Private credit is painted as a quicker, cheaper and simpler way to borrow. And you don’t need to tell the public about it. Perhaps that is its very flaw?

The private credit industry is precisely as it is named - non-bank lending to companies.

Their primary function is to provide leverage for private equity. When PE houses take slices of businesses, they often use significant proportions of debt in these ‘leveraged buyouts’. This brings with it the risk of defaults, and so this means public markets view these as ‘speculative-grade’.

Hence, private credit lenders are able to charge a higher interest rate as a risk premium, presenting attractive returns to investors in private credit funds. They are providing liquidity in deals which traditional banks would often avoid due to post-2008 increases in regulatory constraints.

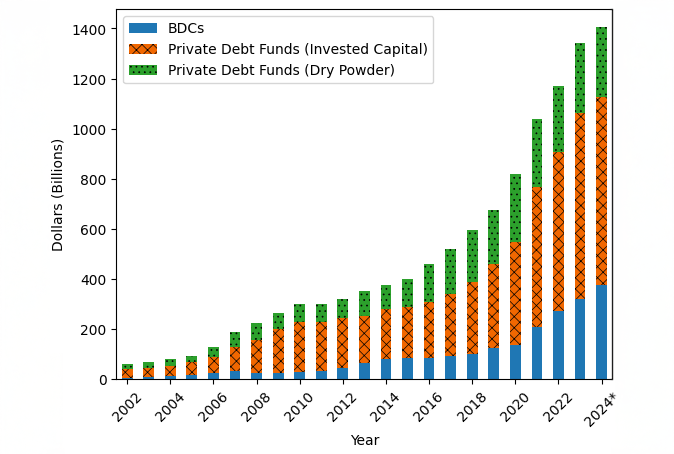

A product of the post-2008 credit crunch, it has ballooned into a massive trillion-dollar industry. It has grown fivefold from 2008 to $2tn in 2026, and is expected to reach $4tn in 2030. Private credit boomed because it offered an alternative to traditional bank loans post-2008, operating largely unregulated outside the banking system and providing PE firms with more desirable loan structures, such as variable covenants (the conditions lenders place on a borrower's financial activities).

The cracks began to appear with the collapse of First Brands, a heavily leveraged American automotive parts conglomerate, which triggered mass redemptions across multiple private credit funds. Pimco has since described the broader industry situation as "a crisis of really bad underwriting," predicting a "full-blown default cycle." JPMorgan has begun marking down loans and tightening lending to private credit funds, while Partners Group forecasts that defaults could double.

This shaky mood has been accelerated by the AI inflection point in Q1 2026. Private credit has become deeply exposed to the AI boom - the OECD estimates the asset class will supply $800bn to AI expansion alone over the next four years, with AI's share of private credit deal value rising from 9% in 2024 to 34% in 2025.

Flashes of the future of AI, such as Claude Code and Citrini Research’s viral piece with dystopian predictions, meant investors questioned the future prospects and valuation for software-based companies. This anxiety didn’t stay in equities - it travelled through the industry.

Doubts about software companies led to doubts about PE firms holding significant stakes in them, which fed into doubts about whether those PE firms could service their private credit loans. The value of highly leveraged companies came into question, triggering redemption requests. This builds on a previously poor situation; more than 40% of private credit borrowers had negative free cash flow at the end of 2024, meaning a large share of the underlying companies were not generating enough cash to comfortably service their debt (Bloomberg).

The issue? Private credit funds are fundamentally illiquid assets. They are long-term and hard to trade and cannot always be sold quickly without damage. Hence, dressing them up as easy access products for retail investors - by alternative asset manager Blue Owl, for example - meant the investors are left with a misunderstanding.

Blue Owl were forced to ‘gate’ their fund, to prevent a ‘run on the bank’ style situation. Funds like Blue Owl operate with a 5% quarterly redemption cap - meaning investors can only withdraw up to 5% of the fund's value every three months. This is built with the intention of preventing funds from haemorrhaging, so funds can effectively manage their underlying assets instead of being forced to liquidate with poor timing.

When confidence wobbles, however, this cap does the opposite: it incentivises investors to request more than they actually want, because they know access will be rationed. Cliffwater, Morgan Stanley and BlackRock all hit this trap in Q1 this year, recording record redemption requests of 14%, 10.9% and 7.9% respectively. Overall, this illusion of illiquidity has fuelled a self-reinforcing problem, reminiscent of the effect of inflationary expectations on price levels.

The illusion arises because private credit is fundamentally opaque. Unlike public markets - where a company's rising borrowing costs and valuations are visible in time, forcing discipline - private credit operates in the dark. The FT’s Lex column correctly notes that financial crises are often predicated on valuations and borrowing being inflated beyond reality.

The darkness shrouding private credit means problems only become visible after they've already become serious. Crucially, both the lender and the PE sponsor have strong incentives to quietly restructure rather than publicly acknowledge bad loans, neatly called “liability management”. One tool is "payment-in-kind" interest rollups, where a borrower unable to meet interest payments simply adds the unpaid interest onto their debt pile instead. This kicks the problem down the road rather than resolving it.

The numbers hint at how much is being swept under the rug: Goldman Sachs Asset Management identified around 150 debt-to-equity swaps in the European private equity universe since 2017 - cases where a PE firm failed to repay its debt and handed over equity instead. Over the same period, only four companies filed for public bankruptcy. The rubble is there; it's just been carefully hidden - and you can’t blame investors for getting jittery about what these credit funds may be hiding from them. A slight jolt causes a quake.

Finally, private credit funds are not even the start of the chain - they borrow themselves, drawing capital from pension funds, insurers and banks to fund their loans through ‘back leverage’. This creates a chain: if the underlying loans deteriorate, pressure travels upward through that chain quickly.

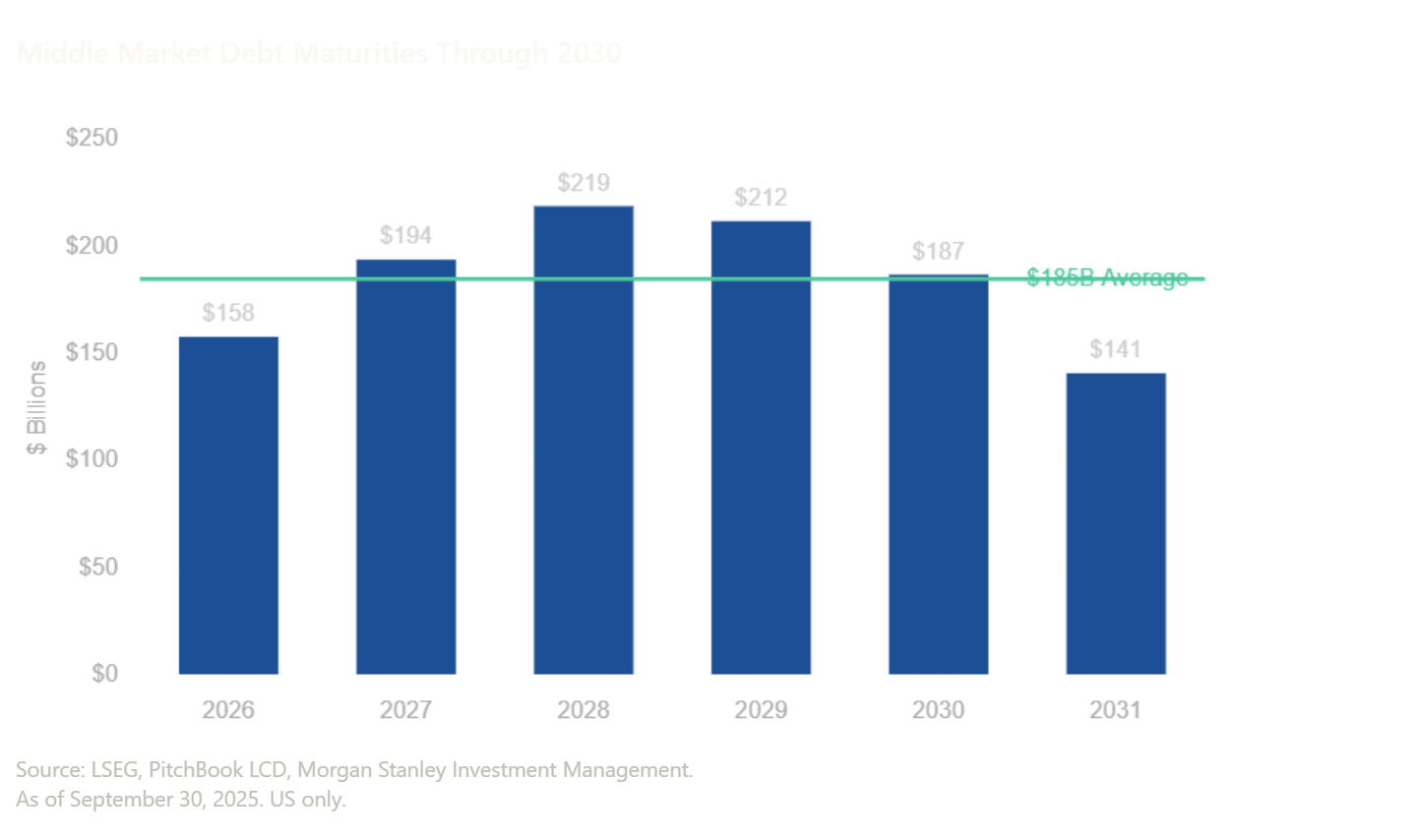

This risk shouldn't be overstated - roughly 65-70% of money lent is equity-funded, a far healthier ratio than traditional banks - but it is real. Add to this a looming maturity wall: middle-market US companies have over $150bn in debt due for repayment every year from 2026 to 2031. Plenty of refinancing is on the horizon, but the willingness to lend may be harder to come by.

The so-called “crisis” does not stop at investment-grade private credit; across Asia and Africa, private credit markets take all kinds of forms, but seem to be following the same pattern.

Microfinance is one of these forms; it is the concept of providing uncollateralised loans in the name of social business. In other words, billions of dollars of private investment have been funnelled into non-bank lending for the purposes of growth and impact, the developing world’s private credit, which has also been subject to heavy criticism, with rising non-performing loan rates, interest rates, and overall loan quality rapidly decreasing across Asia, Africa and Latin America.

With costs of servicing investment debt so high that consumers are having to face the burden, a report published by the World Bank and the Consultative Group to Assist the Poor highlighted the severity of the situation, with Uzbekistan, Mexico, Uganda, Kenya and Ghana all flagged as countries with exorbitant interest rates being passed onto consumers.

First Brands’ shockwaves, however, are being felt even further. Fasanara Capital, a digital assets hedge fund, ran an on-chain tokenised strategy that involved First Brands. This strategy was used as collateral on the Morpho protocol, a major lending and borrowing platform in decentralised finance. When the underlying fund (First Brands) marked down exposure tied to the bankruptcy, the token's net asset value slipped about 2%, pushing highly leveraged borrowers close to liquidation and tightening liquidity on the platform.

CoinDesk estimates that private credit funds stand at nearly $5bn, with a 74% growth in the past year, perhaps a recipe destined for disaster. Tokensing private credit wraps an already opaque, illiquid, and increasingly stressed asset class into crypto infrastructure that most users don't understand, with no legal framework to fall back on when things go wrong.

To close, the $2 trillion private credit market is defined by its deep opaqueness, where lenders and firms have a mutual incentive to hide troubled assets in the shadows of the financial system. This lack of transparency has created a precarious structure, where a sudden loss of investor confidence is all it takes to illuminate the enormous risks that the world now needs to watch out for.