In August 2023, there was a moment following the US Treasury’s auctioning of $23 billion worth of 30-year bonds, triggering an immediate jump in yield, fuelling speculation that the market could accommodate the auction. This premium term (also known as the ‘term premium’) may be quite unheard of for those new to the FICC landscape, but at first, it is a simple concept in fixed income terms explaining the pricing of duration risk. To clarify, this type of risk refers to the exposure that a bond holder faces when interest rates rise. This is because newly issued bonds will have higher yields, resulting in the price of previous bonds falling, due to lower rate of relative return. Owing to the years of the Federal Reserve’s dovish stance on monetary policy, such as extended Quantitative Easing, this term had seemingly vanished.

Yet, term premiums have once again returned to the treasury bond market headlines, arguably to the extent that the success of any FICC investor depends centrally upon their understanding of this topic. To understand why, it’s essential to get a fundamental understanding of what yields are and what bonds and term premiums truly represent.

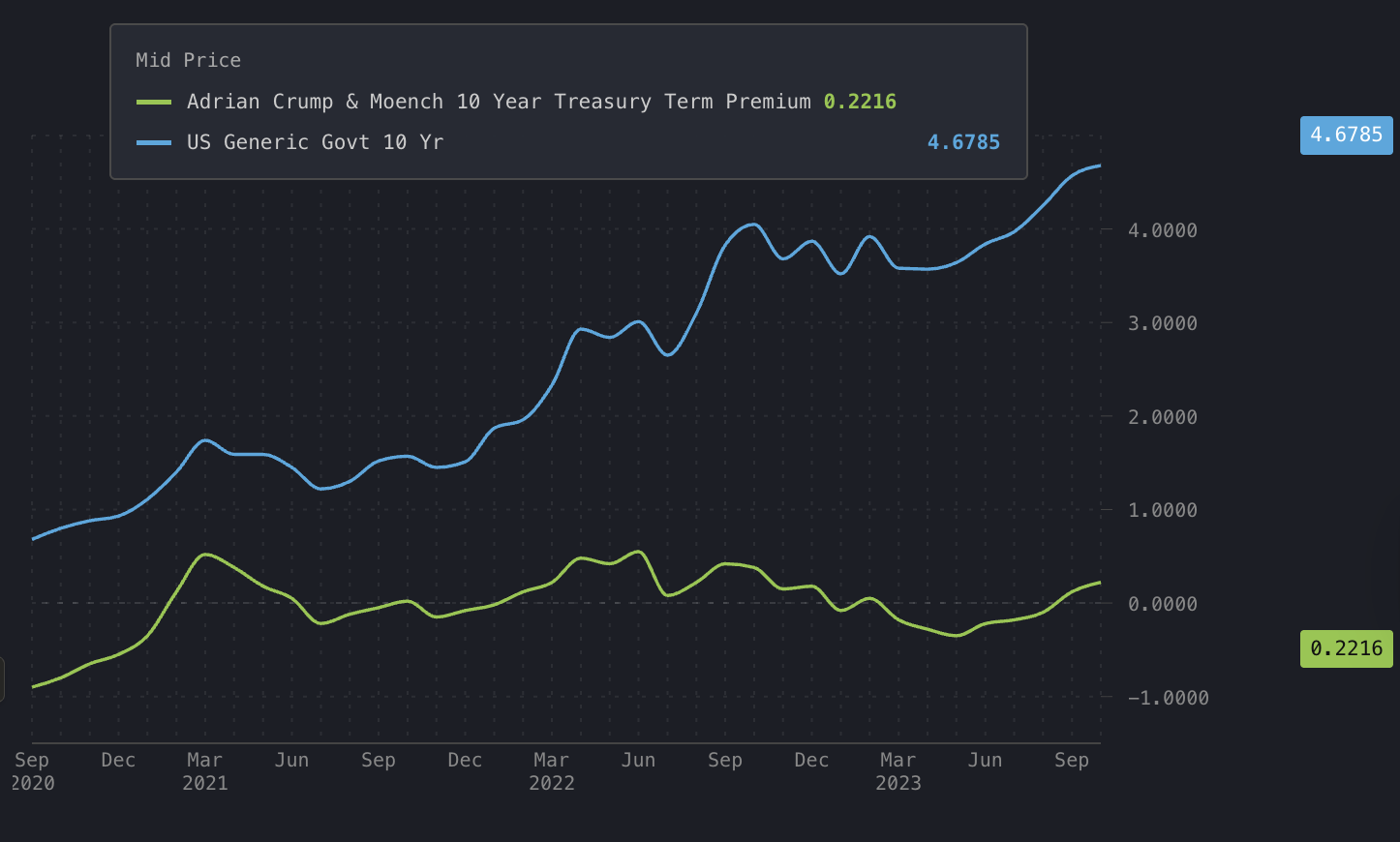

In fixed income markets, a yield is the term that is used to denote the income returned on an investment, in comparison to the current market price of that investment, as a percentage. When there is heightened duration risk, markets can often demand compensation, a greater reward, to hold risk for an extended period of time. This is exactly the concept of term premiums, when investors desire additional return in exchange for holding investments long-term, rather than investing in the equivalent short-term bonds. Continuous quantitative easing and low-interest rates from 2010-2020 led by the US Federal Reserve and similar initiatives by the ECB and BoE drove term premiums negative. Yet as of early 2026, term premiums stand at +0.59% points, a new record high since 2019, and expected to rise further, as indicated by the historical trend on the diagram (Figure 1) below.

You may wonder what’s caused this recovery of term premiums, and it stems once more from the decisions of the US Federal Reserve. The shift in term premium trends is not just a bubble, or expectation-led hype, but centred around a fundamental reprice of the market risk in bonds. This is because of the Fed’s decision to reduce its balance sheet by almost $1.7 trillion, increase in fiscal deficits, and uncertainty around inflation figures, which shadows doubt on fixed-income returns. For a long time now, most investment decisions had a zero term premium strategy, but in light of its revival and greater uncertainty in markets, such as heightened liquidity risk, this approach is fast becoming outdated, with fixed income investors needing to adapt their portfolios.

To comprehend why this change in dynamics is so significant, we must observe the historical patterns in bond markets. In the 2010s, post the infamous 2008 financial crisis, the Federal Reserve undertook large-scale quantitative easing (QE) under a zero-lower-bound interest rate scenario, leading to purchases of more than $3.5 trillion worth of treasury bonds. Consequently, with demand for safe assets surging and QE flooding the bond market, term premiums were almost eliminated throughout the 2010s, to the point where in 2019, models suggested 10-year term premiums to be roughly -0.8%. This meant investors were accepting lower yields on long-term bonds than the corresponding shorter-term bonds. This is intuitively unconventional, especially factoring in traditional bond market logic over duration risk. This is best explained by thinking about it from the perspective of fund managers, where it becomes clear that choice was limited. The Federal Reserve was continually purchasing bonds, leading to bond scarcity and falling yields. A pension fund manager in this position would need to find investments that fit the duration of their liabilities, and as a result, markets ended up in a situation where 10-year treasury bonds yielded even below the federal funds rate.

Returning to early 2026, however, investors once again find themselves having to factor in term premiums due to three primary reasons. Firstly, quantitative tightening (QT) has been taking place since 2022, as the Fed continues to reduce its balance sheet by over $1.7 trillion. This has led to an increased supply of bonds to the point where it can be considered an excess due to a lack of private demand. Secondly, fiscal deficits have swelled, with the US deficit exceeding $1.7 trillion in 2023, and over $1.8 trillion in 2024, sparking an even further need for Treasury bond issuance to control national debt within a post-Covid economy. Lastly, the inflation picture since 2020 has been one of persistent volatility, with unpredictability and CPI deviations at all-time highs. This invariably reflects in duration risk, as investors require compensation from inflationary risk of erosion to their real returns in the long-run. However, despite the heightened risks due to volatility, these conditions all suggest the risk/reward trade-off for long-end exposure is not worth it right now according to BlackRock’s Chief Strategic Income Fund Manager, Russ Brownback suggesting that yield trends are once more returning to their norm.

Now for the key focus of this article: How should investors adapt to this phenomenon?

For larger-scale institutional investors, term premiums will sharply alter investment strategies. Take pension funds: while their existing long-duration Treasury holdings appreciated handsomely during the QE era, negligible term premiums meant that new allocations to 20-year bonds offered little yield advantage over short-term alternatives - stripping away the very compensation that makes long-duration bonds worth holding. Yet now, these funds will appreciate the need for short-term investing, given that term premiums mean even 10-year bonds have similar yields to much longer-term ones.

The story is similar for retail investors, too, who also find themselves recalculating their bond portfolios. Where bond returns were once solely dependent on central bank rate changes, leading to short-run price changes in the QE era, now, returns come from income via term premiums instead. Thus, if term premiums continue to rise, long-duration bond holders will have to adapt their strategy as shorter-run bonds also earn greater returns.

One thing this does not mean, however, is that investors must pick sides, as the most tactical investors already appreciate that strategies involving a mixture between shorter and longer-term bonds are more viable. On one hand, term premiums allow them to capture long-term bond rate returns, whilst reducing liquidity risk by also holding shorter-term bonds. Some investors may want to maximise term premium returns under the volatile environments that may exist, opting to concentrate investment into 5-7-year bonds, to extract maximum returns.

Whichever route investors may take, though, the way term-premiums have seemingly revived, recessions could draw curtains at 2x speed. The risk of recession to term-premiums has once been seen in 2008, with QE measures eliminating them, and with many analysts predicting another financial crisis at some point within this serve as a significant risk to large-scale long-term bond investments. As a result, eyes must remain fixed upon the US Federal Reserve’s balance sheet, fiscal deficits and inflation trends to see whether term premiums ‘mature’ in investment strategies, or are ‘redeemed’, as current trends suggest favourable trends towards term premiums. Finally, it’s naive to think term premiums will only affect fixed income investors - elevated term premiums reduce the Federal Reserve's influence on long-term borrowing costs, a central monetary policy tool. Thus, we may also be in a transformative period for monetary policy itself.