A few years ago, NFTs were everywhere. What began as simple digital collectables for crypto users quickly moved into the mainstream, with artwork, profile pictures, and blockchain-based brands generating headlines and billions in sales.

Collections like Bored Ape Yacht Club and Pudgy Penguins became cultural symbols, and the idea of digital ownership looked set to redefine how we interact with media.

This sudden surge of attention pushed NFTs far beyond their niche origins. Auction houses began selling tokenised art, celebrities and influencers endorsed projects, companies like Nike experimented by releasing digital collectables, and NFT marketplaces saw trading activity at levels few could have predicted.

For a brief moment, NFTs represented a new creative economy, while also becoming one of the fastest-growing segments of the wider crypto market.

This momentum did not last. As markets began to cool, interest faded, and many collections lost most of their value. Trading activity fell sharply, scams, rug pulls, and failed projects damaged trust, and the downturn exposed just how reliant the boom had been on hype and rapid liquidity.

What had once been presented as a digital revolution became, for many, a painful lesson in how quickly narratives can shift within emerging technology.

Yet the story of NFTs is not as black and white as a simple rise and collapse. Beneath the noise, some brands endured, solidifying themselves while most of the market disappeared. Many of the core ideas continued to develop quietly in the background. Understanding this cycle requires looking at the full picture: how the hype began, what fuelled it, why it broke down, what remains, and what the future may look like.

Long before NFTs became a mainstream term, the idea behind them was being explored in small online communities. Early crypto developers were trying to answer a simple question: can you prove ownership of a unique digital item on the blockchain? The technology was still limited, but these experiments quietly built the foundations for everything that came later.

One of the earliest versions appeared through Bitcoin as “Coloured Coins”, which tried to mark certain coins as representing something specific or unique through their metadata. It was a clever idea, but Bitcoin’s architecture wasn’t designed for this level of customisation, so the concept never moved far beyond small developer communities. Still, it showed that digital ownership was possible and acted as a precursor to NFTs.

When Ethereum launched in 2015, experimentation picked up. Its flexible design made it far easier to create and track digital items, leading to early collections like Rare Pepes. These were small, niche tests, but they showed what digital ownership could look like. By 2017, projects like CryptoPunks and CryptoKitties demonstrated that the idea could scale, with activity slowing the Ethereum network and providing the first real sign that NFTs had room to grow.

NFTs remained niche throughout the 2010s. Marketplaces were small, activity was limited, and the broader public had little awareness of the concept. But the core idea - scarce, verifiable digital ownership - had been planted. Once the right conditions emerged, this early groundwork made the rapid growth that followed possible.

By 2020, the early groundwork finally had the conditions it needed to grow. The idea of digital ownership had been planted years earlier, but it wasn’t until more people moved online, interest in crypto increased, and new platforms emerged that it began to take shape. What had started as a small niche for collectors and developers began to develop roots in broader culture, setting the stage for NFTs to move from an experiment to a genuine component of crypto.

One of the first major sparks came from NBA Top Shot, a platform that allowed users to buy and trade digital basketball highlights. It introduced NFTs in a way that felt familiar: simple, collectable, and tied to a major brand. For many, this was their first interaction with owning an item on the blockchain, and activity grew rapidly.

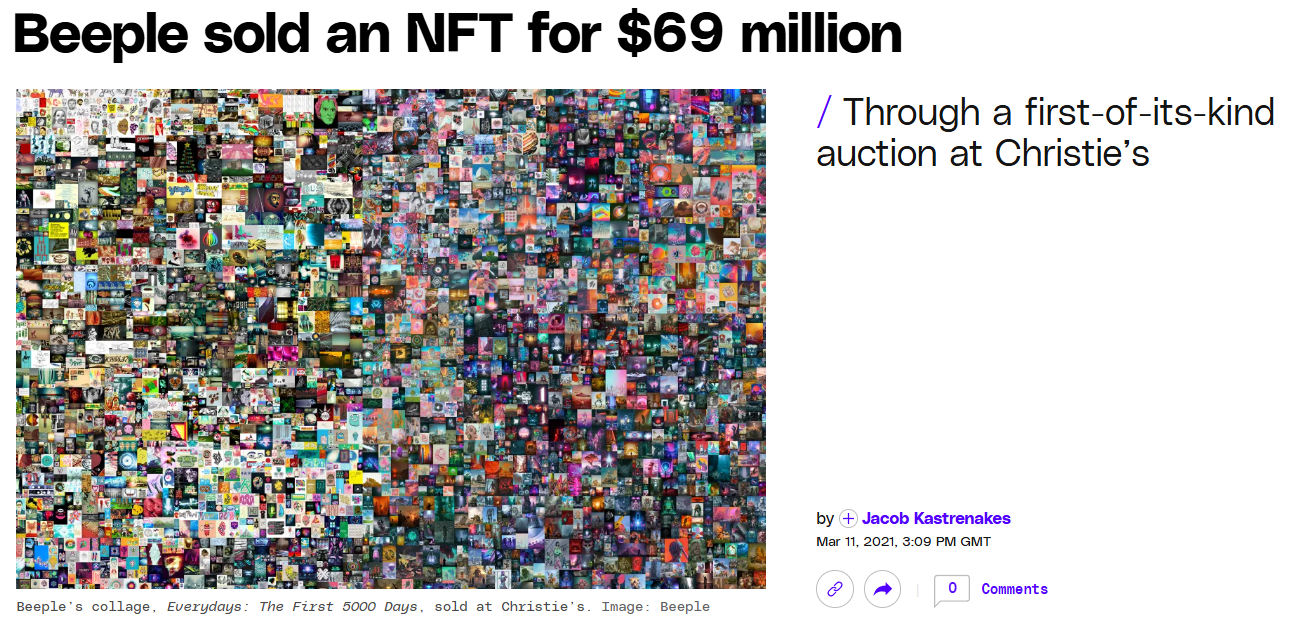

In 2021, Beeple, a digital artist who had posted work every day since 2007, sold an NFT artwork at Christie’s for $69 million. It was the first time a traditional auction house had given this level of attention to a digital piece, and the sale pushed NFTs into global headlines almost overnight.

This shift wasn’t only about high-profile sales. Marketplaces like OpenSea, Rarible, and Foundation saw sharp increases in users, and creators across art, music, gaming, and VR began exploring NFTs as a new way to distribute their work.

At this point, the excitement was still manageable. Prices rose, attention grew, and NFTs were entering the mainstream for the first time. But this was only the beginning. The surge of interest throughout 2021 would soon turn into something much larger - and far more chaotic - than anyone expected.

As NFT marketplaces expanded and attention increased, trading activity rose sharply. Profile picture collections (PFPs) like Bored Ape Yacht Club, Pudgy Penguins, and later projects such as Azuki and CloneX became defining symbols of the space. For many, owning one wasn’t just about the artwork – it acted as a form of online identity and as a membership pass to exclusive communities.

This period also saw a huge wave of mainstream involvement. Celebrities, athletes, musicians, and major brands began buying NFTs or even launching collections of their own. Visa purchased a CryptoPunk, Adidas released collaborations with several projects, and social media was filled with people using their NFTs as profile pictures.

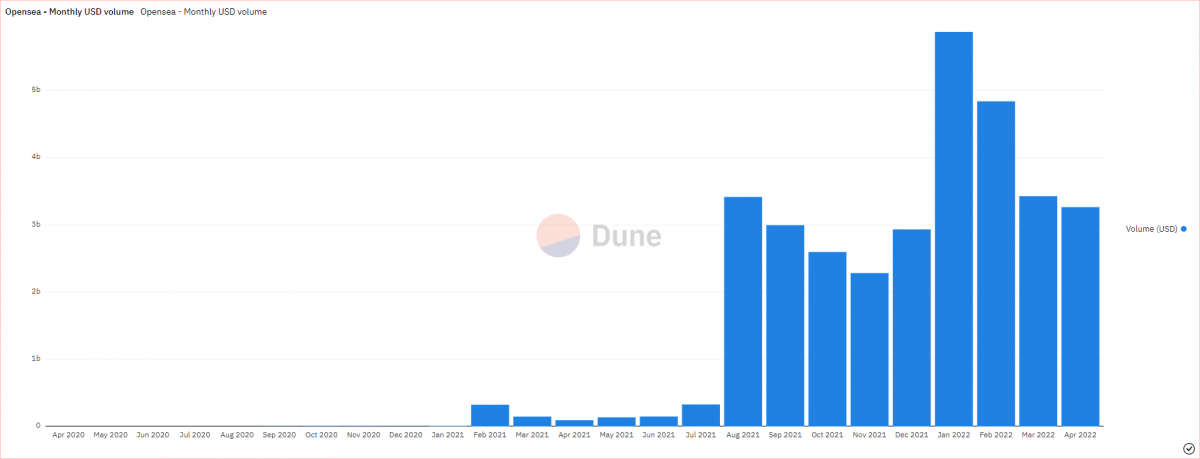

Marketplaces experienced their highest levels of activity, with monthly trading volumes in the billions of dollars. New collections appeared by the hour, many selling out within minutes. For most people in the space, the growth was unlike anything they’d seen – trends were shifting constantly, and keeping up became part of the experience.

But this rapid growth created weaknesses. New projects were launching far faster than new buyers were entering the market, or current buyers could keep up with. On top of this, speculation drove most price movements, and many teams couldn’t deliver what communities expected. From the outside, the market looked strong, but the conditions that caused the surge were beginning to change.

By mid-2022, the pace of growth in the market was starting to show its limits. As more collections launched and speculation intensified, the gap between supply and genuine demand became visible. New projects struggled to maintain any attention after their initial mint (the moment a new NFT is created and sold), and the excitement that had driven the previous boom started to feel hard to sustain.

Issues within the ecosystem became clearer as trading volumes remained high, but the quality of new projects decreased. Rug pulls (when founders disappear with the money after selling the NFTs), failed collections, and unrealistic roadmaps began to erode trust. Communities that had formed around speculation and rapid price increases found it difficult to manage expectations without markets rising. The number of participants was still huge, but sentiment was shifting, and confidence was no longer as strong as it had been.

At the same time, broader market conditions began to turn. Crypto prices fell, liquidity started to dry up, and the wider economic environment grew more uncertain. NFTs, which had risen mostly on momentum and optimism, felt this impact quickly. Collections that once saw constant activity now experienced serious declines in trading, and enthusiasm cooled across many parts of the market.

The signs were early, but clear. Less liquidity, fewer new buyers, fading interest. It wasn’t a full downturn yet, but the cracks had started to show.

By 2022, those early cracks in the NFT market had widened. Trading volumes fell sharply as liquidity across the crypto market halted, driven by major events like FTX’s implosion and rising interest rates. Many collections that had once been highly active saw interest fade almost overnight. What had been a rapidly expanding market shifted into one defined by declining activity and falling prices.

The collapse wasn’t driven by a single event, but rather by a combination of oversupply, weakening demand, and a loss of confidence. Hundreds of thousands of projects were launched during the boom, but very few could sustain long-term engagement. As speculation slowed, floor prices dropped, trading activity thinned, and communities became inactive.

Crypto was entering a prolonged downturn, with investment flowing into the market decreasing, while economic uncertainty pushed buyers away from riskier assets. Platforms that had reported record volumes now saw those volumes fall by more than 90%, and sentiment shifted from excitement to scepticism.

By the end of 2023, the rapid expansion that had defined the previous years had been unwound. What remained was a smaller, quieter market – and a clearer view of the projects still building despite the conditions.

As the market unwound, it became clear which NFT projects were built on more than just speculation. While thousands of collections disappeared, a small group continued to operate and grow. Their survival reflected stronger leadership, clearer branding, and communities that stayed even as trading activity declined.

Pudgy Penguins became one of the clearest examples. After a difficult start, new leadership rebuilt the project around brand development rather than price movements. Physical products, retail partnerships and licensing deals shifted the focus towards long-term IP, allowing the project to grow during this period.

Other established collections also maintained momentum. Projects with durable communities and recognisable IP were able to keep building, even as sales fell.

What set these survivors apart wasn’t high floor prices - it was consistency. They continued to release products, communicated with holders, and moved towards long-term goals.

I’ve been involved in NFTs since 2021, mainly through the creative side – contributing to NFT gaming, 3D work, and PFP artwork. Being inside these teams and communities meant I saw the rise and decline of the market directly, rather than just being an observer. I watched how quickly interest could build around a new idea, and how just as quickly it could disappear once attention shifted.

Holding NFTs myself, including pieces from collections like Pudgy Penguins, made the volatility more real. It became clear to me which projects were built on strong foundations and which relied on speculation. Seeing that contrast in real time shaped my understanding of the space today.

This experience is what informed this article. The NFT cycle wasn’t just some market event – it was shaped by the people inside it. Communities, creators, and collectors were the ones driving momentum long before any companies paid attention. Watching how quickly something could be built, and how equally fast it could unravel, revealed to me just how dependent the entire movement was on individuals and their shared beliefs. It was a cycle powered by people – and when the people shifted direction, the market followed.

With the speculative boom in the past, NFTs exist in a far quieter market than before. It is smaller, more selective, and mostly removed from the attention that once defined it. Yet the core ideas that sparked the initial excitement are still in use, even if they now sit on the sidelines.

The clearest legacy is digital ownership. NFTs introduced a simple way to verify who owns a digital asset and track its history – ideas now influencing gaming, digital identity, and other on-chain applications. The technology has continued to evolve, even as the narrative around it has faded.

A small number of projects have demonstrated that their IP can extend beyond crypto. Only a few made this transition, but those that did have provided a clearer example of what a sustainable, NFT-born brand can look like.

Taken together, the rise and fall of NFTs resembles an early exploration rather than a finished technology. The hype cycle has ended, but the ideas it introduced continue to develop. The story now is less about speculation and more about this technology finding practical uses across gaming, identity, and other digital systems – not just as NFTs.