.png)

This has come at a particularly crucial time. August is notorious for thin liquidity, with market depth in Treasuries and FX typically well below average. In such conditions, even modest flows can translate into enhanced price movements due to a lack of volume, and players, with this year proving no exception. Treasury yields have experienced large swings, FX has traded in exaggerated ranges, and options markets have lit up with hedging demand, all crying uncertainty.

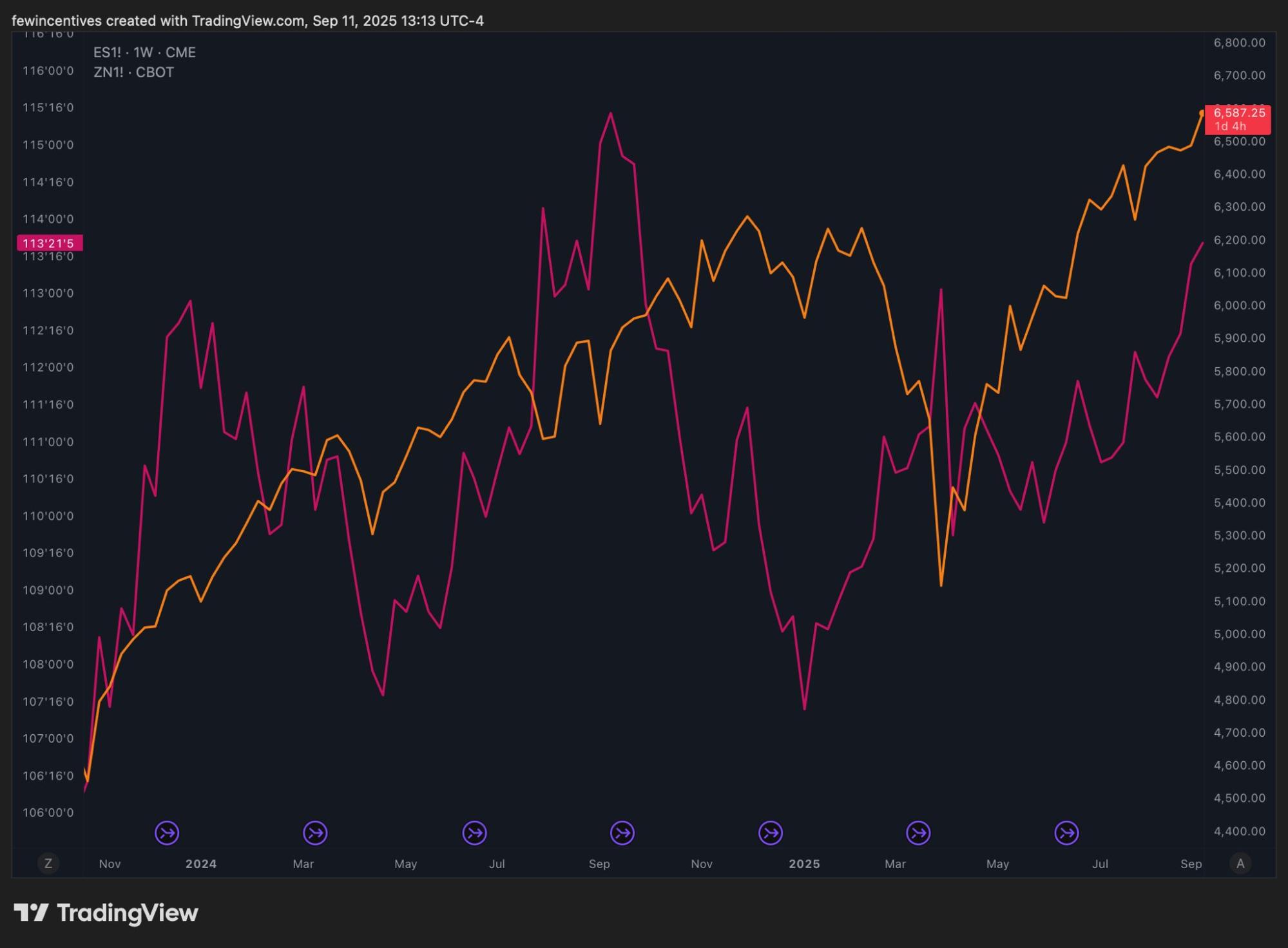

One of the most striking developments has been in the U.S. yield curve. After months of deep inversion, the 2s10s spread is crawling back towards zero. The curve remains inverted, but the re-steepening is unmistakable. However, historically, moving out of inversion has been more destabilising than the inversion itself. Investors are forced to reassess recession probabilities, whilst simultaneously pricing in the risk that policy will remain restrictive for longer, creating mispricing and confusion within the market. This will have been exacerbated this year through Powell’s reluctance to cut rates insofar, when repricing rate cut expectations.

The 5s30s segment of the curve is already positive, reflecting a market view that the long end must carry more risk premium as issuance climbs and inflation uncertainty remains. The danger now is a bear steepening episode: front-end yields anchored by Powell’s data-dependence, but long-end yields rising as supply of longer bonds rises, and term premia are driven up by investors demanding more. This leads to credit spreads widening, as extra compensation is demanded for higher risk corporate bonds due to rising rates from Treasury bonds, and worsening financial conditions.

This could suggest that the return to a ‘normal’ curve is being driven by long-end yields, with less from shorter term bonds. This may, consequently, tighten financial conditions and put stress on credit and risk assets, which may be early warning signs of the recession the Fed is so desperately trying to avoid.

SOFR futures front end has repriced aggressively. Contracts that once pointed to 100bps of easing are now closer to 60–70bps, reflecting Powell’s refusal for imminent, deep cuts, coupled with sticky inflation and a cooling labour market. But markets are still betting on more rate cuts than Powell has hinted at, meaning there’s room for investors to adjust if the Fed keeps pushing back.

The swaptions market reveals more uncertainty. A swaption is an option on an interest rate swap, giving the buyer the right, but not the obligation, to lock in a swap at a later date. Payer swaptions (the right to pay fixed rates but receive floating) benefit if yields move higher, while receiver swaptions benefit from lower rates. Recently, payer swaptions have become more expensive, particularly in popular 1y10y and 2y10y contracts. This “payer skew” shows investors are increasingly willing to hedge against rising long-end yields. In today’s thin liquidity, these hedging flows can be magnified, as dealers adjust their own exposures, creating feedback loops that exaggerate moves in Treasury yields.

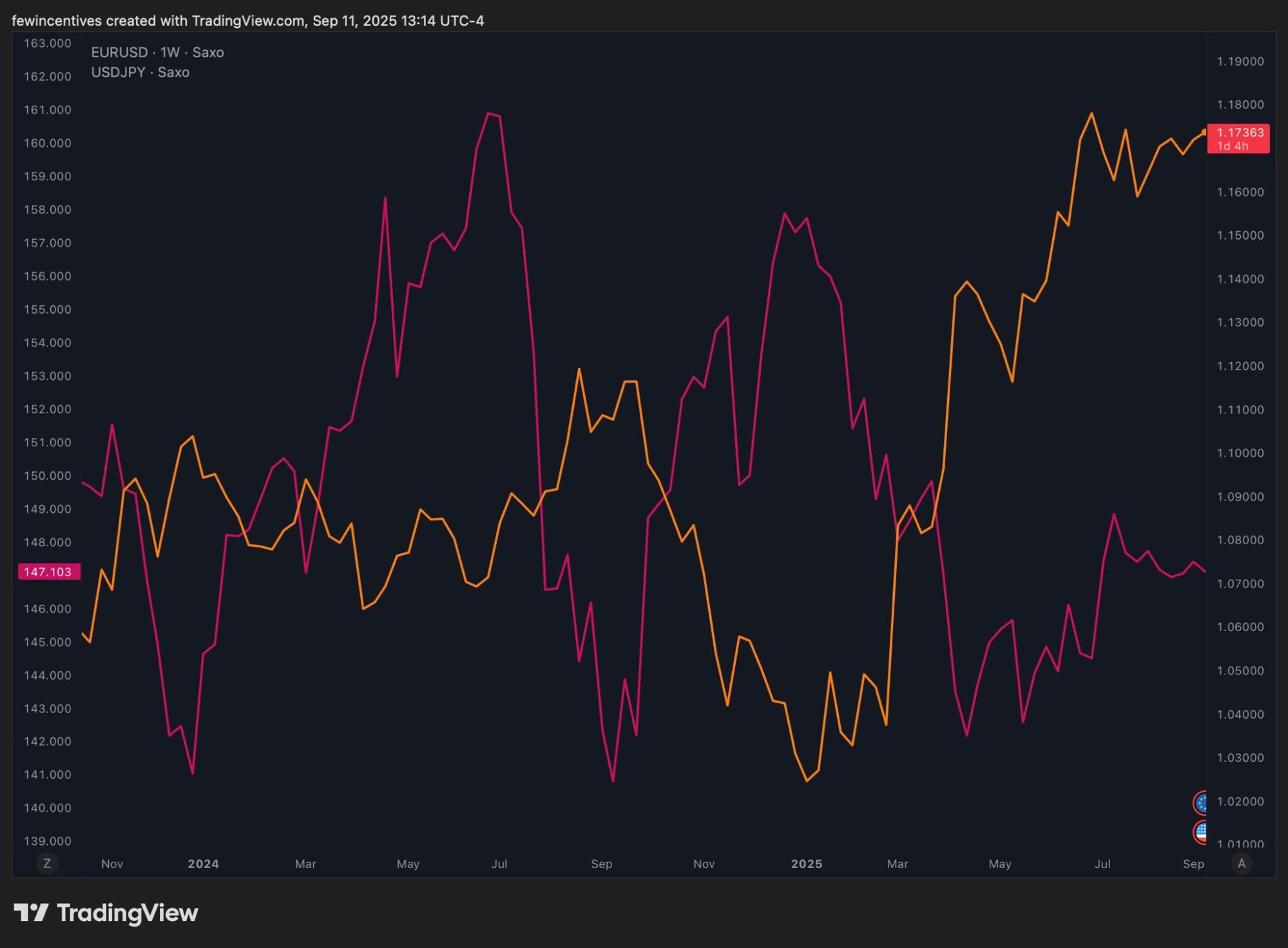

FX options are telling a similar story. Risk reversals remain tilted toward dollar calls, reflecting persistent demand for protection against USD strength. The widening yield gaps between Treasuries and Bunds, or Treasuries and JGBs, continue to underpin the greenback. In thin August conditions, small shifts in U.S. yields have translated into large swings in G10 FX.

With rate cuts strongly expected by the markets, the market for securitised products is likely to skyrocket massively, with there being two main reasons for this.

The first reason is due to the fact that there will be lower returns on Treasuries, and so investors will look elsewhere to replace those yields. Mortgage-backed and other securitised products offering stable cash flow alongside a better yield, leading them to become an attractive option, whilst still maintaining a moderate risk profile. This shift in demand will cause an increase in price and tighten spreads within the market.

The second reason is due to the lower cost of borrowing for consumers and businesses, increasing total borrowing value. As lending grows, more loans can be pooled into securitised products, expanding the supply and variation of these products. This increased supply not only matches demand but will also allow for investors with higher risk appetites exposure to a wider range of products, creating opportunities for both issuers and investors.

Consequently, the possibility of rate cuts will boost market activity within securitised products, as demand increases through more attractive yields, but also by increasing supply through larger lending volumes. This could make securitised products one of the most active and important sectors within fixed-income markets in the coming months.

In FX, the story is simple: higher U.S. yields continue to support the dollar. EUR/USD has drifted lower as the gap between U.S. Treasuries and German Bunds has widened, while the Japanese Yen remains constrained by the stark yield differential with Treasuries.

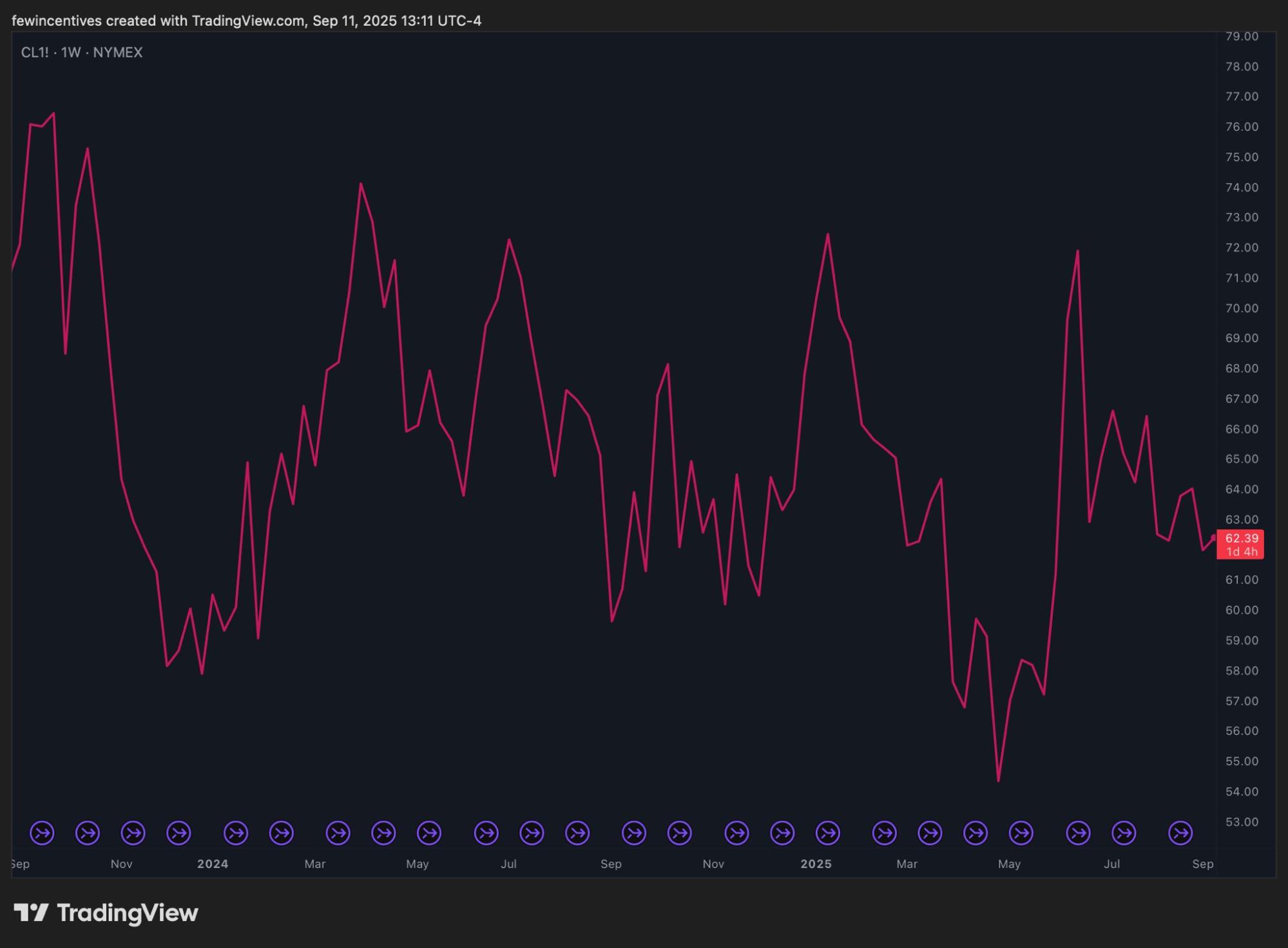

Commodities add another layer of complexity. Oil prices have traded in choppy ranges over the summer, and options markets show a bias toward upside protection. For the Federal Reserve, sustained oil price increases could be problematic. Higher oil prices risk pushing inflation expectations upward just as the Fed is signalling caution on rate cuts, potentially forcing policymakers to adopt an even more hawkish stance.

Equity success today, the S&P 500 and Dow Jones have both reached all-time highs, is due to strong expectations of rate cuts with a decision to be announced on 17th September. This could lead to even greater highs in the short term as investors get over-excited at the possibility of renewed economic growth. However, when this falters, the come down could be devastating. If key data post-cut isn’t enough, then investors may be spooked into pulling their money out, leading to a sharp crash in prices. This, coupled with inflation that is now harder to control due to lower rates, could lead the US, and subsequently the global economy, into a period of economic downturn.

In my view, markets are currently navigating a delicate balance between anticipation and reality. Investors are pricing in imminent rate cuts, yet inflation remains sticky and economic growth slow, creating a sense of uncertainty that is reflected in Treasury yields, the yield curve, and derivatives markets. I expect securitised products to become a particularly active space, as lower rates both stimulate borrowing and make these instruments more attractive to investors. Meanwhile, FX and commodities continue to react to broader macro pressures, and equities appear to be pricing in more optimism than fundamentals might justify. Overall, while there are clear opportunities, I believe the coming months will be defined by heightened sensitivity, where small shifts in policy or data could have large effects across markets.