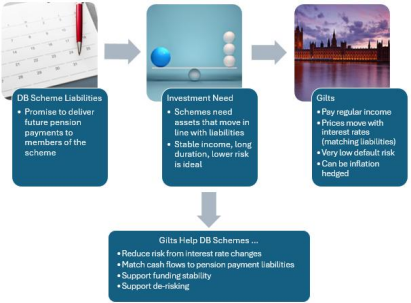

For those who are less acquainted with DB pension schemes and their long-standing appetite for gilts, Figure 1 outlines the basic mechanics of these schemes, as well as the reasons gilts remain well-suited to their investment requirements.

Despite retracting sharply during the week starting the 20th of October, gilt yields in 2025 have been at the highest levels seen in decades, which has profound implications for both returns and DB funding. Long-term UK borrowing costs in September surged to levels last seen in the late 1990s.

From a DB standpoint, the recent rise in bond yields presents somewhat of a double-edged sword. Heightened yields have diminished the present value of future liabilities that DB schemes hold. While gilt values have fallen simultaneously, The Pensions Regulator reported that between 2021 and early 2025, increases in gilt yields reduced liabilities at a faster relative rate than asset values, leading to improvements in aggregate funding levels. UK DB schemes are in their strongest position in years, with an aggregate funding level of roughly 123% in early 2025 compared to just 105% by the end of 2021. Data from the Department for Work and Pensions built on this by declaring that funding levels in the DB pension sector have hit a record high, with just over three-quarters of schemes now running a surplus.

Schemes that had hedged less of their interest rate exposure saw particularly large gains, as falling liability values drove surpluses higher. A prominent example is the Universities Superannuation Scheme (USS). As of their most recent accounts, the DB section, which moved from a consistent deficit to a £10.1 billion surplus by mid-2025, saw assets outperform liabilities by 14.1% annually over the five-year period leading up to August 2025.

By contrast, the inverse correlation between yields and prices has given way to falling market values for gilts in the short term, which can prove particularly challenging during episodes of heightened volatility. In the 2010s, yields remained artificially suppressed due to huge QE measures, but now gilts carry substantially more volatility risk. However, a crucial consideration is that today’s higher yields provide a thicker cushion of income (and expected return) to weather these risks.

Inflation remains the foremost risk to gilts’ real value. The country’s battle with inflation is by no means won. As of the most recent data release, CPI remained at 3.8%, well above the BoE’s 2% target and the highest inflation rate among G7 economies. The good news is that, to analysts’ surprise, inflation has held at the 3.8% level for the three months through to September 2025 and appears to have peaked for this cycle. Many economists now expect inflation to resume a downward trajectory into 2026, where the IMF forecasts the average CPI rate to fall to 2.5%.

For gilt investors, this outlook implies that current yield levels could offer a positive real return over time if inflation moderates in line with expectations. Index-linked gilts, which traded at negative real yields for much of the past decade, have offered positive real yields since late 2022, a fundamentally attractive proposition for DB plans with inflation-linked liabilities. However, inflation risk is not entirely vanquished. Upside surprises, such as commodity spikes, are still possible. Moreover, high inflation directly hits the UK government’s debt costs because a sizable share of gilts are index-linked, adding further pressure on fiscal policy. DB trustees should continue to hedge a certain level of inflation risk via ILGs and swaps in order to protect their liabilities, as it may be bold to assume that nominal gilts alone will preserve real value.

Inflation risk is embedded in today’s gilt market via a significant premium and is a major reason yields remain elevated, but crucially, it may now work in investors’ favour. After years when gilts offered little protection against inflation, the market is finally compensating investors for inflation risk. In effect, gilts now seem priced to reflect inflation uncertainty rather than be undermined by it. If inflation continues to fall, repricing sets the stage for strong real returns ahead. As Figure 3 illustrates, 10-year gilt yields have consistently exceeded the inflation rate since Q3 2023, a signal that real yields are positive and the long-term value proposition for gilts has improved.

Another critical consideration is the UK’s fiscal position and its influence on gilt markets. Investor sentiment is cautious, reflecting the country’s heavy debt-servicing burden. Public debt has roughly doubled as a share of GDP since the financial crisis, and September’s was the second-highest monthly reading since April 2023.

The government’s financing requirements remain substantial. For the fiscal year 2025/26, the Treasury has scheduled £299 billion in gilt issuance, with these plans having been amended (through shorter maturity issuances) to ease pressure at the long end of the curve. Looking ahead, the OBR projects over £50 billion of additional gilt sales over five years, embedding higher borrowing costs as older, lower-yielding debt matures and is refinanced at current elevated rates. Such continued issuance, together with the BoE’s ongoing QT, suggests that the market will continue to demand attractive yield levels to absorb the growing volume of government debt. A society that is aging and continuous demand for high-quality public services will only add pressure to increase spending. This requires a delicate balancing act from the government at their Autumn Budget, as too much austerity could hit growth further, but too much borrowing would undoubtedly hurt investor confidence.

Crucially, investor confidence in the UK’s fiscal discipline is a major swing factor for gilt valuations and was a lesson learned during the mini-budget crisis in 2022. Though pushback has been more muted recently, markets are once again signaling unease over the UK’s fiscal discipline. Demand weakened at a gilt tender on 25 September 2025, which Reuters described as a sign of “impatience with fiscal uncertainty.” Any wavering in fiscal discipline will continue to be swiftly punished by the market.

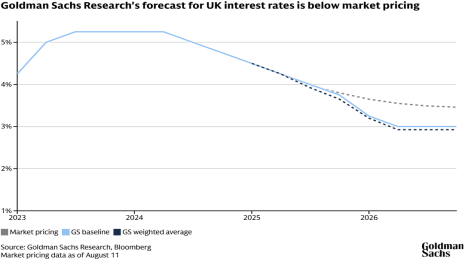

The trajectory of Bank of England policy rates is an important consideration for DB schemes in timing their investments. Since 2024, the BoE has cautiously started undoing previous rate hikes. In its September 2025 meeting, the majority of MPC members voted to hold rates at 4.0%, while a minority took a more dovish stance. This reflects a growing sense that policy may have been restrictive enough to slow the economy and that future moves are likely to be downward, albeit at a careful pace.

Market expectations overwhelmingly point toward cuts in the near future. The surprise stabilisation of inflation at 3.8% in Q3 led investors to accelerate their rate-cut bets. By October 2025, after somewhat soft inflation data, markets are pricing around a 75 to 80% probability that the BoE would cut rates by 25 bps in December. Forward interest rate futures also imply roughly 50 to 65 basis points of total rate reductions over the course of 2026.

Projected rate cuts are generally bullish news for gilt investors. We saw 2-year and 5-year gilt yields in October 2025 drop to their lowest in over a year as markets penciled in policy easing. Expected rate cuts present a compelling case for holding gilts, particularly as we seem to be past peak yield levels and the carry on gilts remains attractive in a world where policy rates will likely drift down. One caveat is that schemes with under-hedged liabilities should be mindful, as falling yields do the inverse to liability values. However, because most UK DB plans have extensive hedging via ILGs or swaps, improved asset-liability matching means a more muted impact on funding if yields decline.

While the case for holding gilts in DB schemes remains strong in the current environment, it is not without vital risk factors. Recent events underscore that even sovereign bonds can exhibit volatility and liquidity challenges. Thus, it would seem sensible for pension funds to broaden their investment approach to liability matching rather than relying solely on UK nominal gilts and ILGs.

Quality corporate debt and overseas bonds often provide a yield pickup and diversification benefit. For instance, a modest allocation to some AA-rated corporate bonds that yield marginally above gilts will boost returns for bearing extra credit risk. Overseas bonds, if currency-hedged, can offer further exposure to different interest rate environments and lower inter-portfolio correlation. As a Russell Investments consultant noted, most schemes are now well-positioned with strong funding, and “maintaining portfolios diversified beyond the UK economy will be crucial” to achieving long-term objectives.

An interesting consideration is that of maintaining some exposure to safe-haven assets or currencies as a form of insurance. In the context of gilts, a “tail risk” scenario could arise from a severe loss of confidence in the UK due to negative speculation following the autumn budget. In such a scenario, GBP could depreciate significantly. Holding a portion of assets in alternative currencies such as the dollar, yen, or franc could provide protection against this risk. These assets tend to appreciate when sterling assets are under stress. For example, if a UK-specific shock hit, the JPY/GBP rate might spike, meaning any JPY-denominated bonds or cash would be worth more in GBP terms, offsetting some of the losses on gilts. The recent First Actuarial briefing on gilts explicitly noted that exposure to safe-haven currencies can offer protection against gilt tail risks, reinforcing this risk management strategy notion.

Perhaps the greatest lesson from 2022 was the importance of maintaining collateral buffers when using gilts and LDI strategies. Diversifying is not only a question of asset classes but also ensuring some assets, such as repos or cash, can be readily liquidated or posted as collateral in stress events. The good news is that LDI managers have built in much more resilience since 2022. Trustees should nonetheless ensure governance processes are in place and that matching portfolios are not overly concentrated in instruments that could become illiquid under strain.

In conclusion, UK gilts remain a compelling investment for UK DB pension schemes and should comprise a significant part of portfolios, even in the face of today’s economic uncertainties. Our research reinforces that holding gilts remains beneficial for most schemes’ objectives. Current yields appear to adequately compensate inflation and fiscal risks, assuming those risks are managed down over time. Moreover, with monetary policy likely easing amidst softer CPI releases, the prospects for capital gains on gilts have improved materially. At the same time, I believe that DB schemes should diversify their matching portfolios to include select non-UK or corporate debt to guard against geographic-specific risks. It would be prudent to review schemes’ hedging levels, as improved funding may lay the ground to increase hedges now to lock in funding gains and de-risk without sacrificing return requirements. Additionally, considering a modest allocation to safe-haven assets or currencies seems reasonable.

Such diversification guards schemes against tail-risk scenarios where any single asset class might underperform. Finally, schemes should continue to strengthen their governance and risk management around bond portfolios. Regular stress-testing of interest rate and inflation exposures, and ensuring collateral sufficiency for LDI programs under various economic conditions, are vital. This is not a hard change in strategic direction but a fine-tuning of the existing strategy to reflect that gilts are inherently more volatile than in previous years. By taking these steps, trustees can better secure their schemes’ ability to meet promised benefits under a range of future outcomes.