In terms of issuance, gilts (UK bonds) commonly range from 10 years to around 50 years, going up to 55 years. For these debt owners, this is relatively good, as they’re protected from fluctuations in interest rates, and these bonds provide predictable cash flows that match their long-term liabilities. However, the UK Debt Management Office (DMO) has decided to shift away from issuing these long-dated bonds to more short-term borrowing (for context, the DMO is a UK government agency responsible for managing public debt, cash and certain public sector funds).

A range of different factors is pushing this major change to the British government’s borrowing system. Events such as falling demand for these longer duration gilts, a preference to lower interest rates based on Rachel Reeves’ pro-growth agenda, and fear of recent market volatility are the biggest motivations for the DMO’s rewriting of gilt issuance, which will be explored throughout this article.

For decades, the main purchasers of long-dated gilts were domestic pension funds, as these financial products were most suitable for the risk appetite and outcomes required by pension funds. These institutions purchased 30-50-year bonds to match the timing of their long-term promise of paying retirees in the future, making these bonds the ideal, safe investment.

Pension funds reinforced this demand through what’s known as Liability Driven Investing (LDI). The basic idea is pretty intuitive. Instead of just chasing returns, pension funds invest in a way that makes their assets move in line with their future obligations to retirees. Since those liabilities stretch decades into the future and are highly sensitive to interest rates, funds use long-dated gilts, alongside derivatives like interest rate and inflation swaps to mirror that behaviour.

When interest rates fall, the value of future pension payments rises, because those payments are discounted at a lower rate. LDI helps offset this by ensuring the assets increase in value at the same time. Similarly, when rates rise, both the liabilities and the assets fall together, keeping the overall funding position more stable.

This is really about managing duration risk. Duration just means how sensitive something is to changes in interest rates. The longer the duration, the bigger the movement will be. Pension liabilities are very long-term, so they’re highly sensitive to rate changes. That’s why funds hold long-dated gilts: they behave in a similar way, helping keep things balanced.

After the 2008 Global Financial Crisis, interest rates were cut to near zero and kept there for years, with central banks like the Bank of England using quantitative easing to hold bond yields down. Following the COVID-19 pandemic, a mix of heavy government spending, supply disruptions, and rising energy prices pushed inflation higher, forcing central banks to raise interest rates sharply from 2021 onwards, to deal with rising inflation, and weak growth.

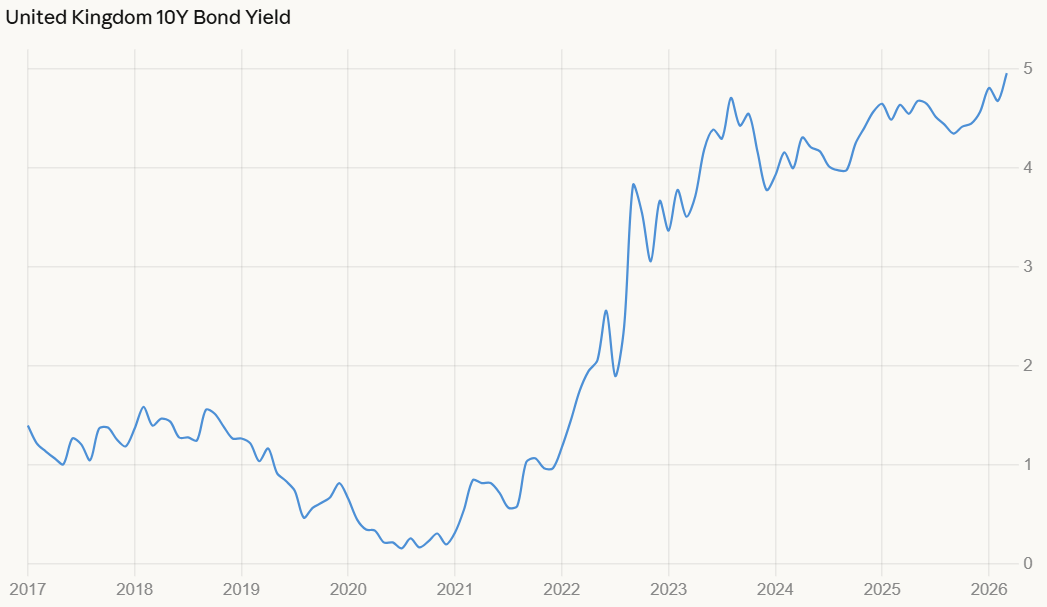

Figure 1 shows that 10-year gilt yields have risen sharply from near 0% in 2020 to around 4.5-5% in 2025-2026. This increase in yields allows pension funds to generate higher returns with less funds locked into these bonds. As a result, demand for long-term gilts has weakened, helping explain the improved funding positions seen in recent years.

This era of higher interest rates means that these pension funds are going through a period that analysts call a ‘funding revolution’. The PPF 7800 Index indicated that UK Pension schemes in 2025 and early 2026 hit record highs, with the funding ratio being above 140%. The funding ratio is just a simple way of measuring a pension scheme’s financial position, by comparing the value of its assets, what they own and have invested in, compared to its liabilities, which is what it expects to pay out in future pensions. Therefore, if a scheme has £140 in assets for every £100 of liabilities, that’s a funding ratio of 140%.

Back to the main idea, when interest rates were near zero, pension funds were structurally underfunded, not due to low capital, but rather burdened by the high present value of future liabilities. In such a low-interest environment, these pension funds need to hold a large amount of capital to meet their fixed payments (pension obligation to retirees) in decades to come, which presents itself as a major financial burden.

Now that interest rates have increased, and remained at a stable level, these funds are successfully reaching their investment goals and are able to generate strong-yield returns with less capital.

But why is this?

Now that pension funds no longer solely rely on long-term gilts, they’re able to diversify their portfolio and shift their funds into different investment types. When interest rates rise, newly issued bonds offer higher interest payments than older ones. So as older, low-yield bonds mature, these pension funds can reinvest that money into newer bonds that pay more. This means they can hit their investment return targets more easily, without locking money away for decades. This is a new strategy adopted by funds, to diversify their portfolio. It provides different sources of income, and the offset of risk that comes with tying money away for years.

This is why demand for these long-term gilts is now waning, given pension funds simply don’t need to allocate their funds into these products anymore, when they can generate higher income from higher-yielding, short-term bonds. Consequently, the DMO’s decision to slash long-dated gilt issuance reflects the new reality of the gilt market, where demand has structurally shifted, permanently. Ultimately, this is driven by pension funds no longer relying on these gilts to hit their investment targets, as high interest rates have significantly improved their funding positions.

Due to pension funds demanding less of these long-term gilts, the DMO needs to lean towards short-term bonds, which mature between 2-5 years. This benefits taxpayers, since short-term borrowing typically carries lower interest costs than long-term borrowing, and bond yield rates are used to set mortgage rates/interest rates for example.

This is due to investors demanding higher returns for lending over longer periods, as there is greater uncertainty around inflation and future interest rates. As a result, issuing shorter-term debt reduces the government’s immediate debt servicing costs. This frees up billions in the UK’s national budget, which could go towards the NHS, infrastructure or lowering tax rates. The exact figure the UK spent last year on overall debt servicing was £106 billion, so by saving a portion of this figure, it’s a large sum that could go towards the aforementioned causes.

However, there’s a catch to this strategy, because the government rarely ever pays off their debt with cash. Instead, they rely on a process called ‘rolling over’. For example, when the 2-year bond matures, and the principal amount is due, the government auctions new bonds to pay back the old lender.

A brief introduction to the government auctioning process: the UK government sells their gilts through the DMO’s auctions. Large investors like banks, pension funds and insurance companies submit bids showing how much they want to buy and the yield they are willing to accept. The government then accepts the lowest yields, meaning it borrows at the cheapest cost. Additionally, there are certain entities that are contractually obliged to participate in auctions. They’re known as primary dealers, or GEMMs in the UK, who ensure that the government can sell its debt, acting as market makers and stabilising the bond market.

However, what happens to sovereign debt refinancing when the monetary policy climate changes? If interest rates drop when the government ‘rolls over’ its debt, the government saves billions, as they can repay their outstanding debt at a lower rate (from the current 3.75%), and they have more funds to invest elsewhere into the UK, thereby allowing for some degree of fiscal room. However, due to supply-side shocks arising from geopolitical conflict, such as from the US-Israeli strikes on Iran, leading to the effective closure of the Strait of Hormuz, inflation is expected to rise from 3%, resulting in a hawkish stance from central banks around the world, including the Bank of England. With this, it is expected that the UK will be forced to renew its debt at an even higher, more expensive interest rate.

The bottom line here is that the DMO is betting that the future bond yields will be lower; however, if they’re wrong, this is a burden that taxpayers and businesses may have to accept, in the form of higher taxes in the future for later generations.

The DMO needs to deal with the memory of the 2022 gilt market crisis. The UK government had announced large unfunded tax cuts in the September 2022 Mini Budget announced by Liz Truss and Kwasi Kwarteng but had no explanation of where they’d get the funds for this. This resulted in both pension funds and international investors panicking, leading to sharp gilt sell-offs to reduce exposure. If it wasn’t for the BoE’s intervention, the entire pension market would’ve crashed.

Figure 2 shows the spread between UK and German 30 year bond yields, with Germany being used as a low-risk base due to its stable economy, strong public finances, and reputation for fiscal discipline, meaning its bond yields are lower and more stable. It’s a relatively safe place for investors to tie their money into.

The sharp spike following the mini-budget shows UK borrowing costs rising much more than Germany’s, highlighting a huge loss of confidence in UK fiscal policy, as investors demanded a higher yield to compensate for increased risk.

This event shattered trust between international investors and the government, with investor confidence in the British government’s fiscal prudence and ability severely damaged. As a result, the message the DMO is sending, by this issuance change from long-term to short-term gilts, is that the government wants market stability, over long-term uncertainty, having learned its harsh lesson from 2022. Foreign investors in UK debt are important, as without them, the UK would face significantly higher borrowing costs and financial pressures; hence, improving investor confidence is the main emphasis of the DMO. According to the OBR (Office for Budget Responsibility), foreign held UK debt has nearly doubled to around 25% of total debt since 2004, above the advanced economy average of 18%. This means the UK is more reliant on overseas investors to finance its borrowing, making it more vulnerable to sudden changes in confidence. If foreign investors lose trust, they may demand higher yields or reduce demand for gilts altogether, increasing borrowing costs. It’s imperative that the UK maintains good ties with foreign investors to ensure less volatility to the bond market.

Italy provides a useful comparison, as it has increasingly relied on shorter-term government bonds in recent years, partly because high debt levels and rising interest rates make long-term borrowing more expensive and difficult, so issuing short-term bonds helps reduce immediate costs. However, this strategy increases refinancing risk, as the government must roll over its debt more.

All in all, the DMO’s decision to slash long-dated gilt issuance marks the end of an era. For decades, the government and pension funds had a steady partnership where billions were locked away for 3-5 decades at a time. High interest rates have essentially ‘fixed’ the pension funding crisis, leaving these investors with a surplus and limited reason to keep purchasing long-term debt.

If the BoE can tame inflation and interest rates are relatively low, the UK government will benefit from low debt repayment costs and consumers will be an indirect winner. However, if interest rates rise, the UK will be trapped in a cycle of expensive roll-overs, with high repayment costs that will burden the treasury further.

Ultimately, the UK is moving from a long-term fixed debt model to a more reactive, short-term strategy. While this aligns with the current lack of demand from pension funds and helps maintain market stability following the volatility of 2022, it also means the government has less control over its future, long-term borrowing costs, due to shorter maturity durations. The success of this fiscal gamble now depends on the long-term course of inflation and the UK’s ability to remain an attractive destination for global investors.