European governments have shifted gear on defence spending with remarkable speed. The European Defence Agency reports that member-state investment and procurement reached record levels in 2024, with EU defence expenditure reaching €343bn, up 19% on 2023.

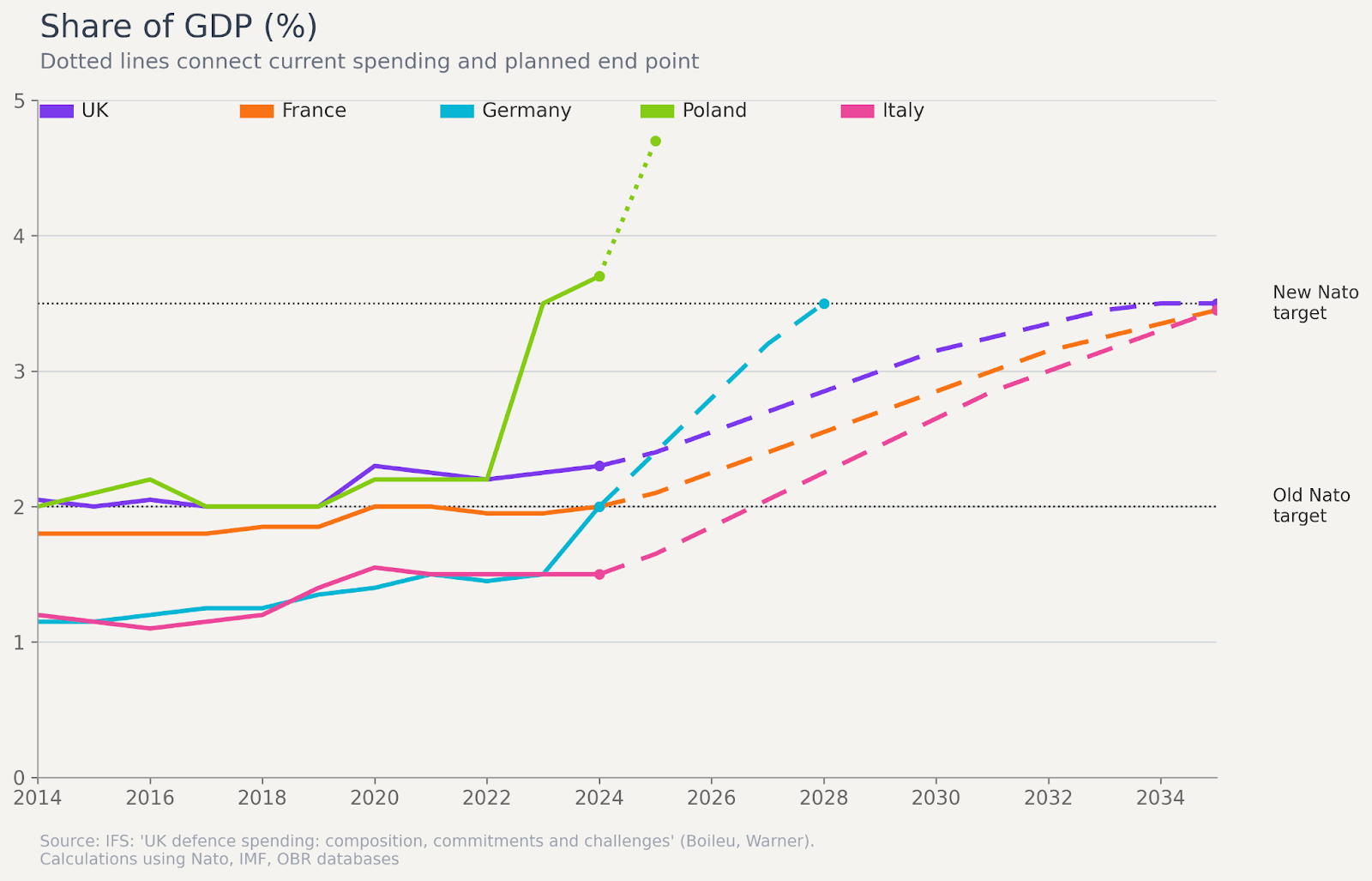

What began as reactive measures to the war in Ukraine has matured into long-term industrial commitments. Germany exemplifies this shift. After years of tight fiscal rules, it approved a “special fund” which lifted defence expenditure above 2% of GDP. In March 2025, lawmakers went further by approving an exemption of security spending beyond 1% of GDP from debt limits, enabling a €500bn fund for defence and infrastructure over 12 years.

Meanwhile, Poland, along with several Baltic states, has driven up spending even more aggressively. This is important for the industry. Predictable demand and multi-year procurement plans give prime contractors the confidence to scale. For instance, Rheinmetall secured a major deal worth $271mn with the German Bundeswehr to support logistics for NATO forces, indicating firm demand for long-term support and deployment readiness. Moreover, the recently adopted Security Action for Europe (SAFE) initiative offers up to €150bn in long-term, low-cost financing for heavy equipment and technology projects. With nineteen member states already requesting SAFE loans, Europe appears to be systematically rebuilding its industrial base.

Yet, turning public funds into functional capacity is harder than budgets might suggest. The post Cold War “peace dividend” left factories idle and eroded expertise across the continent. After over twenty years of downsizing, Europe is now trying to quickly rebuild, but in doing so is revealing bottlenecks in ammunition and skilled labour. Job postings, especially in engineering and materials within the sector, have grown faster than the wider labour market. In Eastern Europe, smaller component suppliers face a different challenge. Many are being pushed to full capacity and are struggling to meet surging demand.

Meanwhile, major firms have expanded order books and announced capacity increases, with Rheinmetall reporting a backlog that has risen markedly through 2025. This has prompted the firm to accelerate facility upgrades across multiple European sites. BAE Systems, SAAB, and Leonardo report similar gains in orders and production plans. The larger firms aim to onshore critical production and lock suppliers into longer agreements, to shorten fragile cross-border supply chains. Recognising the bottleneck risk, the EU already launched an ammunition-production programme under which ammunition is targeted to rise to 2 million units per year by the end of 2025. Past decades mean that the region doesn’t have the industrial depth to meet surge requirements without further investment.

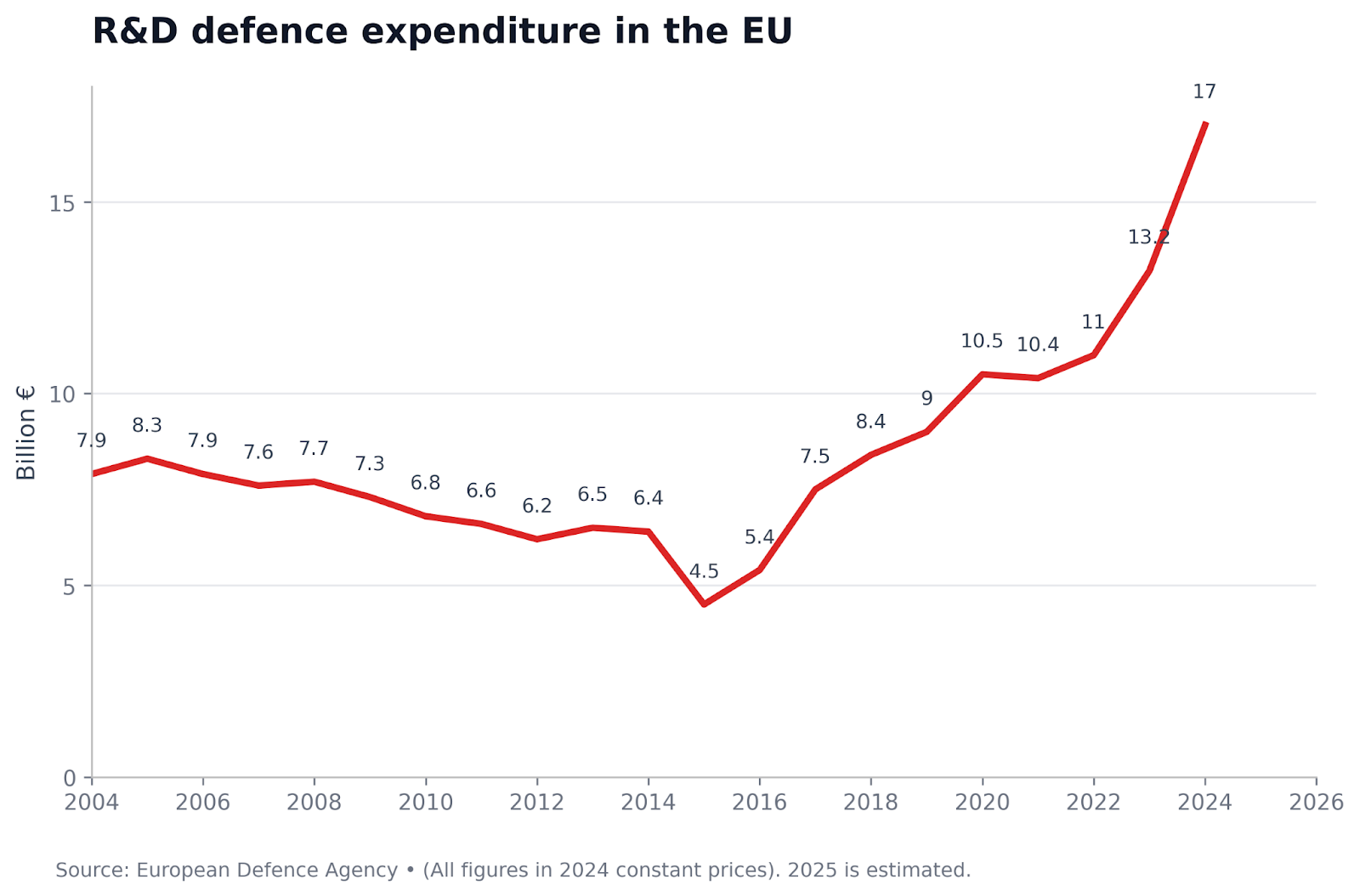

The strategic focus of defence is also shifting fundamentally. The twentieth-century model of defence dominated by tanks and fighter jets is now complemented and in some cases, overshadowed by data-centric capabilities. Governments are placing growing emphasis on cyber resilience, AI-assisted command, counter-drone systems, and modern sensor networks. As a result, defence-tech firms and start-ups are increasingly pivotal to national security. Early estimates for 2025 suggest R&D outlays have doubled relative to just 5 years ago.

Moreover, according to recent data for H1 2025, European venture capital investment into defence-tech startups reached €946.3mn, a 26% increase from the same period in 2024. The European Commission further highlighted the trend that emerging technologies are seeing faster rises in investment than legacy platforms. An interesting example is Germany's Helsing, which raised €600mn in June 2025 at a €12 bn valuation, positioning it as Europe’s defence-tech champion. The company develops AI software that analyses real-time battlefield sensor and weapons data. Vertically integrating, it has expanded into manufacturing its own drones and submarines.

Traditional defence firms are adapting to this, with BAE Systems increasing investment in electronic warfare systems, Leonardo partnered with Turkey’s Baykar to produce unmanned aerial vehicles (UAVs) as they estimate the European UAV market will reach $100bn over the next decade. However, Europe still trails the United States considerably in innovation within the industry. American companies benefit from the Defense Innovation Unit’s decade-long track record of awarding substantial contracts, while Europeans rely heavily on foreign investors to provide late-stage funding while facing greater regulatory hurdles.

After years of underperforming, European defence stocks have rallied since 2022. As governments reaffirmed commitments, early 2025 saw one of the strongest sector-wide surges in defence. Firms including SAAB and Thales climbed to all time highs on renewed investor optimism. But the rally has proven volatile, with November seeing sharp pulling back as diplomatic developments temporarily reduced threat perceptions. This pattern highlights the central tension investors face, i.e., distinguishing a structural shift and cyclical geopolitical sentiment.

Over time, the trend appears more structural, with Goldman Sachs predicting European defence spending could rise to 2.7% of GDP across the eurozone and UK by 2027. However, there is a risk of over-interpretation as spending in Europe depends on the political cycle, not just military needs. A change in public opinion or an increase in budget pressures are factors that make defence expansion unpredictable. Spain's rejection of the 5% NATO target and instead sticking with 2.1% illustrates divergent national priorities. The spread of valuations in the sector reflects these uncertainties. Companies that have strong tech leverage and exposure to high-growth segments or vertically integrated supply chains have seen significant multiple expansions.

Looking forward, the factors that determine which businesses will outperform are how effectively orders are converted to deliveries and agility in the adoption of new technologies. For investors, the most attractive bets for the long term will likely be hybrid firms combining manufacturing scale with tech-driven capabilities.