.png)

Stablecoins’ rapid growth has caught the attention of regulators. The EU’s MiCA framework, the US’ GENIUS Act signed into law in July 2025, and the UK’s upcoming “Systemic Stablecoin” regime led by the Bank of England all share the same concern: stablecoins are now large enough that, if something goes wrong, the impact could spill into the wider financial system.

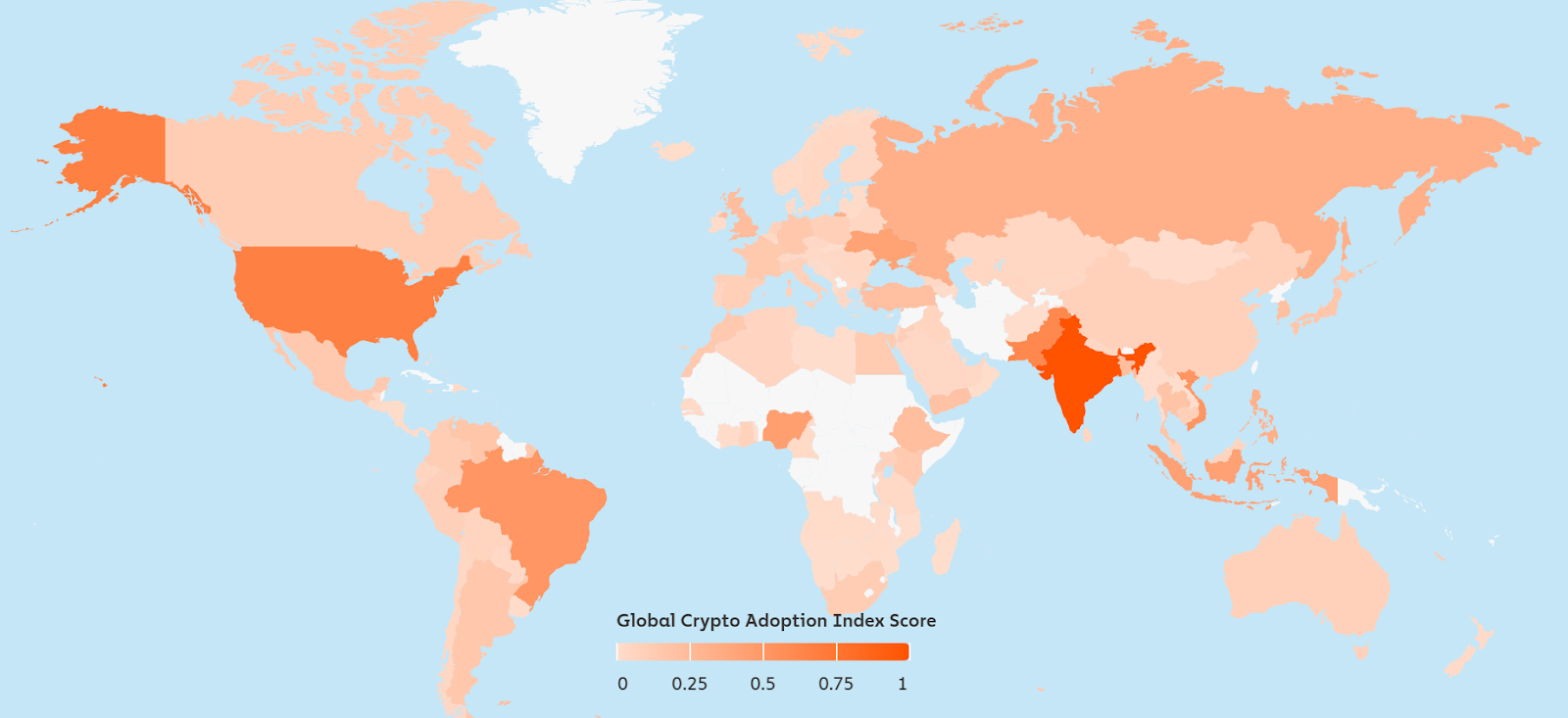

The rise in stablecoins’ popularity has mostly been driven by their speed and low cost. In countries facing high inflation or currency instability, people increasingly use stablecoins to protect their savings. Nigeria is a clear example of this.

The Chainalysis Geography of Crypto report ranks it among the top three stablecoin markets globally. With annual inflation reaching 34.2% in late 2024 (National Bureau of Statistics), many Nigerians now keep part of their savings in USDC or USDT to protect their purchasing power. Stablecoins are also becoming a practical tool for remittances and cross-border payments, where they tend to be faster and cheaper than using a bank.

As stablecoins grow in popularity, the risks around them are becoming harder to ignore, and many of those risks depend on how transparent the issuer is. Since the launch of USDT in 2014, it has been the most widely used stablecoin globally, but has faced criticism in recent years over the transparency of its reserves.

In 2021, Tether faced a $41 million fine from the CFTC after regulators found it wasn’t fully backed between June 2016 and February 2019. USDC is seen as the safer option, as Circle publishes monthly reports showing the exact value of its reserve assets, giving users confidence it maintains its 1:1 dollar peg.

Crypto-collateralised stablecoins such as DAI take a different approach. They use cryptocurrencies as collateral, which makes them decentralised but more sensitive to volatility in the crypto market. Despite stablecoins being steadier than most crypto assets, their safety still depends on regulation.

The collapse of Terra in 2022, an algorithmic stablecoin that wiped out approximately half a trillion dollars across the wider crypto market, remains a reminder that poorly designed stablecoins can result in catastrophic failures.

MiCA is the EU’s new rulebook to regulate crypto assets within the EU and EEA. Stablecoins are split into two groups by MiCA: EMTs, which are backed by a single currency and ARTs, which reference a broader mix of assets. EMTs (E-Money Tokens) are stablecoins that are pegged to a single currency to maintain a stable value. EMT issuers must hold their reserves in safe, liquid assets like cash or government bonds, and they must allow consumers to redeem at full value at any time to ensure consumer protection.

ARTs (Asset-Referenced Tokens) are stablecoins whose value is pegged to a basket of different assets. ARTs face even tighter supervision because their structure is much more complex, and regulators are cautious about how large they could become. According to Cyfrin, MiCA also places a €200 million daily trading cap on ARTs to ensure that an ART does not grow uncontrollably large and does not pose a threat to the financial system. MiCA is designed to make sure any stablecoin operating in the EU has sufficient liquidity and transparency to avoid a repeat of collapses like Terra.

The US GENIUS law, signed in July 2025, was the US’s first serious attempt at setting clear rules for stablecoin issuers. The law introduces a two-tier structure: smaller issuers can be licensed at the state level, while larger issuers fall under direct federal supervision. In both cases, issuers must be approved before launching a new stablecoin, something which wasn’t required previously under the old set of state rules.

The US framework is more flexible compared to MiCA and encourages private-sector innovation. The key motive behind the GENIUS act is strategic: regulators want dollar-backed stablecoins to scale in digital finance, strengthening the dollar’s position globally.

The UK’s “Systemic Stablecoin” regime, led jointly by the Bank of England and Financial Conduct Authority, is set to launch in 2026. The BoE policy focuses specifically on systemic stablecoins because of their potential to disrupt financial stability. Issuers are required to hold their reserves in high-quality, liquid assets such as short-term government bonds and cash deposits, while the FCA will oversee consumer protection and market integrity.

Despite the UK being open to digital-market innovation, it is taking a deliberately cautious approach, which prioritises financial stability. Policymakers remain concerned that if stablecoins reach large-scale adoption, heavy redemption flows could drain liquidity from commercial banks during a financial crisis.

The implementation of regulation on stablecoins is shifting them from a crypto product to a financial infrastructure. While the impact won’t be immediate, the direction stablecoins are heading in is clear: fully backed, transparent issuers will thrive, and weaker models will be wiped out.

As stablecoin adoption rises, institutions will play a bigger role in ensuring consumer protection and the wider financial system remains stable. Ultimately, despite the expected continued rise in popularity of stablecoins, the future will be shaped by transparency, trust, and regulation.