As we enter 2026, PayPal is entering a pivotal moment in its future. Long seen as one of the dominant players within online payments, PayPal has built reputation and scale through early-mover advantage. However, competition is now rising with PayPal’s branded checkout button becoming less visible due to the rise in competitors such as Apple Pay and Shop Pay. This article will discuss the challenges and risks facing PayPal and whether the stock is potentially undervalued.

PayPal is one of the largest digital payments platforms globally and has a few key revenue drivers. Its largest driver is the branded checkout business line, such as the PayPal button or wallet on online payment portals. This is followed by its unbranded processing line, where merchants integrate PayPal’s payment rails without the PayPal branding, such as Uber. This second income stream delivers lower margin revenue but has been the main contributor to PayPal’s recent volume growth.

Following PayPal’s Q3 2025 earnings report, total payment volume increased by 8% year over year and revenue grew by 7%. This shows continued growth, but at a much slower pace than in previous years. Free cash flow of $2.3 billion remains a clear strength of the company’s financial position. Despite this, investors no longer view PayPal as a high growth fintech firm and increasingly believe the business is not accelerating.

In terms of valuation, PayPal is currently trading at a forward P/E ratio of around 10x. This is significantly lower than competitors such as MasterCard at 33x and Adyen at 31x. The gap suggests the market expects weaker growth from PayPal relative to its peers, likely reflecting concerns around its business model and competitive pressures. The EV/EBITDA multiple tells a similar story, standing at 8.35x compared to an industry average of around 12x. These discounted multiples could point to an undervalued stock with recovery potential, or they may signal structurally limited growth prospects.

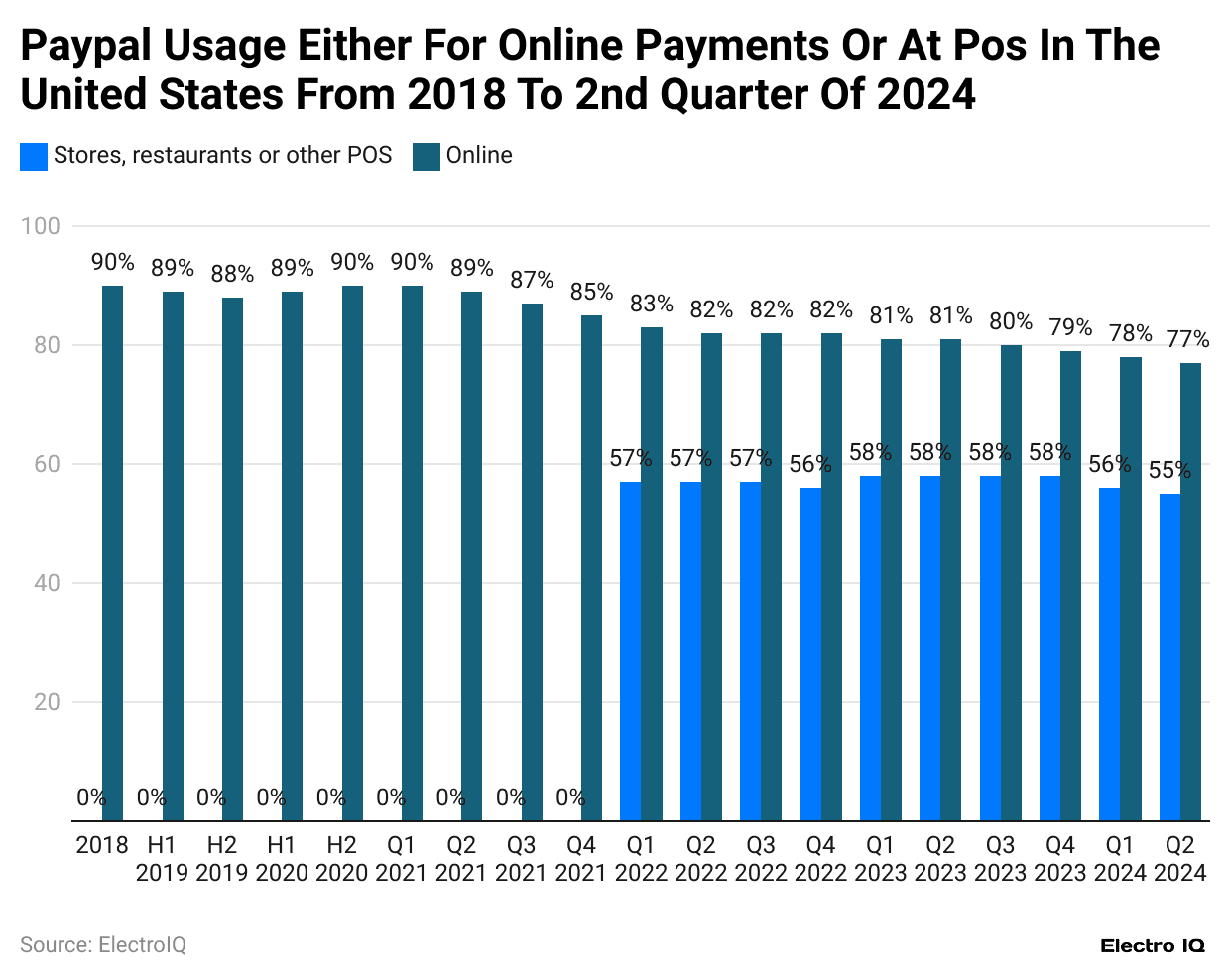

One major risk for PayPal, highlighted by the Financial Times, is that the firm is losing market share in the branded checkout market. Apple Pay and Google Pay dominate mobile checkout, while Shop Pay has become the default payment method for millions of Shopify stores. As a result, the PayPal button is often pushed further down the checkout screen, reducing visibility. Even small losses in market share can have an outsized impact on profits because branded checkout is PayPal’s highest margin business. The key concern is that this pressure is structural rather than temporary, as it reflects lasting changes in consumer behaviour rather than short term competition.

Another significant risk, noted by Yahoo Finance, is the faster growth of unbranded processing compared to branded checkout. This segment is attractive to merchants because it is flexible, but it earns lower fees for PayPal. If unbranded processing continues to outpace branded volumes, overall payment volume may rise while the take rate falls, compressing blended margins. This shift raises fears that PayPal could gradually resemble a commodity payments processor such as Stripe or Adyen, rather than a differentiated consumer facing platform.

A potential opportunity for PayPal is the recent deal agreed with OpenAI, which will see PayPal integrate its wallet and payment network directly into OpenAI’s platform. This allows users to make purchases within ChatGPT using PayPal while benefiting from its consumer protections. Strategically, this could help lift branded checkout volumes and offset some of the share losses to Apple Pay and Shop Pay. It also positions PayPal as an early mover in AI-enabled commerce, an area with long-term optionality. Markets responded positively, with the stock jumping around 11% following the announcement, as reported by Yahoo Finance. That said, the durability of this upside will depend on execution and whether usage meaningfully scales through 2026.

Another key catalyst is the continued expansion of PayPal’s Venmo platform. Venmo has a younger, mobile-first user base and remains one of PayPal’s strongest consumer assets. The company is actively shifting Venmo beyond peer-to-peer transfers into everyday commerce, including online checkout and in-store payments. If successful, this reduces PayPal’s reliance on the slowing branded PayPal button and strengthens its relevance with younger consumers, where long-term payment behaviour is still being shaped.

As PayPal enters 2026, the company is at a critical inflection point, trading at a significant discount to peers. However, the key question remains; is PayPal undervalued or are there limited growth opportunities. The evidence somewhat points to the latter with the declining visibility of is high-margin checkout button and margin pressure from the growth in unbranded checkouts. However, catalysts such as the deal with OpenAI and the growing Venmo monetisation mean that there is definitely potential for PayPal to recover in 2026.