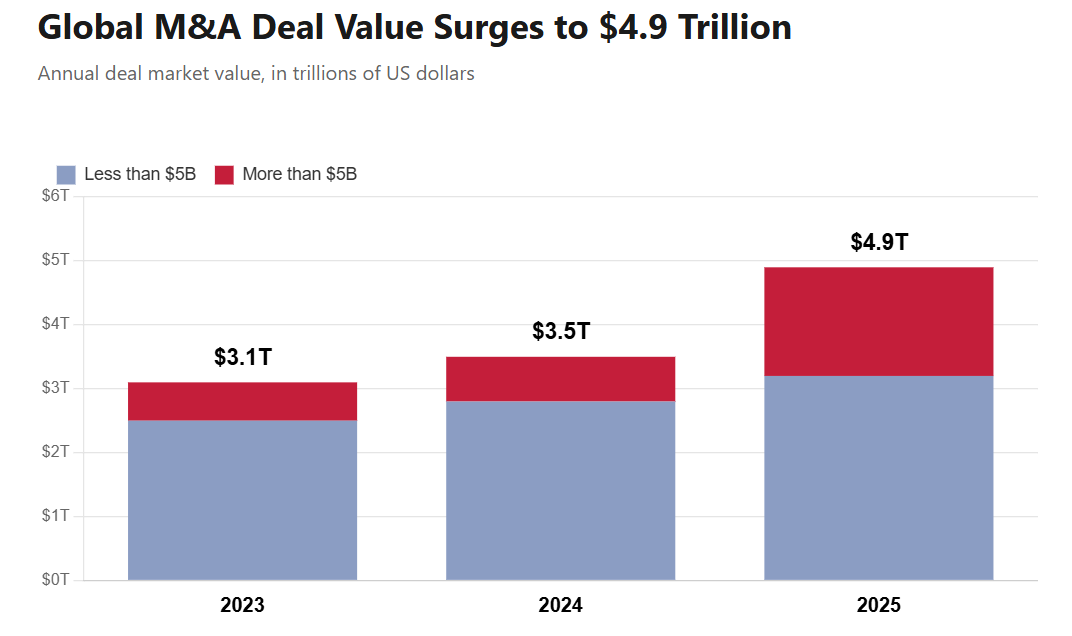

Mergers and acquisitions are one of the most powerful and most persistently used tools in corporate strategy. The rationale is straightforward: buy another business, unlock synergies, accelerate growth, and deliver returns to shareholders. In practice, the reality is far less clean. Yet deal activity shows little sign of slowing. According to Bain & Company, global M&A deal value reached $3.5 trillion in 2024, up 15% year-on-year and consistent with mid-2010s levels, while deal volume rose 7%, reversing two years of consecutive declines. In 2025, the market accelerated further still, with estimated deal value climbing 40% to $4.9 trillion, on track to become the second-highest year on record.

The scale of this activity stands in stark contrast to what the academic evidence tells us about outcomes. A statistical analysis of over 40,000 acquisitions worldwide across four decades found that 70–75% of deals fail, as stated by professors Baruch Lev and Feng Gu in The M&A Failure Trap. Similarly, KPMG's analysis of more than 3,000 public-to-public deals above $100 million between 2012 and 2022 found that 57.2% of acquirers ultimately destroyed shareholder value. As such, M&A has clearly earned its often quoted title as "a mug's game."

This raises an obvious and important question: if the odds are this bad, why do companies keep pursuing it? Part of the answer lies in incentive structures; executives are often rewarded for deal completion rather than deal outcomes, and investment banks earn fees regardless of long-term performance. Part of it is competitive pressure; when a rival acquires, standing still can feel riskier than acting. And part of it is simple overconfidence, with many believing that their deal will be different, that their management team will extract the synergies others failed to find.

For equity investors, the implications are material. When a company announces an acquisition, the market is pricing the probability of a known base rate of failure. Understanding why most deals underperform is therefore a core input to assessing whether an acquirer deserves a premium or a discount.

The most common and most damaging of ways an acquisition can go wrong is overpaying. As Professor Nuno Fernandes of IESE Business School concludes in his book The Value Killers (2019), if an acquiring company overpays for a target, it will destroy value even if every single projected synergy materialises. This is the central mechanism of M&A failure, and it operates before integration has even begun. Acquirers typically pay a significant premium above a target's pre-announcement share price to secure shareholder approval, often in the range of 20–40%. That premium has to be entirely funded by value created post-deal through cost savings, revenue uplift, or operational improvements. When those gains are overestimated, or when the premium simply starts too high, the deal is effectively underwater before it has even begun.

Why do experienced management teams routinely make this mistake? Behavioural finance offers a compelling explanation through two closely related concepts: hubris and the winner's curse. The hubris hypothesis, first formalised by economist Richard Roll in 1986, holds that overconfident managers fall prey to the winner's curse and systematically overbid when acquiring other companies. The mechanism is intuitive: in a competitive bidding contest, the party that most overestimates the value of the target tends to bid higher than its rivals and is therefore more likely to win. However, the acquirer most likely to win is often the one most wrong about what the target is actually worth. Empirical research bears this out at scale. A study by Varaiya and Ferris examining 96 acquisitions completed between 1974 and 1983 found that the winning bid premium overstated the market's estimate of expected takeover gains on average, and the cumulative excess return to winning bidders was significantly negative, averaging -14% in cases where the premium exceeded the expected gain.

The problem is further compounded by incentive structures that actively encourage overpayment rather than penalise it. As Lev and Gu note in their analysis of 40,000 deals, many companies pay their CEOs a substantial bonus simply for completing a deal, and executive compensation typically rises after acquisitions because company size is a major determinant of pay. In this environment, a disciplined walk-away is not just psychologically difficult, it can be financially costly to the executive making the call.

The category of deal most at risk is also the largest by volume. Unrelated or conglomerate acquisitions now account for nearly 40% of all deals globally, yet they offer no industry synergies by definition. An investor wanting cross-sector diversification can achieve it far more cheaply by buying shares directly. When a corporate acquirer does it instead, they hand the target's shareholders a large premium for something the market was already pricing in, generating immediate, structural value destruction for their own shareholders.

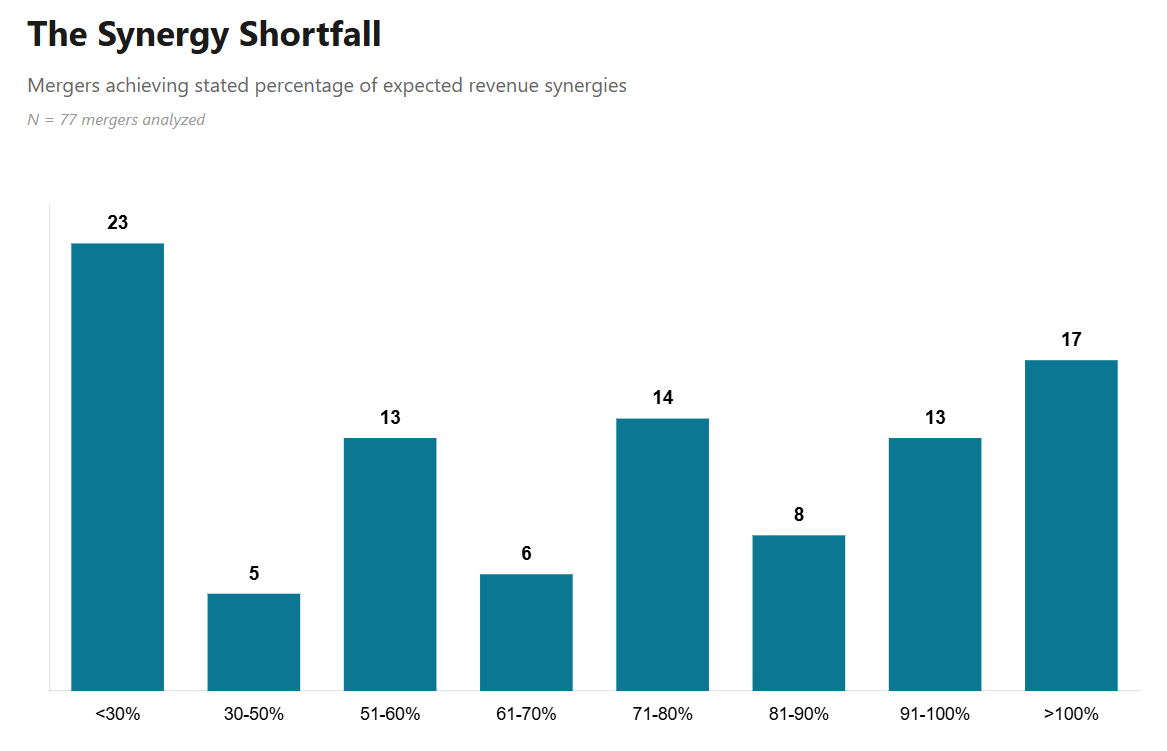

Even when overpayment is avoided, deals regularly collapse at the execution stage. The synergies that justified the acquisition premium: cost savings, revenue uplifts, operational efficiencies, frequently fail to materialise on the timeline or scale promised. McKinsey research found that in roughly a quarter of all mergers, cost synergies are overestimated by at least 25%, a miscalculation that can translate directly into a 5–10% valuation error. The issue is partly structural: deal teams work under time pressure with limited access to the target's internal data, making bottom-up synergy estimation almost impossible before signing. Assumptions about the timing and sustainability of synergies are routinely too optimistic, causing near-term earnings and cash flow metrics to appear more attractive than they genuinely are.

Then comes integration. Cultural clashes, delays in combining systems, and leadership misalignment are among the most frequently cited causes of integration failure, and they are also the most consistently underestimated. Microsoft's 2014 acquisition of Nokia serves as a textbook example: the deal failed due to overestimated cost synergies, underestimated operational complexity, and an unrealistic assessment of Nokia's revenue potential given its declining market share against iOS and Android.

The persistence of M&A activity in the face of such consistently poor outcomes is itself revealing. It speaks less to the strategic logic of any individual deal and more to the structural forces that drive dealmaking regardless of the odds: misaligned incentives, competitive anxiety, and the enduring human conviction that this time will be different.

For investors, the takeaway is not that acquisitions are always destructive, but that the burden of proof should be high. A compelling deal thesis requires more than a plausible synergy story; it requires evidence that management has the discipline to walk away from a bad price, the operational depth to execute integration, and a track record that earns the benefit of the doubt. In the absence of those qualities, the base rate is unforgiving. Most acquirers don't fail because they chose the wrong target. They fail because they paid too much, promised too much, and underestimated how hard the hard part actually is.