.png)

This meant countries with a trade surplus would accumulate gold as a payment for their exports, whilst nations with a trade deficit would see their reserves fall, since these were used to pay for imports. The advantage of using gold was that countries would be able to do business with each other with far more consistent exchange rates, thus spurring globalisation and greater cooperation. Eventually, the world economy transitioned to a fiat currency, leading to a system backed by government trust rather than physical commodities.

This article aims to explore the key reasons behind the monetary system decoupling from gold’s stability, and yet despite this, why gold remains an important hedge against macro headwinds in today’s global markets.

In 1944, despite World War 2 continuing, delegates from 44 countries met to discuss the future financial world order following the conflict. In particular, the conference’s primary significance regarding gold was the creation of the Gold Exchange Standard. This functioned as a hybrid between the old physical Gold Standard and the modern Fiat system, where the US government guaranteed that it would exchange $35 for an ounce of gold upon request from other central banks. In return, every other participating nation “pegged” their currency to the USD at a fixed exchange rate, meaning these countries were indirectly backed by gold from their respective dollar holdings.

This hybrid system was revolutionary, as it attempted to give countries the autonomy to balance stability and flexibility over their money supply. Now, these nations could adjust their exchange rates (devalue or revalue) to help their economy when needed, provided they had approval from the newly formed International Monetary Fund (IMF). The IMF’s main task was with managing the exchange rate system and providing short-term loans. In contrast, the other main organisation formed at the conference, the World Bank, was focused on the long-term reconstruction of war-torn nations.

As the USD was the only currency backed by gold, resulting in global trust and confidence in the currency, the States were able to enjoy ‘exorbitant privilege’. This was because the US could run trade deficits by simply printing more dollars, which other countries were happy to hold as reserves. However, this eventually led to the Triffin Dilemma. To provide the world with enough liquidity (USD) for global trade, the United States had to keep running trade deficits, which resulted in many people questioning whether the US had enough gold to back all those dollars.

To compound these doubts further, by the late 1960s, the country was spending heavily on the Vietnam War and domestic programs through printing money, Consequently, more dollars entered the global market than the US had gold to back, resulting in France demanding the States to exchange French dollar reserves for physical gold. This move threatened the financial authority of the USA, as it showed countries were lacking trust in the dollar as a store of value, with Charles de Gaulle’s France famously sending ships loaded with dollars to bring back gold bullion. Moreover, Britain, the USA’s longest-standing, closest ally requested to exchange $3bn for gold, fearing it was far overvalued than its intrinsic value.

Fearing a global bank run, President Nixon universally ended the direct convertibility of the dollar for gold, given the country simply did not have enough gold to fulfil its promise of exchanging $35 for every ounce of gold it held. Indeed, there were roughly $40bn in the hands of foreign central banks, whilst the US had only about $10bn worth of gold left in its reserves. As a result, the Bretton Woods system effectively ended and ushered in the era of pure fiat currency.

Economists regard inflation as one of the primary indicators of an economy's wellbeing. Whilst sustained, high levels of inflation can erode trust in the currency as a store of value and the fiscal prudence of political institutions, deflation can also harm the economy, just as worse, if not more. When the average price level of goods and services in an economy starts falling (deflation), consumers will delay purchases, particularly on big-ticket items, as they anticipate further price decreases. Such postponement of economic activity spreads throughout the economy, where prices fall, with businesses interpreting this signal to cut production, leading to unemployment, and governments faced with the prospect of financing projects through debt due to low tax revenue.

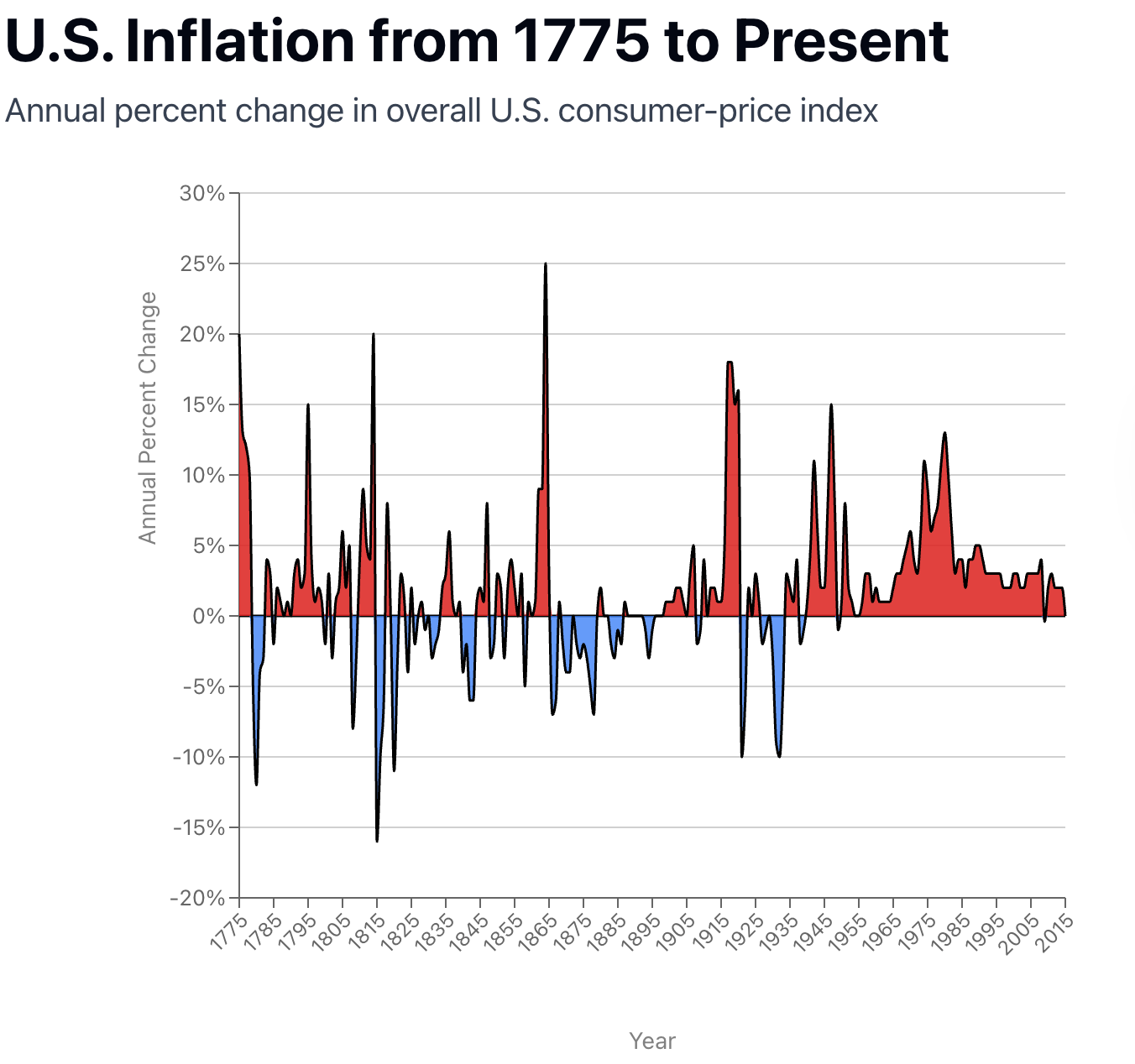

With this theory in mind, it is important to analyse historical trends in the changes in average price levels. Figure 1 (above) illustrates that before 1944, the US had significant points of deflation along with inflation. This is a direct result of economies having little control on monetary policy in their system. Following the Bretton Woods Agreement, there were some periods of high inflation (reaching as high as 14% in the late 1940s) but once the US came off the gold standard in 1971, we saw more sustained periods of inflation. The exception came throughout the 1970s due to the Oil Crisis, where OPEC members imposed an oil embargo on the States in retaliation for its support to the Israeli military. As oil prices increased, the cost of production for firms rose, from transporting goods and manufacturing goods in factories spiked, leading to sustained, high price levels. Aside from this, inflation stayed at or below 5% for the best part of three decades, highlighting that with responsible policymaking, it is possible to maintain price stability in an economy, without the gold standard.

Since the U.S dollar was no longer backed by the gold commodity, this gave countries the flexibility to control their money supply to tailor it to their economic environment. For example, during a recession, like in 2008 following the GFC, central banks were able to “create” new money to keep banks lending and firms operating through quantitative easing. Had this been under a gold standard system, nations would have been forced to let the system crash as they could not ‘make’ more gold. Furthermore, a key reason behind the US’ low levels of sustained inflation was because the Federal Reserve is able to adjust its monetary supply at around 2% inflation rate to encourage spending (consumers will prepone purchases knowing prices will rise in the future even more), without making prices increase rapidly and unsustainably.

By its very nature, a fiat system, where monetary flexibility was allowed led to excessive supply of USD (given USD did not need to be tied to gold), resulting in inflation. Consequently, deflation was never experienced by the USA, although disinflation (a fall in the rate of inflation) did happen to get inflation closer to the 2% mark that central banks universally target.

Although historically currencies were tied to gold, despite the Nixon Shock and the now prominent Fiat system, this rare commodity still plays a crucial role in modern investors’ portfolios.

This is for several reasons. Firstly, there is a supply constraint as new mining only adds about 1-2% of gold to the annual total supply. Secondly, gold is a chemical element, which cannot be manufactured in a laboratory or printed like money today, making it impossible to hyperinflate its value. Although it is a scarce resource, simultaneously it is chemically inert, meaning that it will not react with air or moisture and change through corrosion or rust. This gives it the fundamentals needed to preserve and increase its value since there will always be a low supply of it, for a given high demand due to its versatility in jewellery, technology, and healthcare.

To add to this, gold acts as a buffer against price volatility. Even if every gold mine on earth stopped working tomorrow, the total global supply of the commodity would only drop by an insignificant 1.5% as an optimistic estimate, making it resilient to supply shocks and geopolitical turmoil. Finally, there is no counterparty credit risk. To explain this, if you hold a fixed-income asset, like a sovereign bond, you depend on the state to pay you back. However, if you hold physical gold, its value only depends on the metal itself, making it a safe, reliable, long-term investment.

For investors, the main safe havens in times of macroeconomic uncertainty in the category of fixed-income, currency, and commodities are US treasury bills, US Dollar, and Gold. As the latter is priced in Dollars, when the currency weekends due to Federal Reserve reducing interest rates, or elevated levels of US inflation, gold typically appreciates in value. This is because investors reallocate capital towards safer assets to hedge against inflation, due to the belief it preserves your ability to purchase goods even when the paper currency loses value. Consequently, institutional investor’s portfolios will be more resilient, stable, and liquid due to the commodity's low beta of 0.06 (meaning its price movements show almost no correlation with the broader equity market) making it an ideal asset to diversify with.

Following the 1944 Bretton Woods Conference, when the world shifted its monetary order, issues such as the Triffin Dilemma and Nixon Shock led to the Fiat System being favoured over the gold standard. Whilst this has allowed for greater economic flexibility in managing financial crises individual to each country, political instability from conflict, market volatility and structural shifts has remained regardless.

Despite currencies no longer being pegged to gold, people's trust in the commodity has not changed as its enduring influence remains one of only few constants in today's world, making it such a crucial asset of any portfolio.