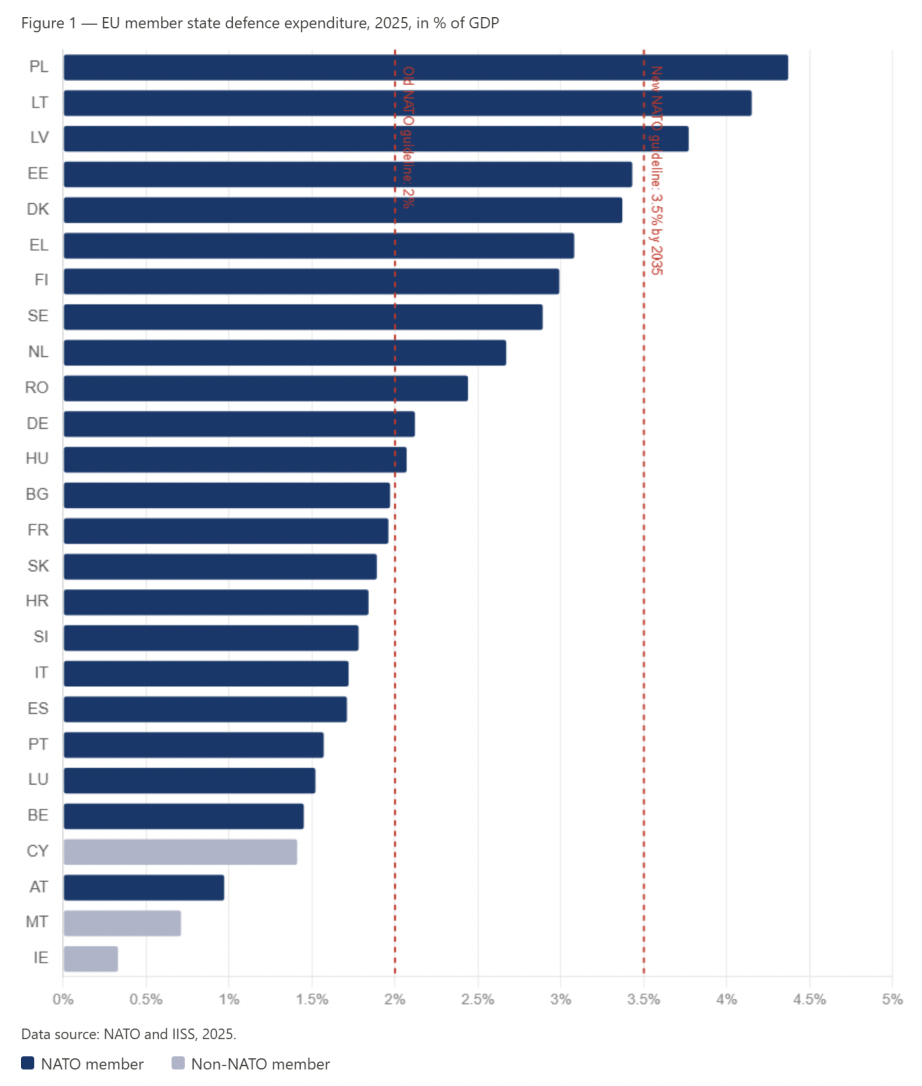

The numbers make the shift hard to argue with. According to the European Parliament, EU member states' combined defence budgets rose from €218 billion in 2021 to an estimated €381 billion in 2025, a jump of over 75% in four years. Germany, long constrained by its post-war consensus on military spending, first activated a €100 billion special defence fund in 2022, then followed it with a constitutional reform creating a further €500 billion in defence capacity through the mid-2030s. Poland has, per NATO figures, become the alliance's top spender by GDP share at over 4% and climbing. At the NATO Hague summit last June, allies went further still, committing to a 5% of GDP target for combined defence and security spending by 2035, a level that could, by some estimates, push European defence expenditure toward €800 billion annually by the end of the decade.

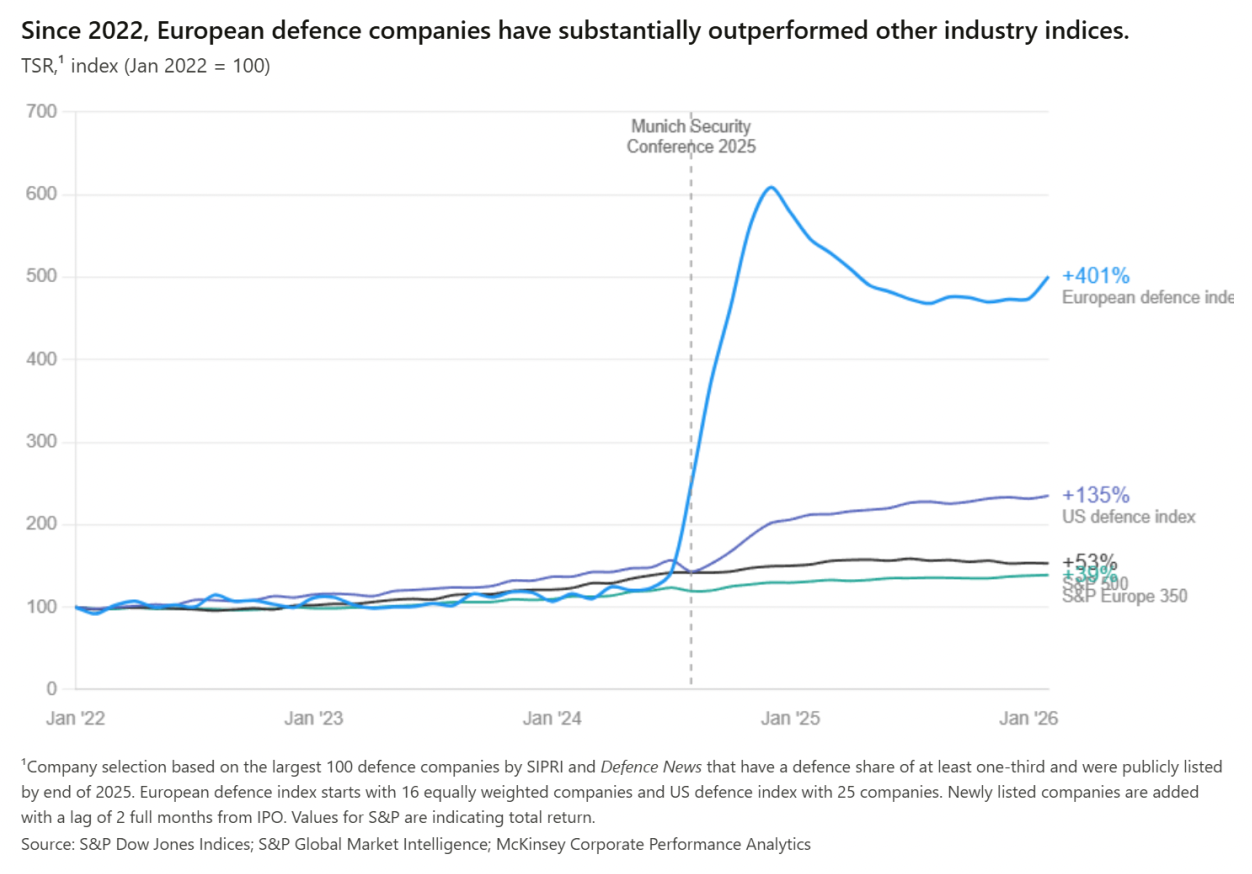

Equity markets have not been slow to respond. An equally-weighted index of large, publicly listed European defence companies has delivered a total shareholder return of over 400% since 2022. Rheinmetall, the German group that has become the bellwether of European land defence, posted 2025 revenues of €9.9 billion, up 29% year-on-year, with its operating margin expanding to 18.5% and its order backlog hitting a record €63.8 billion. That backlog, which includes framework agreements stretching years into the future, gives the company a level of revenue visibility that is genuinely unusual in any sector. The STOXX Europe Aerospace & Defence benchmark grew 53% in 2025 alone, against just 8.3% for the EUROSTOXX 50. Babcock International more than doubled over the period, Rheinmetall gained 158%, and even some of the more modestly positioned contractors saw re-ratings that would have looked implausible just a few years prior. The breadth of the move matters: this has not been a story of one or two stocks catching a theme, but of an entire sector being repriced.

One underappreciated driver of these moves has been an abrupt shift in how institutional money approaches the sector. For years, defence was effectively uninvestable for ESG-oriented funds, marked as high-risk by rating agencies, and excluded from Article 8 and 9 mandates under Europe's SFDR framework. Yet, the European Commission clarified in 2025 that SFDR does not prevent investment in defence companies, and a Defence Readiness Omnibus issued in June explicitly argued that the defence industry contributes to social sustainability under UN Sustainable Development Goal 16. Major asset managers including UBS, Allianz Global Investors and DWS Group have lifted longstanding bans on defence investing. The Morningstar Europe Index now has 4.7% exposure to aerospace and defence, up from just 1.5% at the start of 2022. That tripling of index weight has forced passive vehicles to buy in regardless of conviction, while the ESG reclassification has simultaneously freed up active managers who were previously sitting on their hands. The combined effect is a demand shock for the sector's equity that has very little historical precedent.

The question worth pressing now is whether the re-rating has run ahead of itself. The bear case is not without merit. Peace talks between the US and Ukraine in late 2025 demonstrated the sector's sensitivity to sentiment, when talks made meaningful progress in November, the STOXX index fell 2.2% in a single session, with Saab dropping 5.5%. Supply chain constraints and skilled labour shortages remain genuine bottlenecks on margin expansion. And a Goldman Sachs basket of European defence names was already sitting 19% below its October 2025 peak by December, even before the broader market turbulence of early 2026.

The bull case, though, rests on something more durable than sentiment. European governments are not making one-off emergency purchases, they are rebuilding defence industrial bases that were deliberately shrunk over three decades. Procurement timelines on current contracts stretch well into the 2030s. The US under Trump has been explicit that European allies can no longer rely on American security guarantees as a free option, which means sovereign defence capability is now a political priority that transcends whichever party is in government. That is a fundamentally different demand environment from anything the sector has operated in since the Cold War.

Selectivity matters a great deal at current valuations. Not every name offers a compelling entry point, and the stocks that have already tripled or quadrupled require strong near-term execution to justify their multiples. The structural thesis for European defence remains intact, but the easy money has largely been made. At this stage of the re-rating, the discipline lies in finding those names where order visibility and margin trajectory still justify the premium, rather than simply riding the wave.