The contrasting experiences of Hong Kong, Denmark, Argentina illustrate the divide clearly, and they provide a useful framework for assessing whether a country like Iran could realistically stabilise its currency through a pegged regime.

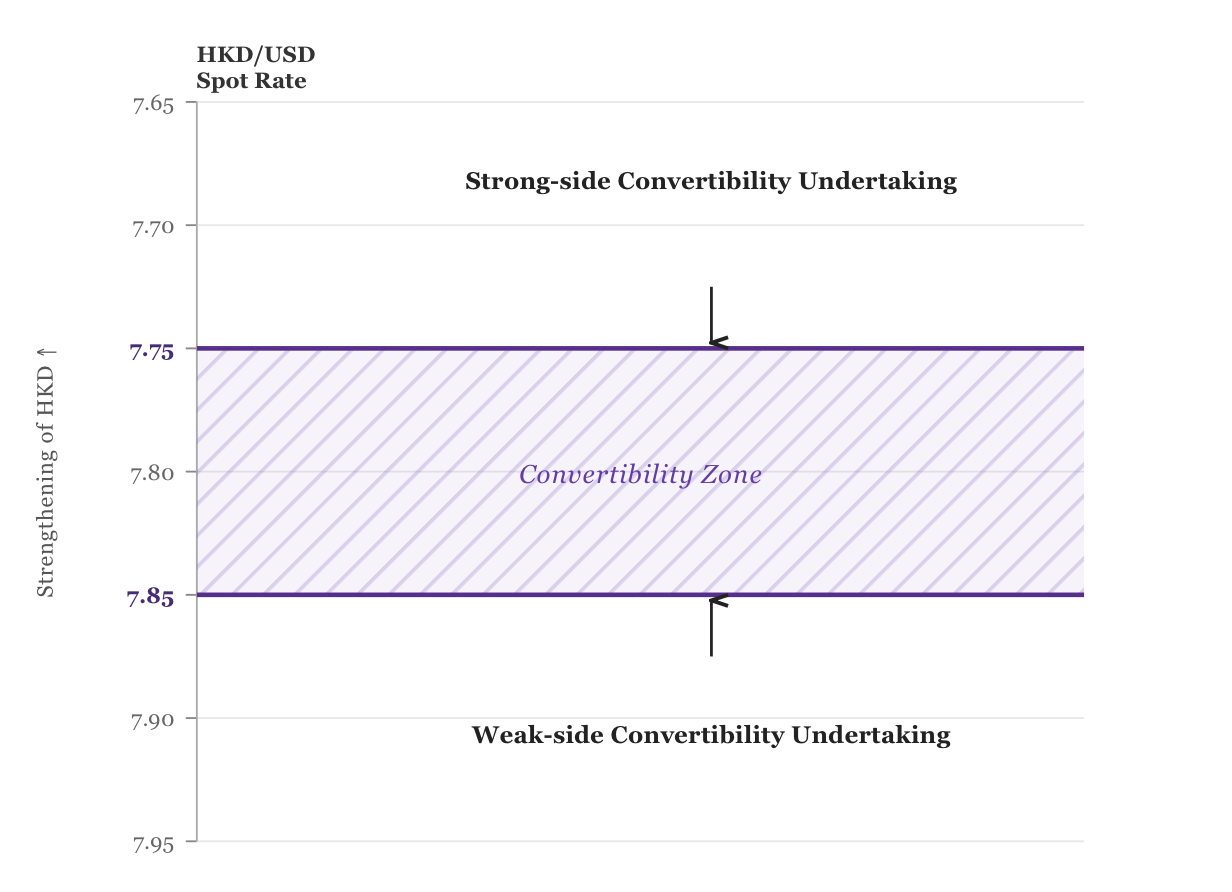

Hong Kong remains the benchmark for fixed exchange rates regimes. Since 1983, the Hong Kong dollar has been linked to the US dollar which is anchored by the discipline of the Hong Kong Monetary Policy, rather than left to market drift. It's important to note that this is not a discretionary peg which is supported by signalling or gradual adjustment. The peg is designed to remove discretion thoroughly. Under the Hong Kong Monetary Policy, the monetary base is fully backed by the US dollar assets. The monetary base highlights how any change in domestic liquidity must certainly be matched one for one by changes in foreign reserves. The HKMA must ensure that the peg is enforced through explicit Convertibility Undertakings. In essence, this is just a commitment the central bank makes which guarantees exchange of its currency for another at a fixed demand. In the case of the HKMA commits to sell Hong Kong dollars at 7.75 per US dollar and to buy them at 7.85, creating a narrow convertibility zone. Moreover, it is clear how the convertible undertaking turns Hong Kong’s peg from a policy choice into a binding market constraint. This mechanism is also laid out clearly in the HKMA’s explanation of the Linked Exchange Rate System and illustrated in the diagram below showing the strong side and some weak sides of the convertibility points.

The diagram also portrays that under Hong Kong’s peg, the exchange rate is the least flexible variable. We must stress how pressure is instead absorbed by liquidity and short-term interest rates, meaning stress appears first in money markets rather than in spot foreign exchange markets, reinforcing the credibility of such a regime which is built on discipline rather than discretion.

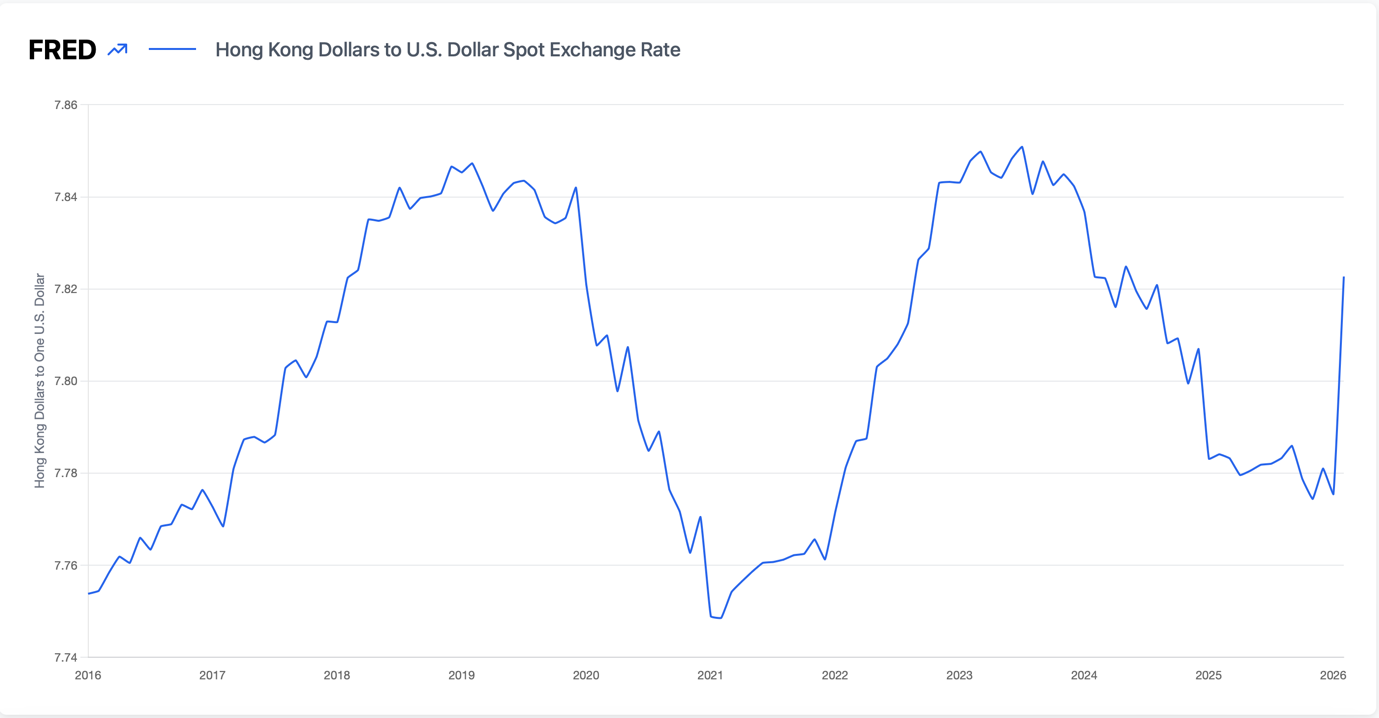

The more interesting takeaway is how the mechanism above is seen in the USA/HKD spot exchange rate series from the St. Louis Fed (FRED), which shows how currency remains tightly confined within the 7.75-7.85 band over many years, even during periods of financial uncertainty and global stress such as COVID-19. This is all depicted in the line graph above.

The line graph points out small oscillations inside the band which represent market pressure, but since there is no sustained breakout adjustment occurs through liquidity and interest rates rather than the exchange rate itself. Ultimately, the flatness of the line is not calm; it is mechanical credibility in action.

The Danish Krone is fixed with ERM II at a central rate of 7.4603 per euro and is defended by the Danmarks Nationalbank. What makes this peg interesting is that Denmark is not part of the eurozone, yet it has voluntarily subordinated its monetary policy to exchange rate stability.

The commitment is showcased in the EUR/DKK exchange rate diagram, which shows the Krone fluctuating within a very range around its central parity.

The line graph reinforces how the peg is credible when put into practice. Even during periods of intense global stress like COVID-19, deviations are often small and short-lived, and therefore, the exchange rate quickly reverts. Markets base prices in the expectation of consistent policy defence and not by meaningfully testing the peg. As a result, stability is achieved not through market calm, but through credibility, with adjustment occurring through policy rather than sustained exchange rate movements.

Until now, we have seen how currency pegs act as powerful anchors. Now it is time to see how when the tides turn, those same anchors can start dragging economies underwater.

Argentina provides us with a canonical example of how pegs fail when fundamentals start to diverge. During the early 1990s, Argentina decided to operate a hard currency board under the Convertibility Plan which aimed to combat hyperinflation. This involved fixing the Peso one to one against the US Dollar. Initially inflation collapsed, and confidence returned. However, over time, fiscal imbalances and external vulnerabilities accumulated.

Examples of macroeconomic imbalances consist of persistent government budget deficits financed through rising debt, most of which is predominately dominated by in US Dollars and an overvalued real exchange rate which undermines the shear export competitiveness.

More consequences of the peg collapse are documented quantitatively in International Monetary Fund Article IV consultation data following the abandonment of the currency board in early 2002. The peg's collapse was economically corrosive as the IMF reported that in 2002 real GDP contracted by roughly 11%, with inflation climbing up to around 26%. These adverse supply side shocks lead to major breakdown in macroeconomic stability which has a great impact on economic welfare.

It is worth bearing in mind that Argentina’s experiences do not inherently imply that fixed exchange rates are inherently flawed. What it demonstrates is that a peg cannot survive when fiscal policy, debt dynamics, and external balance becomes inconsistent with the exchange rate commitment. When markets finally recognised the mismatch, and without credibility, no peg endures.

So far, we have seen how currency pegs can be remarkably effective anchors, but on the flip side when conditions shift, the same anchors can drag economies under.

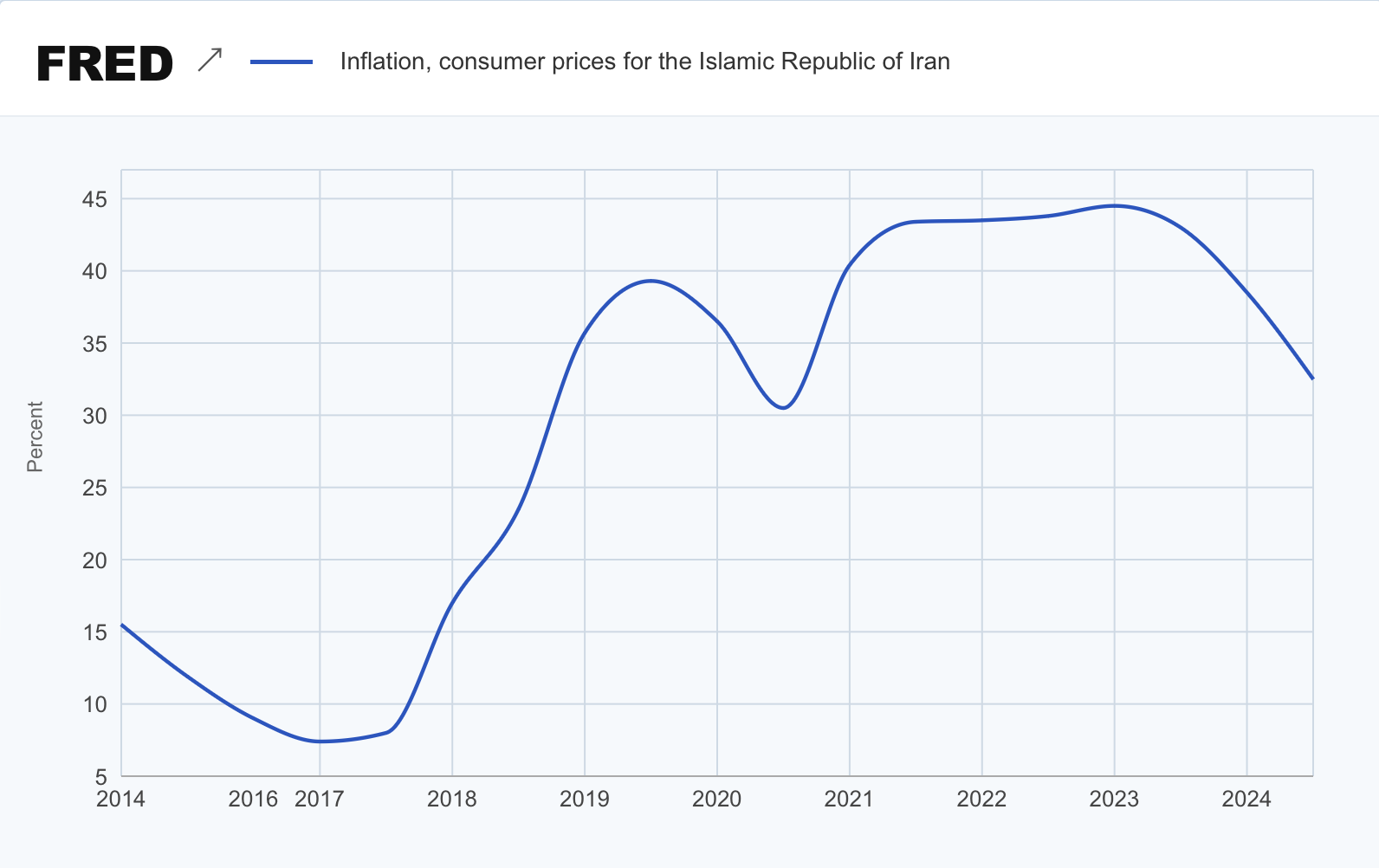

That being said, let's look at a nation like Iran. Having experienced sustained currency depreciation and inflationary pressure, we could perhaps argue that a peg can be attractive as a way to impose discipline and anchor expectations.

The graph shows that Iran has experienced significantly high and volatile inflation, rising from single digits around 2016-2017 to the mid 30% and low 40% range after 2018. This rapid increase in inflation shows erosion of purchasing power, reflects the pressure on living standards and indicates how real income decreases. From this data, a currency peg could be a strategic short term nominal anchor, helping to alleviate expectations, but if there is no fiscal discipline and credibility it would be difficult to sustain and therefore vulnerable to breakdown.

Ultimately, a currency peg could be beneficial for Iran as a later stage policy, following guidance for fiscal discipline, sustained disinflation, and restored credibility. Introduced prematurely, it would be more likely to fail than to anchor stability.

Hong Kong shows us what happens when rules dominate discretion. Denmark shows that credibility can survive even when monetary independence is willingly surrendered. Argentina shows that when fundamentals diverge from promises, pegs collapse rapidly and painfully. For Iran, the message is clear. A peg is not a magic solution, yet rather It is a test of a nation's fiscal coherence, and political resolve. Therefore, this raises the vital question - if these fundamental conditions are not adhered to, does it still make sense to introduce a peg?