As the world pushes deeper into an AI-driven, electrified economy, metals such as silver that were once taken for granted are emerging as strategic bottlenecks. This is particularly predominant in the U.S., which is seeing massive growth in both data centres and their power demands. The last year saw the U.S. fall victim to China’s strong arm over the critical minerals sector. China’s dominance pushed the U.S to reduce its reliance on Chinese minerals, to avoid future weaponisation. How did they do this? By launching a $12 bn. critical minerals stockpile, titled “Project Vault”. This move is not in isolation, as more deals struck with other mineral powerhouses point to a long-term U.S. alliance to reduce dependence on Chinese supply chains.

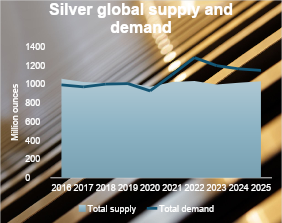

As Figure 1 illustrates, both global silver demand and supply have risen steadily. However, it also highlights how the silver market is now in its fifth consecutive year of structural supply deficits, with inventories at multi-decade lows and refined availability under increasing pressure. The structural supply deficit has persisted due to trade restrictions imposed by China (which accounts for 60-70% of global refined silver output) and delays in opening new mining projects. The last one is particularly significant since new mining projects typically take 8-12 years to bring online, while high-quality mineral ore grades continue to decline.

This is concerning given the growing importance of silver as the critical conductor in photovoltaic cells, high-efficiency power electronics and advanced interconnects. When paired with the accelerating global demand for clean energy, we can see the increasing importance of silver amongst national metal reserves, thus making it more pertinent to study the commodity’s structural, societal change.

In late 2024, China restricted trade of critical minerals with the US, prompting them to seek alternative suppliers of minerals. As a result, the US struck a deal with Australia to help expand their mining sector in late 2025, underscoring the importance of a stable supply of manufacturing metals. These efforts have led to “Project Vault”, a $12 bn. crucial minerals stockpile of key metals designed to mitigate price volatility and shortages by increasing their available supply. Financing has been secured, with the US Export – Import Bank providing $10 bn. in debt and an additional $2 bn. from private investors.

Although protecting domestic manufacturers from supply shocks remains the project’s main priority, one cannot deny the impact of recent Chinese trade relations on this initiative. Therefore, to see this initiative flourish, the US understands the importance of avoiding being undercut by Chinese manufacturers. As such, tariffs on Chinese products will be used to create a price floor for critical minerals, allowing domestic producers to benefit from Project Vault.

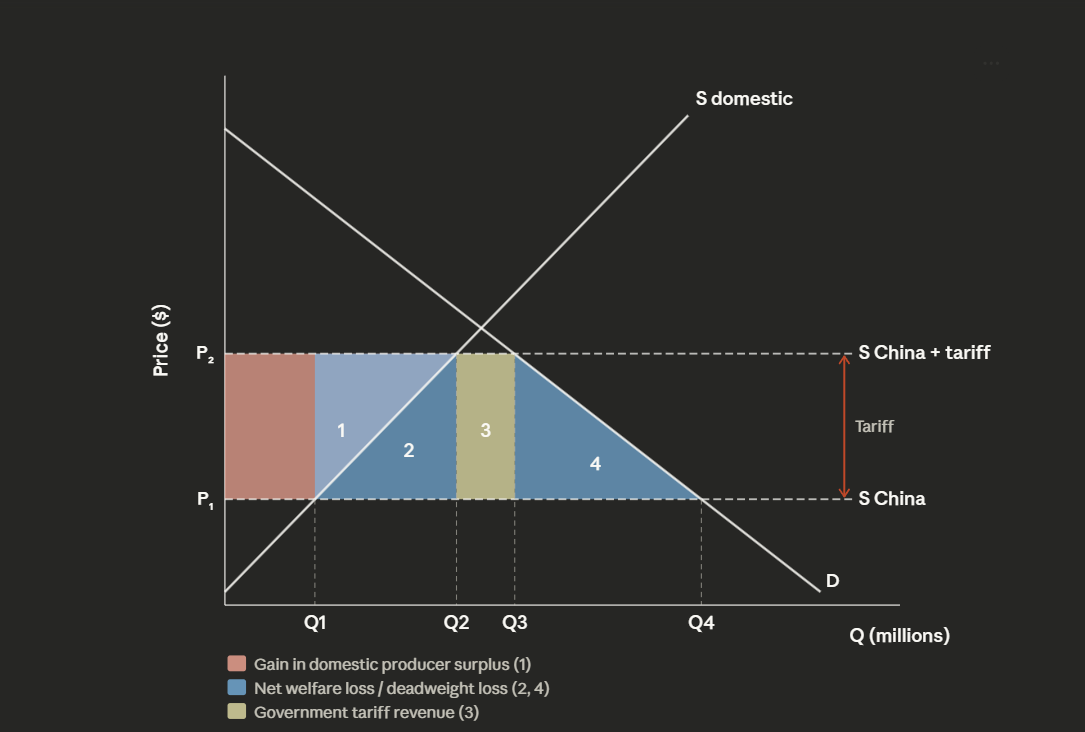

The diagram above illustrates the supply of Chinese imports (as seen by S China) at a low price P1 in the US market. Then, after imposing the tariff (P2 - P1) as seen with the orange arrows, the reduced supply of Chinese imports (shown by the higher S China + tariff) in the US market allows the local US producers to fulfill the difference. This leads to an increase in domestic “producer surplus” - which essentially refers to the benefit producers receive over and above the minimum market price they were willing to accept.

Additionally, in March 2026 the UK business secretary doubled steel tariffs to 50% to preserve British steel production. Under a new major steel strategy, the government seeks to target 50% of steel used in the UK to be made in the UK, up from a current 30%. The strategy is also reducing import quotas by 60% and providing up to £2.5 billion of financing for investment from the National Wealth Fund. This sustained initiative aimed at boosting the UK steel industry can be seen as a response to China’s recent weaponisation of silver - indicating the growing importance of a steady supply of silver for maintaining a reasonable degree of manufacturing independence within developed countries.

As with any national strategy, one move in isolation will not be successful. US nationals are aware of this, hence why a trade zone is being developed with allies including Japan and the EU. They also share concerns over China’s dominance in the critical minerals market and seek to establish sustained trade relations to counteract this.

On 6 January, China targeted Japan with new export restrictions on dual-use technologies including rare earths and permanent magnets in direct response to Prime Minister Takaichi's remarks made in November - who stated that an attack on Taiwan could constitute an “existential threat” to Japan and warrant a military response. Unlike previous rounds of Chinese export controls, this instance ties mineral access to Beijing's foreign policy signalling on Taiwan, marking a significant rise of using economic policy to achieve diplomatic objectives. Despite over a decade of strategic investment in supply-chain diversification, Japan still imports roughly 63% of its rare earth metals from China, highlighting the difficulty of eliminating deep structural dependencies even with sustained political will and capital commitment.

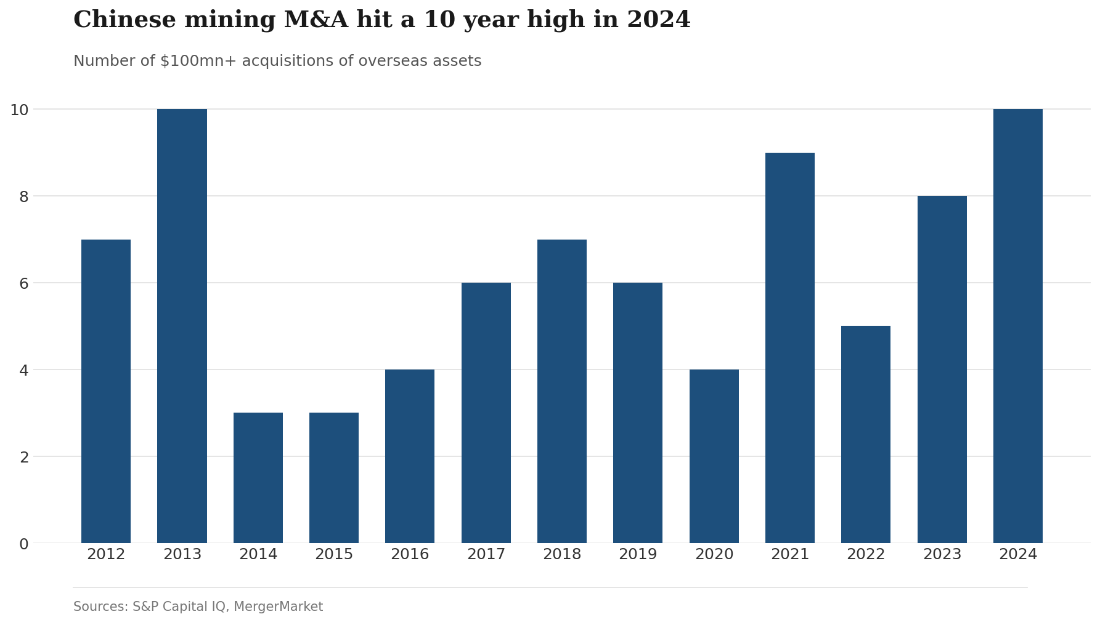

Furthermore, the US struck a minerals deal with Mexico, showcasing the extent to which the US will go to diversify its trading partners geographically to withstand supply-side shocks. When collectively looking at this deal, along with the trade zone, Project Vault and the announcement of Pax Silica - another US strategic initiative launched to secure and diversify AI and semiconductor supply chains - it is clear that the US is willing to go far to both support domestic manufacturers and avoid potential weaponisation of Chinese critical minerals. The graph (Figure 2) below illustrates this point, as Chinese acquisition of foreign mining assets has soared. This has steadily increased China’s influence over the critical minerals sector, hence why collective action from all other major manufacturing countries to secure their own reserves is no longer an option - it’s required.

To secure critical minerals supply for national security and political risk management, I propose a government-led strategy consisting of 3 actions for them to implement:

Overall, by using these 3 levers as part of a long-term national vision for the mineral industry, governments can actively mitigate their exposure to uncertain movements by world leaders and maintain their national reserves of vital resources needed to fuel their manufacturing industries.

Overall, silver’s importance as a strategic material for manufacturing advanced interconnects, electronics, solar panels and EVs is higher than ever before. This is particularly true for the US, as American manufacturing makes up nearly 20% of the global total. Five years of persistent structural supply deficits only point to a market which is seeing a fundamental mispricing of the asset, suggesting silver’s spot price is much lower than it perhaps ought to be. Exploring the commodity from a policy perspective, China’s hegemony over the critical minerals sector has prompted the US to launch Project Vault to create a strategic reserve aimed at preventing industrial shortages, and dependence on Chinese imports.

This is a suitable initiative to protect the critical minerals sector from supply shocks, should future threats arise. However, there are fears over the unreliable and unpredictable actions of the Trump administration - raising the question of whether this is part of Washington’s broader strategy to shield the global critical minerals sector from China’s growing leverage over it, or if this is merely the latest expression of American protectionism to serve its best interests. The US seeks to protect the global critical minerals sector from China’s weaponisation of it, or if this is just another case of US protectionism and wanting to be the main player in every sector.