Currencies within the Gulf Co-operation Council have remained remarkably stable despite the conflict surrounding them. This is because all member states, except Kuwait, maintain fixed exchange rate pegs to the US dollar, including Bahrain, Oman, Qatar, Saudi Arabia and the UAE. Kuwait is the exception because its currency, the Kuwaiti dinar, is not pegged solely to the US dollar but instead to a basket of currencies. This allows Kuwait greater flexibility to stabilise its exchange rate against multiple trading partners, rather than being fully exposed to movements in the dollar. In Saudi Arabia its riyal (SAR for short) has been pegged at a rate of 3.75 SAR to 1 USD since 1986. The Saudi Arabian Monetary Authority (SAMA) does not allow the currency to float freely. Instead, if upward or downward pressure builds, it will intervene immediately to maintain its peg.

Saudi Arabia is able to sustain this system because of its substantial foreign currency reserves worth $450 billion. It produces 10 million barrels of oil per day, generating $179 billion in oil export revenue. As oil is a key input in all production processes, there is consistent global demand for it, allowing Saudi Arabia to accumulate a wide range of foreign currencies that can be used to defend its peg.

Historically, these foreign currency reserves were overwhelmingly made up of US dollars due to the petrodollar system, where Saudi Arabia priced oil exports exclusively in dollars. This ensured a constant inflow of dollar revenue, reinforcing both the Kingdom’s ability to defend its currency peg and the global dominance of the dollar. More recently, however, Saudi Arabia has shown a willingness to accept alternative currencies, such as the euro and Chinese yuan, for oil transactions. While this reflects a strategic effort to diversify its international relations and reduce reliance on a single currency, it also provides evidence of waning American economic influence, contributing to the broader trend of de-dollarisation.

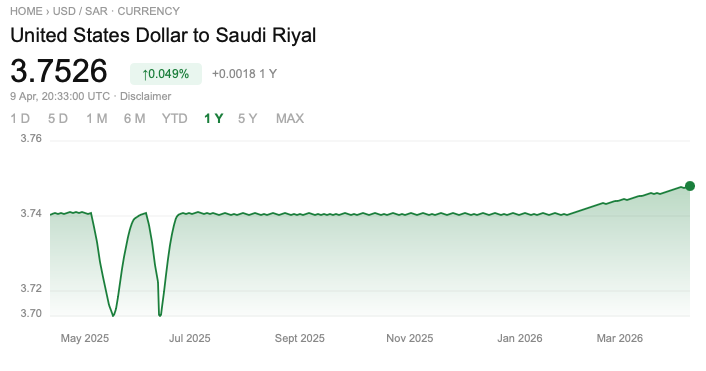

Following the start of Operation Epic Fury, investors may have reacted by selling Saudi riyals in favour of safer assets such as the US dollar. This would increase the supply of riyals on the foreign exchange market, causing its value to depreciate below its peg. In response, the SAMA intervenes by selling its foreign currency reserves to buy back its own currency. This will reduce the excess supply of the riyal while simultaneously increasing demand for it, propping the value back up to 3.75 SAR. This is evident in Figure 2, demonstrating how the exchange rate may experience sharp fluctuations, but the peg consistently restores stability. This dynamic occurred during the first two weeks of the war, when foreign institutional investors sold $8 billion in Saudi equities. As these transactions take place on the Saudi stock market, investors would have received riyals. However, during the war in the Middle East, most foreign investors are unwilling to hold SAR, prompting them to convert their holdings into US dollars or Swiss francs. Despite this, the peg remained intact. This reflects both the scale of Saudi Arabia’s foreign currency reserves and the relatively limited magnitude of capital outflows. More importantly, it shows strong confidence and credibility in the Gulf financial systems, with investors trusting the SAMA will maintain its peg.

The Iranian rial has been on the decline for years because of heavy reliance on oil exports and sanctions. However, recent military intervention has acted as the final blow. In the aftermath of Iran’s revolution in 1979, the US dollar was equivalent to 70 Iranian rials (IRR). Today it is equivalent to 1.4 million IRR representing a 20,000x depreciation. While this collapse may appear sudden, it is the result of a prolonged erosion in economic stability, mainly driven by US sanctions. These sanctions are linked to Iran’s nuclear programme and its support for militant groups, such as Hamas, Hezbollah and Houthi Rebels. These restrictions have significantly constrained Iran’s access to global financial systems and foreign currency inflows.

Iran’s economy has historically relied on oil production generating, $23.2 billion from its exports in March 2025, which roughly accounts for 57% of the country’s total export revenues. The United States has acted on these vulnerabilities by imposing sanctions that directly forbids US individuals and companies from engaging in business with Iran, while also pressuring other countries to reduce their purchases of Iranian oil. The EU has implemented similar measures due to Iran’s poor human rights record and its active role in supplying drones to Russia for the war in Ukraine.

As a result, Iran is suffering huge economic costs. To circumvent sanctions, it is forced to sell oil at discounted prices, losing 20% of its oil export revenue. Most of this is done via the shadow fleet, which is a network of old oil tankers operating with obscured ownership and disabled tracking systems. While these methods allow Iran to bypass international sanctions, they come at a cost due to the legal risks involved. The Islamic Revolutionary Guard Corps (IRGC), a political and military organisation, has expanded into Iran’s oil industry. Originally established to protect the Islamic Republic, it now plays a central role in organising these shadow fleet operations and controlling the allocation of the foreign currency they generate.

Oil exports have been redirected to Asian markets, with China being the largest consumer importing over 90% of Iranian oil. This sounds good in practice as Iran has secured a strong and reliable buyer; however, it does not fully offset the broader financial constraints imposed by the sanctions. Normally, global oil trade is conducted in US dollars using the SWIFT banking system (Society for Worldwide Interbank Financial Telecommunication), which facilitates international financial transactions. However, Iran’s exclusion from the US banking system and ban from SWIFT in 2018 have restricted its ability to trade in dollars. So, if China did buy Iranian oil in USD there is a high risk that the transaction would be blocked or seized. Therefore, China pays in yuan (RMB) which completely avoids the US financial system. The catch is that the RMB lacks the global liquidity and acceptance compared to the USD. This is crucial because only widely trusted currencies like the US dollar can be easily used in foreign exchange markets to stabilise a currency, whereas the yuan is harder to use. As Iran has less USD and more yuan, it will find it harder to manage its currency.

Iran operates under a managed floating exchange rate system, meaning the value of the rial is determined by market supply and demand, but the Central Bank of Iran (CBI) intervenes to limit volatility when appropriate. However, as political tensions intensified in late 2025 and the current conflict with the US and Israel, the system has come under severe pressure. A sharp rise in capital flight, estimated at $40 billion, led to a surge in the supply of rials on the market, driving rapid depreciation. This collapse is evident in Figure 3. For context, in 2023 the price of a loaf of bread was 30,000 IRR. At this exchange rate, £1 could buy just under 60 loaves. With limited and weak foreign currency reserves, the Central Bank of Iran was unable to absorb the excess supply of rials flooding the market. All in all, Iran could not stabilise the exchange rate, causing its currency to collapse.

In conclusion, the currency divide highlights the importance of political alliances over a country's geography. The Gulf economies have anchored themselves to the United States through dollar pegs, and in return, have ensured their currency remains stable amidst conflict. In contrast, Iran’s alignment with China and Russia has left it exposed to sanctions and vulnerable to economic isolation, contributing to the collapse of its currency. The key takeaway from this currency divergence is the enduring power the US gains from issuing the world’s dominant reserve currency. It can capitalise on this by using the dollar as a financial weapon, capable of shaping the economic future of nations.