Special purpose acquisition companies, put simply, are companies set up to acquire private companies. First, a SPAC has a ‘sponsor’ who raises money through an IPO on the stock market from public investors. Next, they go looking for a target private company to acquire and finally, merge with that company, which turns the private company public.

The SPAC sponsor is hunting based on an investment thesis, focusing on a particular sector or geography, with a deadline of typically 18-24 months. In the meantime, SPAC shares trade on an exchange like any other stock, during which they tend to drift down.

If the manager succeeds, the SPAC merges with the target company in a ‘de-SPAC’. If it fails to find a company it’s willing to buy, the SPAC closes, with the money returned to the investors.

It’s worth considering this for each of the players: the investors, the target companies, the banks underwriting the deal (I’ll explain this) and the sponsors.

Investors

Private firms

Banks earn large underwriting fees (underwriting is ‘taking on risk’; here, it refers to not all of the 80% of shares being bought up by investors).

Sponsors can profit enormously by owning “founder shares”. Sponsors start the SPAC process with a “promote” share of typically 20%, at a heavily discounted price. This has the potential upside of becoming hugely valuable when paid when a de-SPAC is completed.

There are rewards to be had for all - here’s how it’s panned out.

SPACs were born in the early 2000s, mainly as an equity capital markets product that niche players worked with. The market matured over the next 20 years, enticing bigger players like Citigroup, Goldman Sachs and JP Morgan.

The pandemic saw a spike in not only cases but also SPACs. Interest rates near the floor meant cheap money, looking for optionality and high-growth opportunities - a SPAC represented both of these. Greater risk appetite, big name and celebrity endorsements (think Bill Ackman, Jay-Z and Serena Williams), and large SPAC mergers seeing big success all combined into a surge of SPAC IPOs, with 300+ in Q1 2021 (White & Case, 2022).

One prominent character in the story is Chamath Palihapitiya. Proclaimed the “SPAC king” on Wall St, he’s an ex-Facebook executive and now VC who championed SPACs from the beginning - as The New Yorker puts it, he "gained notoriety by telling seductive stories of quick riches". He put through one of the most high-profile SPAC deals, taking Richard Branson’s spaceflight business Virgin Galactic public in 2019, along with completing over 10 other deals, in fascinating spaces such as robo-taxis, healthcare and fintech (FT, 2021).

As always, a boom is followed by a bust, and the SPAC bust was faster than a balloon, collapsing for a variety of factors.

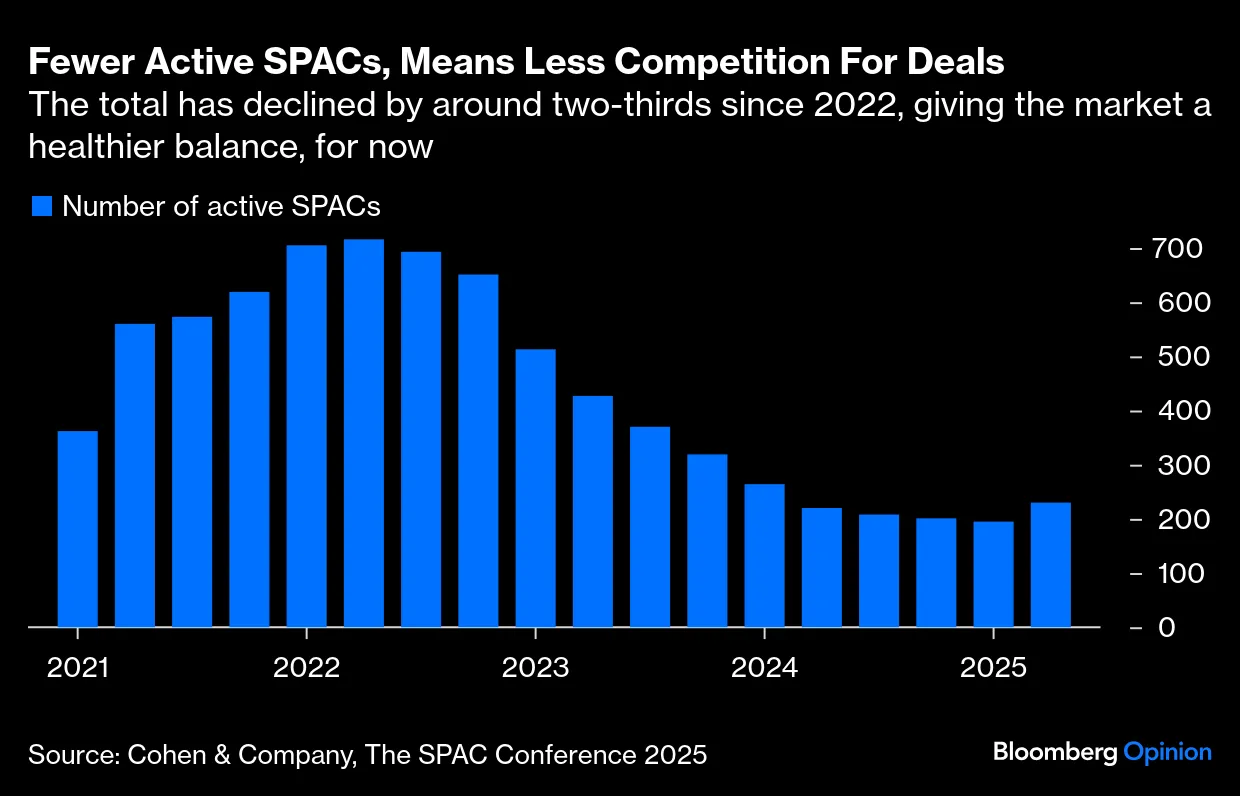

The result was that over 350 SPACs have been liquidated since the start of 2022, a crashing fall from the heights of 2021. Furthermore, the majority of the 2021 SPACs are now trading at well below $10 a share (SPACInsider, 2024).

2025 has seen encouraging signs of the market recovering, with H1 seeing over $11bn in deals, a big shift from the $2bn of 2024 (FT, 2025). We’re even seeing the first crypto-focused SPACs. Initially, this feels counterintuitive in market conditions with rising inflation, lagging growth and perennial uncertainty. The explanation for this resurgence? Multi-faceted as you’d expect.

It’s another Trump trade. Trump Media and Technology Group, who own Truth Social, used a SPAC to go public last year (MarketWatch, 2022), signalling that the new administration backs this market vehicle. Even more concretely, their Secretary of Commerce, Howard Lutnick, was previously Cantor Fitzgerald’s CEO, a leader in SPAC underwriting. With tariffs damaging confidence and so the prospects for traditional IPOs, SPACs are seen as a sensible alternative - an unanticipated consequence of ‘Liberation Day’!

Other factors influencing the SPAC trend are adapted rules on disclosure standards, which imbue trust and certainty, as well as greater reception from hedge funds. High interest rates make Treasury bills an attractive place for hedge funds to park cash while hunting for opportunities. SPACs offer an appealing wrapper for this strategy - the downside protection of returns during the search period, combined with potential upside exposure to high-growth private companies that these funds can’t access easily.

One noteworthy deal features the SPAC king Palihapitiya himself. Launching “American Exceptionalism Acquisition Corp”, he plans to raise $250mn to buy companies that - you guessed it - back US exceptionalism, addressing “the fundamental risks that come from our interconnected global order”. The deal is made unique by an absence of warrants and a bold risk foreclosure from Palihapitiya - “[if retail investors] do lose their entire capital, they will embody the adage from President Trump that there can be ‘no crying in the casino".

The deal will be underwritten by Santander, which is looking to make a move in the SPAC space, having hired several SPAC bankers from Credit Suisse, who financed the Virgin Galactic deal mentioned earlier. Their commission is set at 6%, a handy $15mn on the expected IPO value. However, the deal cleverly pays only a small upfront fee of $250k, unless the de-SPAC is completed.

The uncertainty ailing the global economy makes accurate predictions foolish, but we can expect a steady rise in SPACs as confidence slowly regrows in their validity.

On the back of my summer reading of Howard Marks’ book, “Mastering the Market Cycle”, it is fascinating to observe the cyclicality of the SPAC market. As noted on the FT’s Due Diligence, “it’s starting to feel a lot like 2021 - cryptocurrencies are surging and dozens of SPACs have gone public over the past year, led by many of the promoters behind the last bubble.”

One cycle he discusses is the credit cycle, which plays a role here too - the luring of hedge fund money as investments might cease, with a dovish tone about interest rates recently. Despite this, rates are relatively high for the moment, and hence, in the short term, we shouldn’t see investors running away.

The recent boom is again created by an inability to push traditional IPOs, and a new wave of optimism, taking reduced scrutiny as a sign to increase their risk threshold. It’s the classic market forces of herd mentality, FOMO and safety in numbers at work again - Goldman Sachs has u-turned on their dismay of SPACs, for example. The pragmatism of these large financial institutions is fascinating, utilising rational calculus to optimise for reputational risk and reward.

Speaking of incentives, a criticism of SPACs is that sponsors prioritise pushing a bad deal through instead of liquidating, since they earn the large “promote” only on completing a deal. Furthermore, there is an inherent black box in the target acquisition, with valuations being set with backroom negotiations, not the elaborate sounding out of investors through roadshows and bookbuilding. In the end, the sponsors and banks have the last laugh and, studying deals so far, the investors are left reeling.

SPACs are an exciting new route to the public market, providing investors with early access and targeted products. They have built-in risks and, from the picture so far, are very cyclical. I believe the boom is not curbing back down anytime soon - prepare for a pack of SPACs.