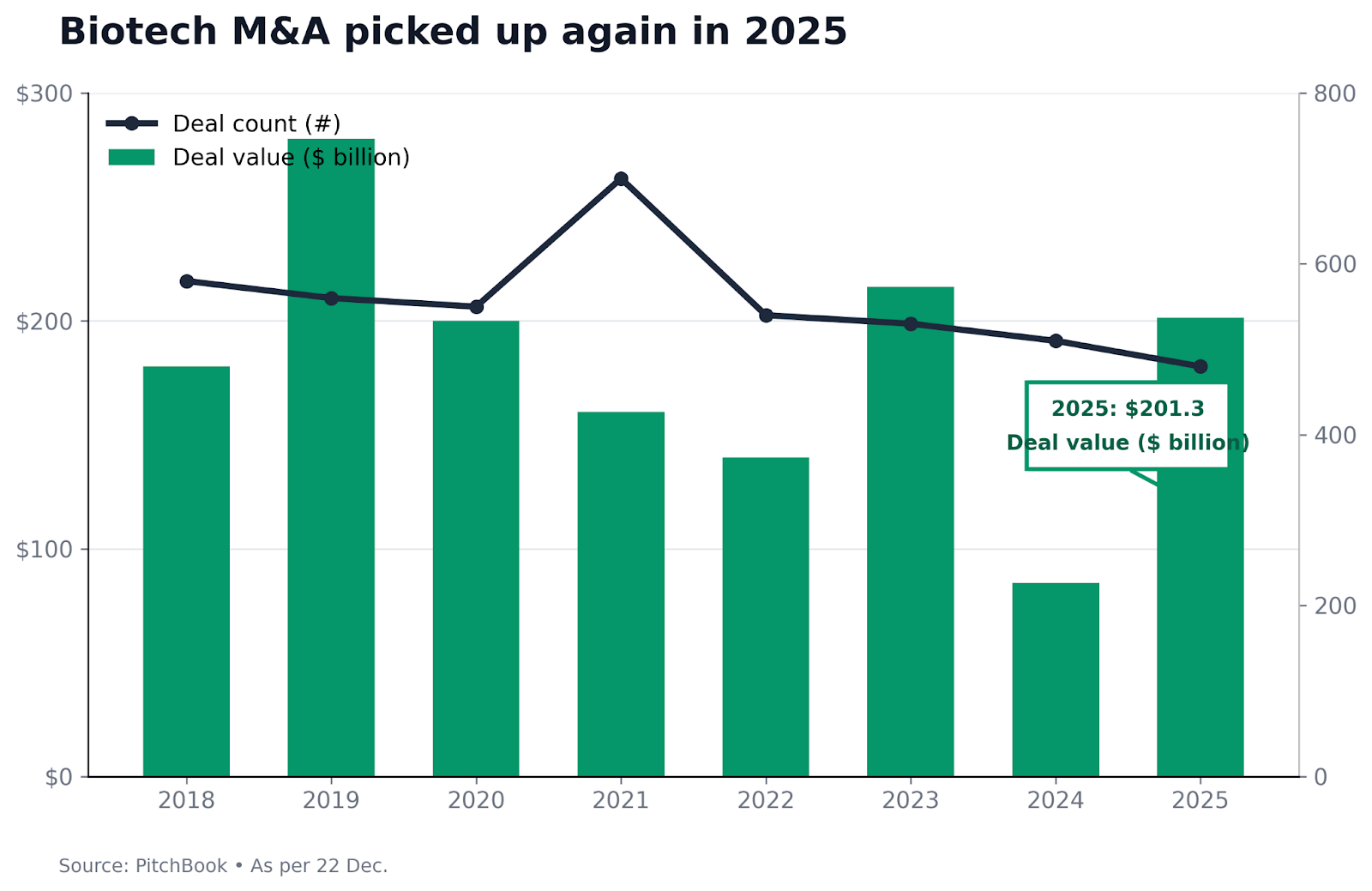

The pharmaceutical sector enters 2026 with major patent expiries, a shift from scarcity to scale in obesity drugs, stricter government price controls and a sharp rise in M&A. The GLP-1 obesity drug market is shifting from unconstrained growth to a competitive industry with pricing pressures and the launch of oral formulations. At the same time, patent expirations are threatening around $170 billion in annual sales by 2032. This is forcing major pharma companies into aggressive acquisitions to fill looming revenue gaps.

Just two weeks into 2026, $9.2 billion in pharmaceutical deals have been announced, signalling the M&A momentum from last year will continue. AI and advanced tech are also shortening R&D timelines by cutting drug discovery periods. Beyond product competition, tighter government price controls are affecting quarterly results. To illustrate the divergent challenges and strategies at play, we examine three companies - Novo Nordisk, Merck & Co, and Pfizer.

Novo Nordisk, the Danish giant, begins 2026 aiming to retain leadership in the expanding GLP-1 segment while adapting to intensifying competition. The company launched its oral Wegovy weight-loss pill in the U.S. in early January priced at $149 per month for initial doses, a level which aims to broaden access. The uptake of 3,071 prescriptions within the first 4 days of the pill’s launch gives some early validation to the strategy of expanding beyond injectables. Simultaneously, Novo’s shares rose as investors reacted to this milestone, which they see as a strategic move against U.S. rival Eli Lilly’s GLP-1 portfolio. However in 2025, Novo cut its full-year sales and operating profit guidance multiple times as its flagship products slowed and market penetration for Wegovy and Ozempic lagged earlier projections. Eli Lilly, in contrast, has surged with tirzepatide - based drugs Mounjaro (for diabetes) and Zepbound (for obesity) becoming the world's best-selling drug franchise in late 2025. As a result, investors increasingly view the GLP-1 market as a competitive battleground where pricing and coverage matter as much as clinical efficiency. Novo’s performance in 2026 will therefore hinge on its ability to convert early momentum into broader market penetration while defending margins against both Lilly’s offerings and compounded alternatives. If it can expand patient access without aggressive price discounting, Novo could trade at a modest premium to historical averages.

Merck’s story this year revolves around its dominant cancer immunotherapy, Keytruda which accounted for nearly half of the company’s revenue in 2024. Patent expiries expected around 2028 are set to expose Keytruda to biosimilar competition that could materially erode sales in the years to follow. The firm’s performance last year, including higher third quarter sales driven by Keytruda’s growth, despite declines in other segments, illustrates how the company has extended the drug’s lifecycle. But this approach highlights Merck's structural weakness with a significant reliance on a single asset potentially increasing uncertainty for investors.

Analysts estimate Keytruda’s sales could peak around $33-34 billion by 2028 and fall sharply as competition increases. Merck’s strategy includes pairing Keytruda with internal assets and pursuing lifecycle management to preserve its market position. However the industry’s history with biosimilars, such as AbbVie’s Humira revenue falling sharply after generics entered, underscores the magnitude of the risk. In recent years, Merck has also added companies such as Verona Pharma and emerged as the leading bidder for Revolution Medicines in a potential $32 billion acquisition. This suggests a deliberate focus on late-stage, de-risked assets that could help offset future declines through loss of exclusivity. The challenge is that acquisitions alone cannot replicate the earnings scale of a long-protected blockbuster. Overall, weak pipeline delivery or earlier than expected biosimilar penetration would likely trigger a valuation reset as Merck’s growth prospects are repriced.

After years of outsized revenues from Covid-19 vaccines and treatments, Pfizer’s core pharmaceutical and vaccine business is reverting to pre-pandemic patterns. The company has provided guidance for full-year 2026 revenue in the range of $59.5 billion to $62.5 billion, down from its 2025 forecast reflecting both declines in Covid product sales and losses from exclusivity on older products. Pfizer has been trying to actively reshape its portfolio with a recent licensing agreement granting it access to Novaxax’s Matrix-M adjuvant technology for future vaccine development. Moreover, Pfizer’s acquisition of Metsera and acceleration of obesity compounds signal a desire to build new growth vectors. Despite these moves, Pfizer’s stock performance in late 2025 and early 2026 reflect uncertainty about the near future, with shares trading well below pandemic peaks. If the business cannot show measurable growth from its diversified portfolio and emerging obesity drugs it could continue to trade at a valuation discount.