A key reason this dynamic receives less attention is its delayed transmission into consumer prices. Oil price movements are immediate, whereas fertiliser operates through the agricultural production cycle.

Farmers are effectively paying higher prices now for inputs that will be used in future planting periods. Depending on when fertiliser is purchased, it can take an entire growing cycle for these costs to fully filter through into food prices.

In practice, this means the impact is typically seen with a lag of around three to six months. Fertiliser purchased today will be used in planting later in the year, with the resulting price pressures appearing further down the line at the retail level.

At the same time, farmers are facing a double squeeze from both fertiliser and fuel costs rising, which is placing pressure on margins and forcing decisions from farmers such as reducing planting below capacity in order to remain viable in the long term rather than producing at a loss.

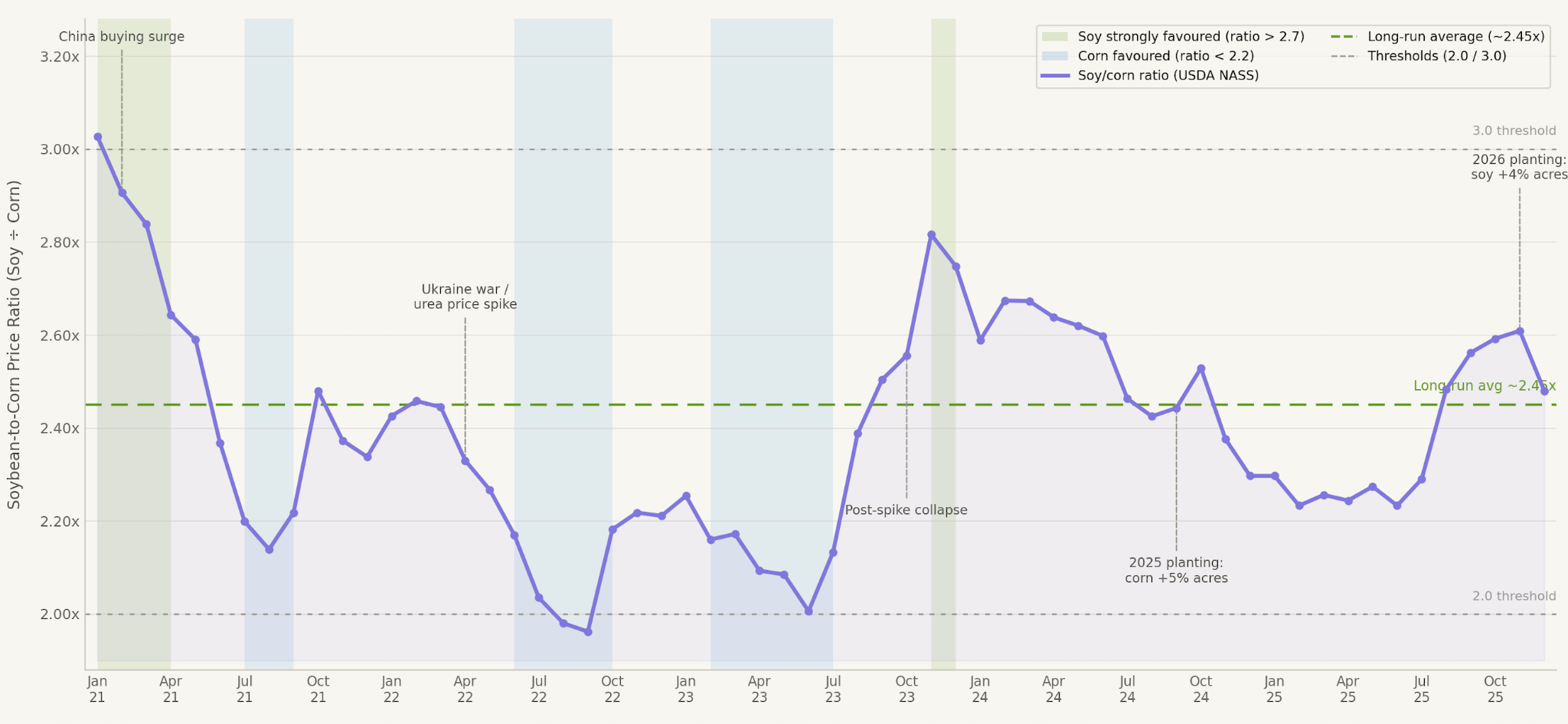

One way of understanding how farmers respond to these shifts is through the soybean-to-corn ratio. The soybean-to-corn ratio is simply the price of soybeans divided by the price of corn and captures the relative profitability of planting corn versus soybeans by comparing their respective futures prices.

As a general rule of thumb, a ratio higher than ~2.7 is where corn is becoming less profitable relative to soybeans. A lower ratio of below ~2.2 suggests the opposite, where corn is relatively more attractive to produce.

In this case, the ratio has actually fallen since late last year and early 2026, moving closer to its long-run average. A key driver has been rising fertiliser costs, which have increased the cost of producing corn relative to soybeans, signalling that corn has become less profitable. This is encouraging farmers to allocate more acreage towards soybeans, which are less fertiliser-intensive, even though corn prices may still appear supportive. Rising input costs are therefore eroding margins and reshaping planting decisions.

What should be emphasised, however, is that farmer decision-making is more nuanced than relying on these graphs alone. Even though the ratio sits close to its long-run average, showing a neutral signal between corn and soybeans, farmers still have to consider other factors, such as production costs, which are not fully captured by this measure. This highlights the multi-faceted approach that is often needed in finance and trading.

This matters because corn is not only a major food crop but also a key input in animal feed. As corn supply tightens or becomes more expensive, feed costs rise, feeding through into higher prices for chicken, pork, and beef.

Farmers typically use forward contracts to lock in prices, which smooths short-term volatility but also delays the adjustment to higher input costs. As a result, current fertiliser price increases are unlikely to be immediately visible in food prices.

However, as new planting cycles begin and higher-cost inputs are fully embedded, the effects are likely to become more apparent towards the backend of the year. The combination of elevated fertiliser prices, higher fuel costs, and shifting crop allocation points towards upward pressure on food inflation.

Ultimately, while oil dominates attention due to its immediacy, fertiliser represents a slower-moving but imminent impact of the Strait of Hormuz disruption and is likely to feed into the broader cost of living.