.png)

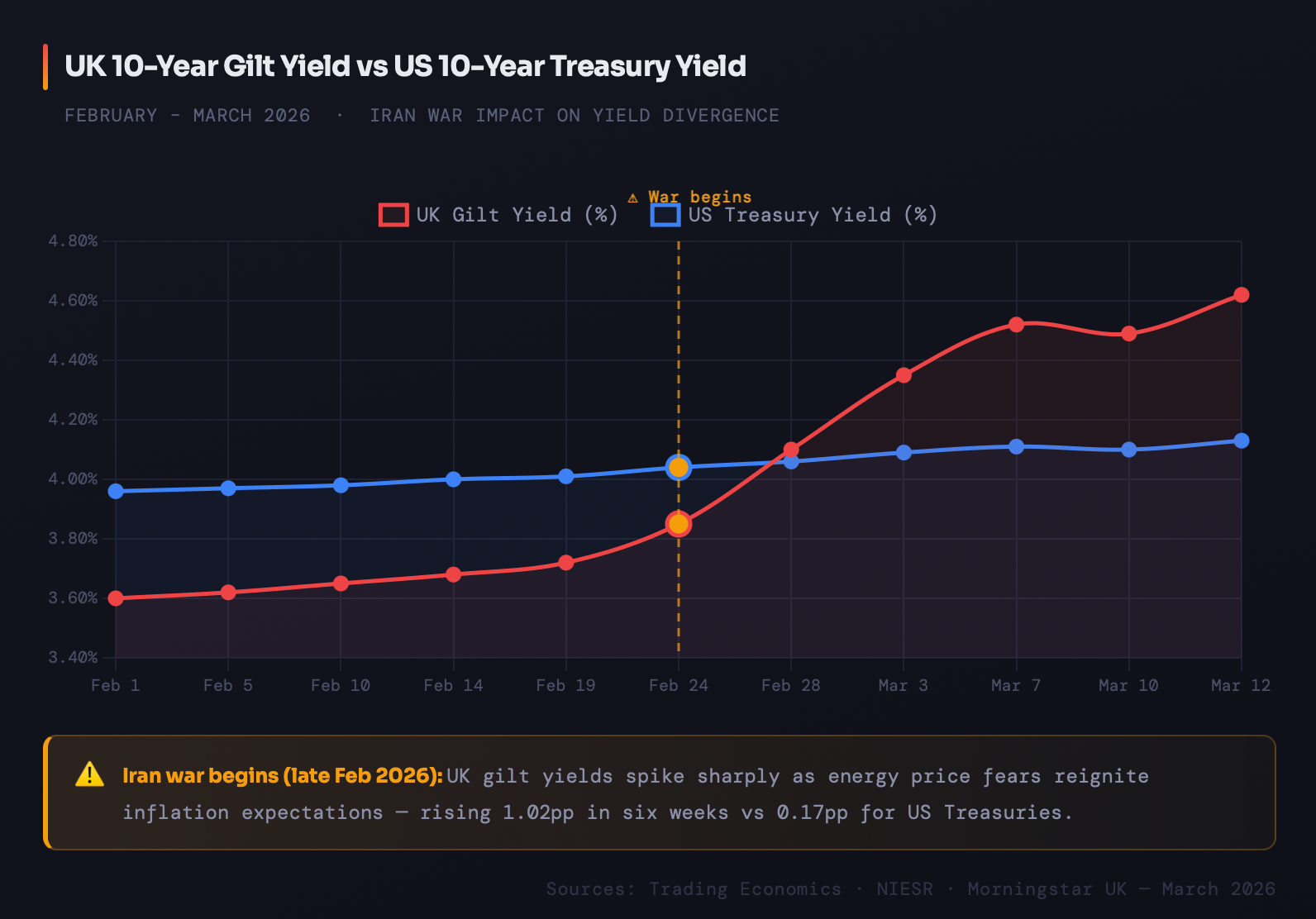

UK gilts experienced their most challenging week since the pension fund crisis of 2022. The 10-year gilt yield increased by 0.39 percentage points to reach 4.62%. Likewise, in the United States, the 10-year Treasury yield also rose, climbing 0.17 percentage points to 4.13%, marking its sharpest weekly movement since Trump's “Liberation Day” tariffs last April.The disparity between these yields highlights where market pressures are most acute, yet again reinforcing Britain’s vulnerability to international supply-side shocks caused by foreign conflict.

For Britain, these rising yields are significant as they increase the cost of government borrowing, which is particularly depressing given the current fiscal climate. As yields climb, the UK government incurs higher interest payments on its debt, which reduces available funds for public spending on sectors such as education, healthcare, and infrastructure, thus increasing the likelihood of further civil unrest through strikes and protests. However, this financial pressure extends beyond the government, affecting businesses that must reprice loans, banks that adjust their products, and ultimately households. For example, families remortgaging or first-time buyers seeking fixed-rate deals are directly impacted by developments in the gilt markets. Although the difference between the UK’s 4.62% and the US’s 4.13% yields may appear minor, it signifies distinct economic pressures and divergent future trajectories.

As you can see in Figure 1, both UK and US yields are stable, with US 10-year treasury yields constantly higher than UK 10-year gilt yields from February 1st to around February 19th. Towards the end of the month, when the Iran war began, you can see that UK 10-year gilt yields sharply rose from about 3.80% to 4.60% in early March. This is a result of markets pricing the UK as the more pressured economy. Alas, that assumption got dismantled quickly, with the dip on March 10th (from Figure 1) offering brief respite. Although yields pulled back slightly before climbing again to 4.62% by March 12th, these events demonstrate how reactive gilts are current affairs. Any hints of de-escalation are shown in the market, whilst any sign of longer-term, attritional warfare and they rise again. This signals fragility - not stability. The question everyone is asking is; where does this end, and what does this imply?

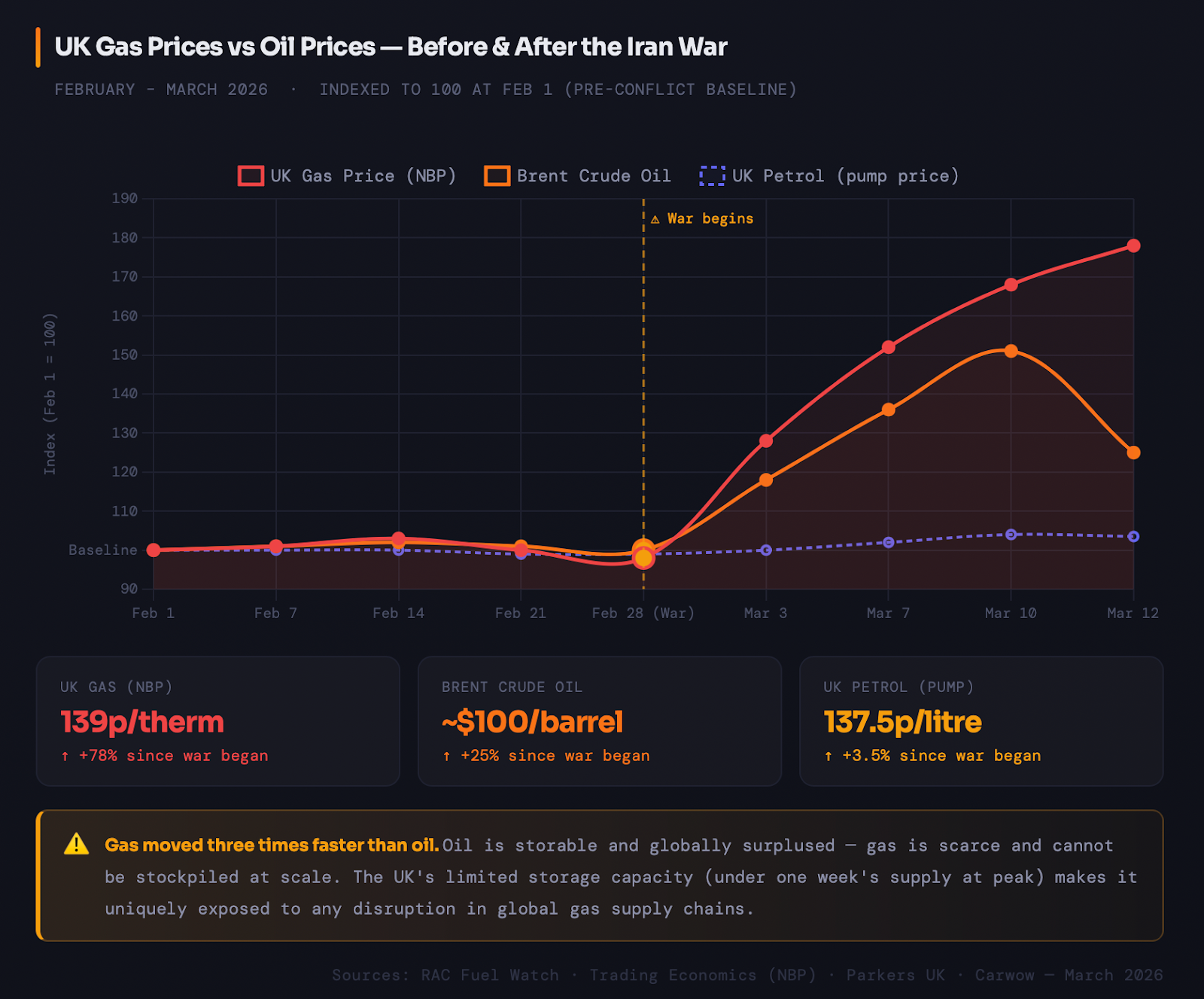

The numbers tell the story bluntly. Since the US’ first strikes on Iran, oil prices rose to $84 per barrel, but UK gas prices hit 139p per therm, up 78% in a matter of days (see Figure 2). According to DESNZ, gas makes up 30.4% of the total generation of UK electricity, compared to oil which only generates 0.6% of the total UK electricity. This is particularly concerning, as, relative to oil, gas has an inelastic supply, since it is more difficult to store than oil. Therefore, due to the lack of reserve gas availability, this scarcity leads to a much higher increase in prices. As a result, the most impact will be felt by households on their energy bills, with Cornwall Insight forecasting that household energy bills could rise 10% from July, pushing the OFGEM price cap to around £1,801 a year for a typical dual fuel household. If the Strait of Hormuz closure persists, figures could even reach £2,500.

Regarding inflation, the OBR have warned that a sustained energy spike could leave UK inflation a full percentage point higher than the forecasted figure for the end of the year. This is important for the Bank of England, given this means that there will be no sign or justification of further rate cuts (two reductions were anticipated by markets this year, though this seems unlikely to happen now), therefore interest rates will remain higher for longer at the current level, or worse rise further. This keeps mortgage costs elevated for longer, reducing buyer affordability, a slowdown in home price appreciation, and a higher risk of default for borrowers and businesses with floating mortgage rates. With this being said, most likely, rates are to be held steady for the foreseeable future given ONS data revealed 0% economic growth in January 2026. Naturally, with inflation cooling back to around 2% levels, rate cuts would be considered to spur economic activity and growth; however, amidst the backdrop of cost-push inflation, the eventual decision is likely to even out to a pause in monetary policy action.

All in all, rising prices combined with slow growth leaves Chancellor Rachel Reeves in an increasingly uncomfortable position, with ordinary households stuck in the middle of this chaos.

The gilt market does not lie: when yields spike, it's because the market has made a judgement about inflation, about growth, factoring in geopolitical tensions. Right now, that judgement is falling heavier on the UK than it is in America, due to structural, not random, reasons - supply and demand. The UK is heavily reliant on gas, and in these current conditions, gas is scarce. When a war disrupts the supply chain that provides Britain with gas, the consequences move fast through inflation, through household bills, through uncertainty.

The US is not immune either, rather it is insulated by its shale oil reserves, its petrodollar status (oil is priced in USD, meaning as oil prices rise, more Dollars are required to purchase oil, thereby increasing demand for the currency and strengthening it, thus ensuring imports are cheaper for American firms and households), and loose labor market giving the federal reserve space to act. The final point is supported by non-farm payroll data, where the US economy lost 92,000 jobs unexpectedly, in sharp contrast to analyst estimates of 59,000 jobs added. This shock marks a significant drop against anticipated gains and indicates a softening labour market, with the unemployment rate rising from 4.3% in January, to 4.4% in February, while previous months saw substantial downward revisions of this figure.

Out of these three factors (natural resources, currency, and soft labour market), Britain has only the latter in common with its transatlantic counterpart. However, this counts for little, given the central bank’s aim to ensure inflation at 2%, meaning that despite low growth figures and poor labour market performance, the chances of rate cuts are as good as zero this year. This contrasts the US, where there is a much greater possibility of rate cuts, due to the lower effect of the conflict on domestic inflation. Consequently, with UK rate hikes being anticipated, this has forced markets to react, as higher interest rates will mean newly issued government bonds will have higher yields, which will incentivise holders of older gilts to sell, causing yields to spike.

With the MPC’s latest meeting concluding with an interest rate freeze of 3.75% following a resounding 9-0 vote, UK bond markets stabilised. Rate cuts will come to the UK eventually, whether that's sooner or later. The question, the one that matters for every household remortgaging this year, is not whether they come, but whether they come before the damage is already done.