By exchanging something valuable (for example, a government bond), you are able to get cash for the night. The next morning, you buy the bond back, plus a small fee for the overnight loan. The fee acts as an interest rate. This happens millions of times a day, across the world, and keeps the financial markets moving.

For decades, this system was controlled and run by Wall Street. If a bank in London, Tokyo, or Singapore needed to borrow dollars overnight, the first instance would be New York. American banks were favoured because they had the biggest balance sheet, the most liquidity, and trusted relationships. This is no longer guaranteed.

In July 2023, a new banking rule called Basel III Endgame came into action for American banks. The aim was to make banks safer by keeping more capital reserved, approximately 30%-35% more than previously.

This might sound sensible. But it had unintended side effects. Keeping more cash in reserve means banks have less room to lend it out. This, therefore, meant that lending dollars through the repo market became way more expensive.

American banks like JPMorgan and Citigroup responded by pulling back. They only lent to their oldest and most important clients, but the rest were not as fortunate.

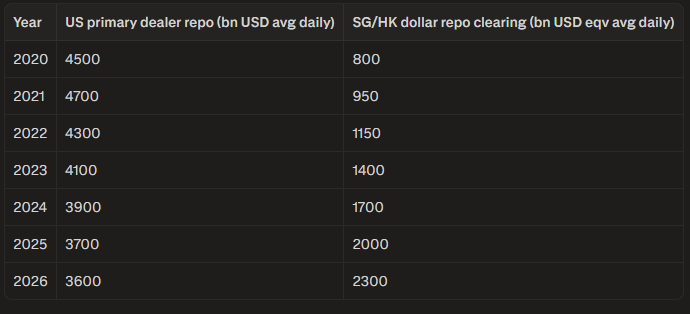

Simultaneously, around the same time, the US government was issuing a record breaking $2.6 trillion worth of new bonds, while the market needed dollars to buy and finance them. This meant the demand for dollar lending went up just as the supply went down.

It went to Singapore, Hong Kong, and the Cayman Islands. Not because those places are cheap or suspicious, but because they have fewer restrictions and rules regarding the amount of cash banks can reserve and store. The same dollar that became expensive in New York is still perfectly affordable in Singapore.

The monetary authorities of Singapore reported a 67% increase in lending in 2025 alone. That alone is extraordinary growth for a single year, and is almost driven by institutions like the ones that run businesses on Wall Street.

In the Cayman Islands, where most of the world’s largest hedge funds reside, 43% of their dollar funding now comes from outside of the US, up from 18% in 2022. This means that over those three years, their monetary sources had undergone significant changes.

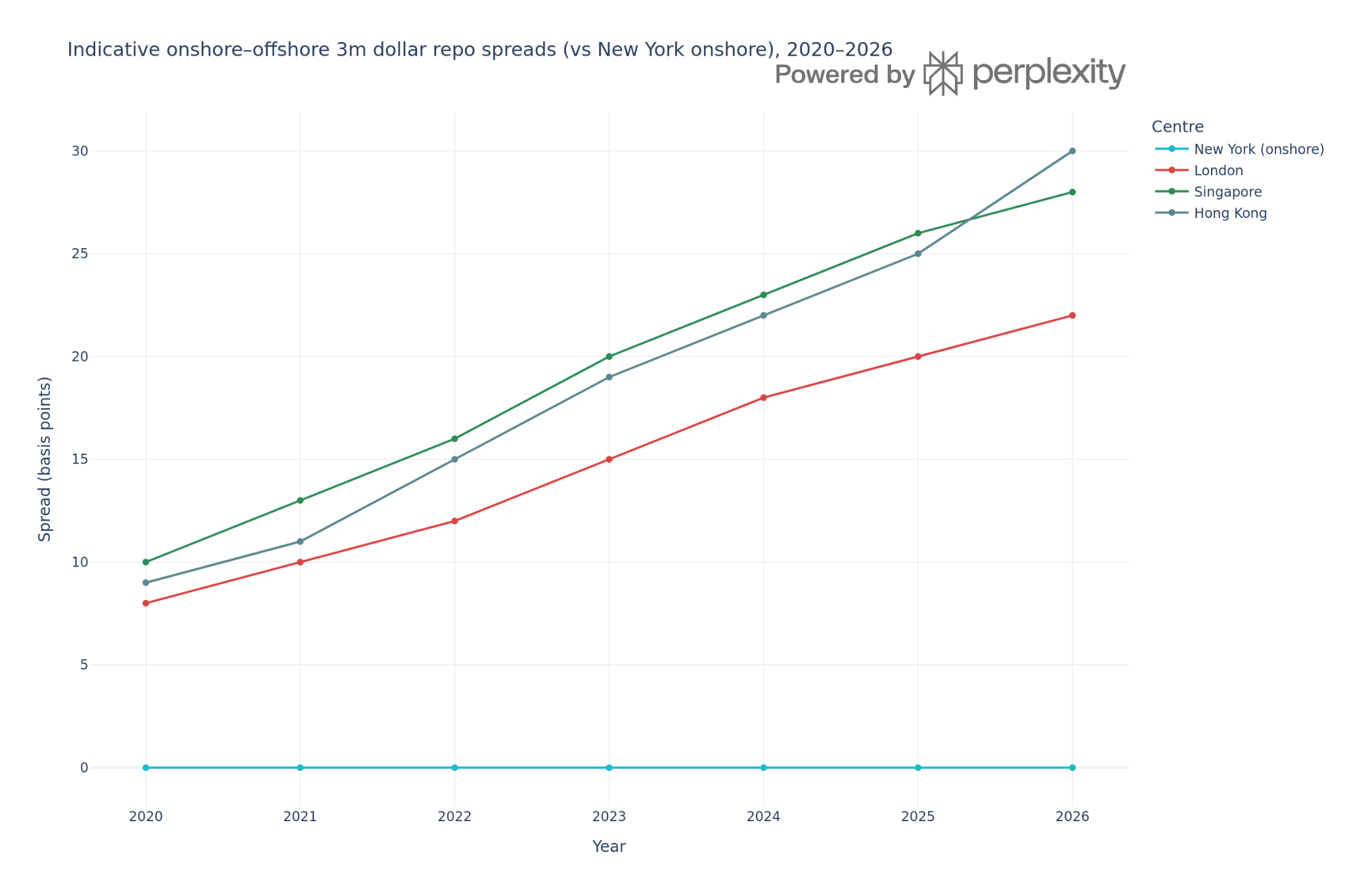

If the cost of borrowing dollars is different depending on where it is borrowed, then this can create a problem for investors. For instance, owning US government bonds, whilst also obtaining funding through a bank in Singapore. The interest rate paid there may be higher or lower than the rate in New York, with the gap possibly moving without warning.

This is where basis risk could arise. Basis risk can be defined as the gap between two prices that you assumed would move together.In this context, it refers specifically to the gap between USD repo rates priced in Singapore and USD repo rates onshore in the US.

As above, if you are funding a US bond through a Singapore bank, you will be exposed to the differences between these two USD repo rates rather than a simple USD-SGD interest rate differential.This gap could potentially widen suddenly, meaning the investment becomes more expensive to hold, despite the bond itself not changing.

Basis risk used to be negligible and often small enough to ignore.However, it was a key factor in earlier episodes such as the LIBOR dislocations during the financial crisis, where different tenors and currencies behaved in unexpected ways. It also played a central role in the September 2019 US repo spike, when secured funding rates briefly surged despite no comparable move in policy rates or broader credit spreads. However, it can no longer be overlooked, particularly as the pricing gap between US and offshore dollar lending is growing. As such, managers who protected their portfolios using older strategies may find that they are no longer as effective.

More broadly, the US Federal Reserve, America’s central bank, sets interest rates in a manner to manage the economy. When rates are raised, the goal is to make borrowing more expensive to slow down the economy, for instance.

However, this tool can only be effective where the Federal Reserve can see, and thus influence, where dollars are actively being lent. If a share of dollar lending grows overnight in regions such as Singapore or Hong Kong, this is outside of the US’s direct reach. In turn, the Federal Reserve's decisions can take longer to have an effect, and could potentially not even reach those markets.That said, US policy can still be transmitted indirectly via the standing FX swap lines with foreign central banks, which allow the Fed to supply dollars to offshore systems in times of stress, and via the central role of SOFR in pricing global dollar funding.

The dollar is not being replaced, especially as all the loans that have been described throughout this article have been made in dollars. Rather, it is the system that the dollar flows through, and those who have a level of control over it.

Initially, American banks used to be guardians of dollar lending globally, but the introduction of new regulations has altered this. In turn, borrowers retreated to other locations, but to overcome this, the market has developed new routes through the Cayman Islands, Hong Kong, and Singapore.

The assumption that the cost of borrowing dollars will be the same everywhere has clearly been challenged in recent times, and this is a key takeaway for investors. The gaps in costing have only gotten wider.This poses further challenges for policymakers: while the dollar system spans vast networks through foreign financial hubs, it complicates monitoring, measuring, and ensuring stability during volatile periods.