europe due to a lower gas storage than in previous years, with this year the gas storage is only 30% full. Consequently, this will make Europe less able to resist this supply shock if the war is prolonged, which could increase prices further across the continent, exposing the vulnerabilities in limited diversification for natural gas sources.

The most significant risk of higher oil and natural gas, two essential commodities, is the risk of higher imported inflation. Brent crude oil is heavily utilised in a range of products from heating homes, to fueling transportation in aircraft and vehicles, and the fact that Brent crude oil features significantly in everyday uses such as plastic and cosmetics. It is highly likely that a higher Brent crude oil and natural gas price will lead to a rise in general inflation, which will weaken real incomes, dampen animal spirits, and reduce living standards similar to those in 2022 when the Ukraine war had commenced.

Despite this, it could be argued that this effect of higher commodity prices will depend on the exposure to global oil and LNG markets. Countries that are likely to bear the brunt of higher Brent crude oil prices include Japan, China, Germany, and India, which have large populations and economies. Similarly, countries most exposed to global LNG prices are Germany, China, and Italy. The UK is also import dependent on both Brent oil and LNG gas, with the North Sea insufficient to meet consumption, and it is estimated that energy bills will rise significantly at the next price cap setting in July. Yet countries that are more self-reliant on energy sources are likely to benefit from higher global prices, with examples including Norway and the USA, which both have significant reserves of Brent and Shale respectively.

The future outlook is uncertain, with no end in sight for the conflict in Iran and neighbouring countries, with President Trump stating it will take as long as it takes. Yet, it looks certain that a prolonged conflict will push up commodity prices further and is likely to have devastating effects on world economies and everyday lives, as argued by the Qatar foreign ministry. This conflict highlights the essence of the Gulf in supplying the world with essential commodities, and how a blockade on the Strait is likely to have significant repercussions across the world, hurting economic firms and the general public.