After nearly three years of subdued exit activity, private equity firms are cautiously signalling a return to public markets. Blackstone has assembled what its president Jonathan Gray described in Q4 2025 earnings as a "record IPO pipeline," suggesting that equity markets have become sufficiently liquid and receptive to absorb new listings. This shift comes as inflation has moderated and markets increasingly price in interest-rate cuts.

This marks a notable shift from the post-2022 environment, where rising interest rates, valuation mismatches and weak equity markets forced general partners (GPs) to delay exits and rely instead on alternative liquidity solutions such as continuation funds, secondaries and dividend recapitalisations.

The key question for investors, however, is whether this renewed IPO optimism reflects a sustainable reopening of the exit market, or merely a tactical window driven by improving sentiment and a narrow set of high-quality assets.

The shutdown of IPO markets was driven by a sharp repricing of risk. Between early 2022 and mid-2023, the US Federal Reserve raised interest rates by over 500 basis points, pushing discount rates higher and compressing equity valuations.

Higher rates had a double impact on private equity. First, leveraged buyouts became more expensive as debt costs surged. Second, public market multiples fell, making IPO exits unattractive relative to private valuations still anchored to pre-tightening expectations. As a result, many sponsors opted to delay exits rather than crystallise losses, contributing to a growing backlog of unrealised assets.

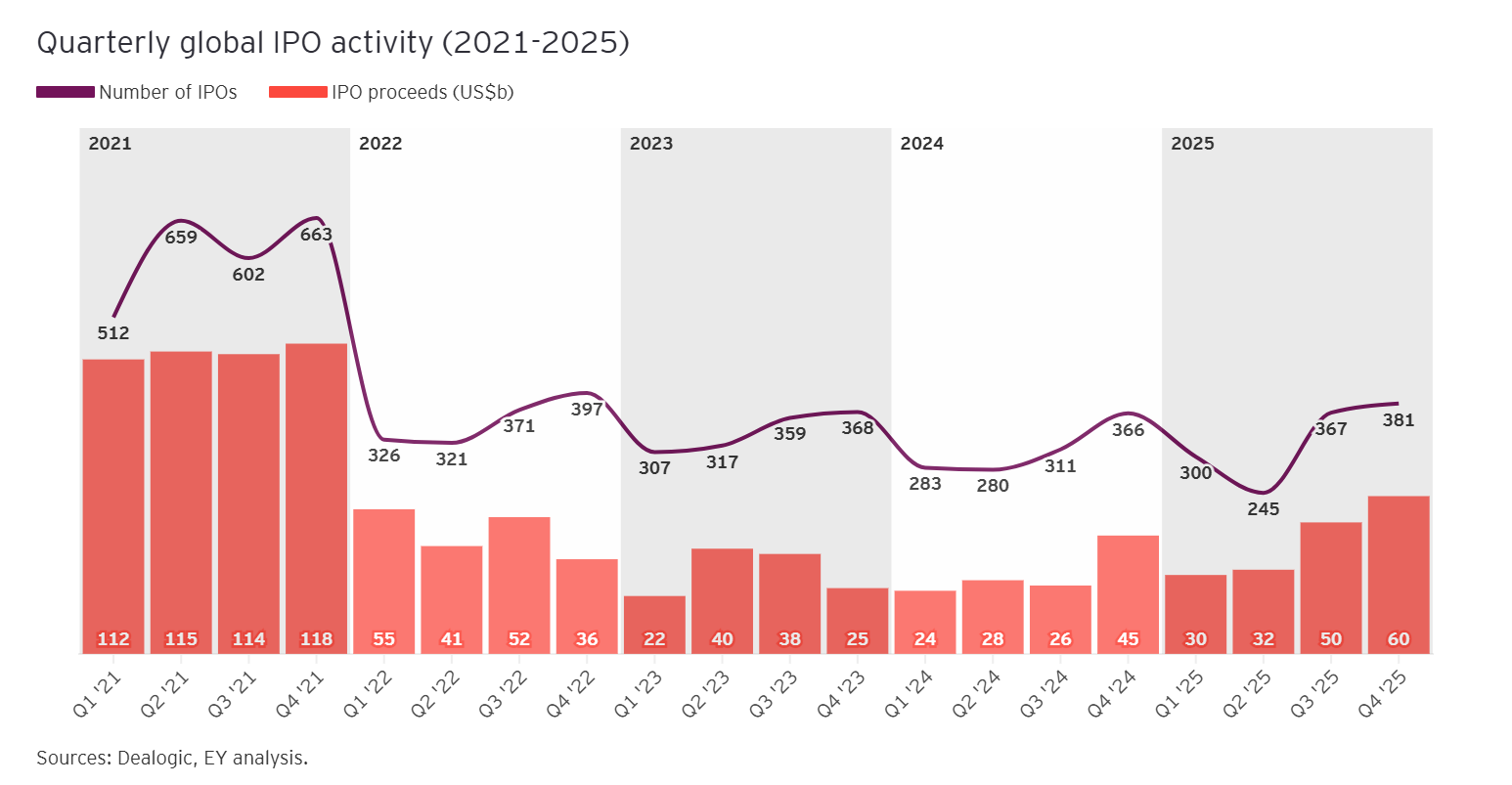

According to EY's global IPO data, global IPO proceeds in 2023 fell to $123.2 billion, down more than 70% from the $453.3 billion peak in 2021.

Two macro forces are underpinning renewed IPO discussions across private markets.

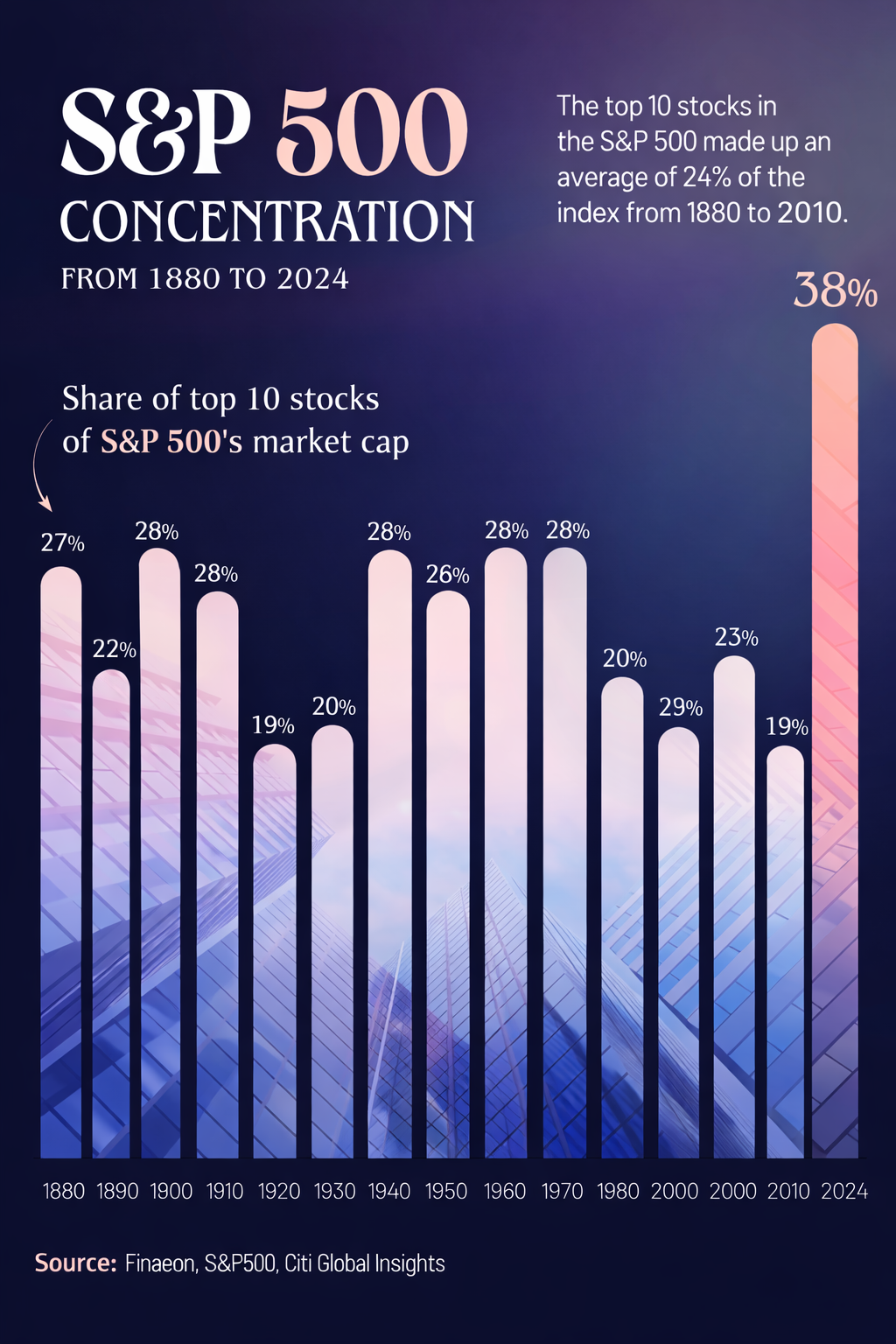

First, public equity markets have regained momentum. Major indices such as the S&P 500 and MSCI World have rebounded strongly from their 2022 lows, equity volatility has moderated and institutional risk appetite has improved, restoring a key precondition for IPO activity: predictable pricing and sufficient secondary-market depth.

Second, interest-rate expectations have shifted. While policy rates remain elevated, futures markets increasingly anticipate rate cuts over the medium term as inflation moderates and growth slows. According to the CME FedWatch Tool, investors are pricing in a growing probability of rate cuts, which mechanically supports higher equity valuations by lowering discount rates. This has narrowed the valuation gap between public and private markets that previously stalled exits.

Blackstone's Jonathan Gray drew a historical parallel in describing current conditions: he compared the present moment to 2013-2014, approximately five years after the financial crisis, when "markets had healed a lot and people were excited about IPOs again." The pattern, he suggested, appears similar: "interest rates went up really quickly in 2022, it scared a lot of people. IPO markets have been closed for a number of years, but now they're opening up." Critically, this reopening has created a window to take "non-buzzy tech businesses, real kind of companies, public and actually find a demand among shareholders."

Recent transactions illustrate this shift. Blackstone's $6.26 billion IPO of Medline Industries - the largest US IPO since Rivian's $13.7 billion listing in November 2021 has been widely interpreted as a proof point that scaled buyouts from the 2020-21 vintage can successfully transition into public markets. The deal's strong first-day performance, with shares closing up 41%, has reinforced confidence that long-held private assets can now find receptive public-market demand.

Despite improving conditions, this is not a return to the free-flowing IPO market of 2021. Instead, exits remain highly selective. Improving market liquidity and shifting rate expectations have created a narrow path to exit for the strongest assets, rather than a wholesale reset of the exit environment.

Assets most likely to reach public markets share common characteristics:

Sectors such as infrastructure, healthcare services, logistics, data centres and select industrials dominate current IPO pipelines. These businesses offer predictable earnings profiles that public investors favour during periods of macro uncertainty.

Conversely, highly levered consumer businesses, cyclical industrials and growth-at-all-costs models remain sidelined. For many GPs, alternative liquidity routes including GP-led secondaries and evergreen fund structures - continue to play a central role in portfolio management. The next phase of private equity exits will be defined less by volume and more by selectivity - a trend that may ultimately benefit both private sellers and public buyers willing to look beyond headline valuations.

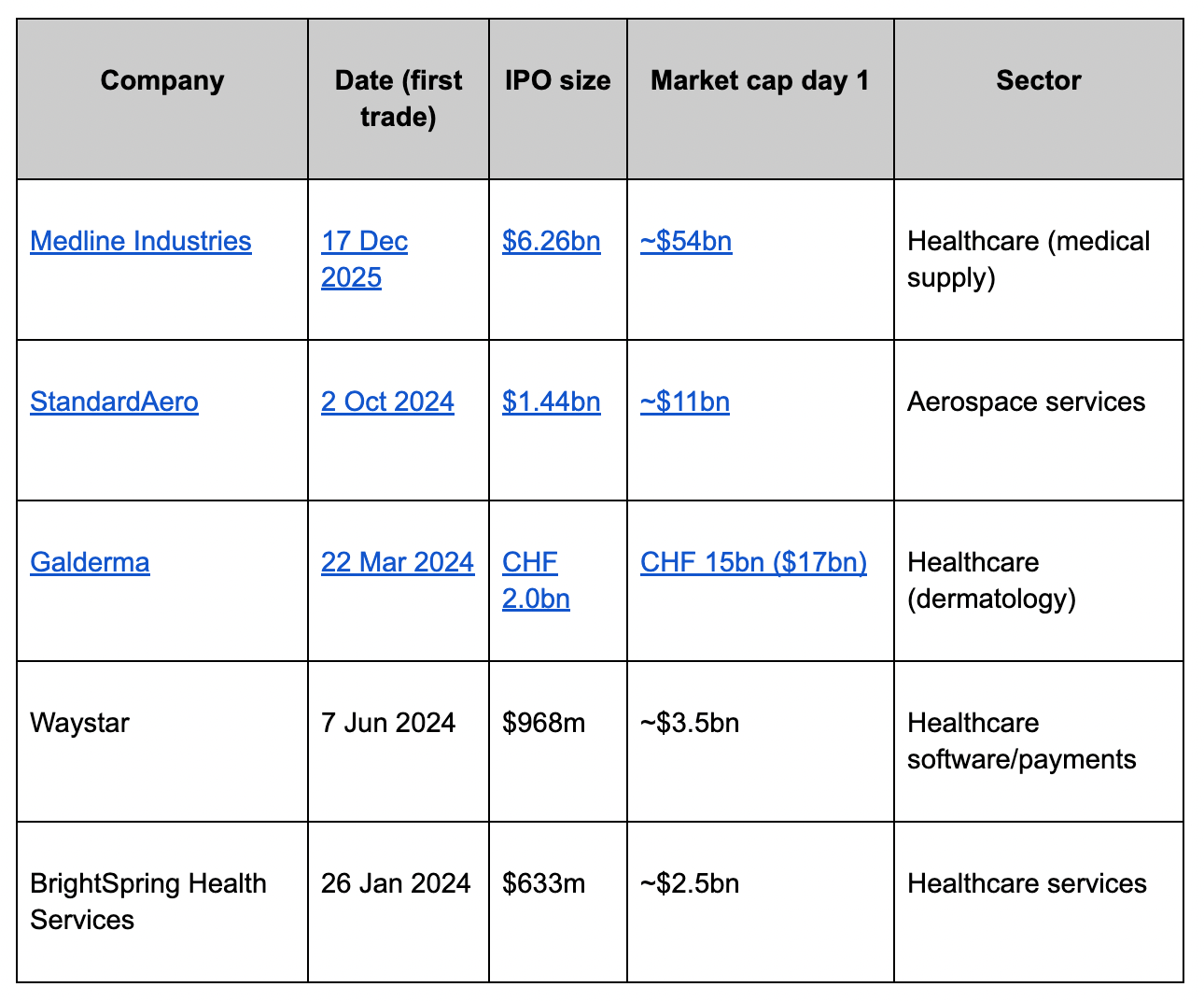

Figure 5 compares prominent sponsor‑backed IPOs where public sources specify proceeds and day‑one market value (figures as reported; FX conversions where given by the source).

Two observations matter for the "selective window" thesis: (1) healthcare dominates among successful sponsor-backed debuts in the period above; (2) dispersion is real - Medline and Galderma saw strong first-day reception, while other listings have shown more modest performance.

For public equity investors, an influx of private-equity-backed IPOs presents both opportunities and risks.

On the positive side, IPOs can expand sector exposure and introduce high-quality cash-generative assets that could offer public market investors an opportunity to diversify away from concentrated exposure to big tech. Infrastructure-linked listings, for example, may benefit from structural demand drivers and, in certain cases, inflation-linked revenue streams.

However, public investors must remain disciplined. Private equity exits are, by definition, seller-driven and timing often reflects a desire to monetise assets rather than long-term public market alignment. As McKinsey has noted in recent research, periods following prolonged exit droughts often favour disciplined investors who focus on fundamentals rather than deal momentum. The question, as Antoine Gara (FT) framed it, is whether Medline and similar listings represent "a referendum for the private capital industry" - can "the largest PE firms start exiting their big deals or would a growing stockpile of ageing deals just continue to grow and grow and grow" - potentially stalling the entire ecosystem.

Investors should scrutinise governance structures, leverage levels and post-IPO capital allocation plans. Crucially, the absorption capacity of public markets will matter. A crowded IPO calendar could pressure valuations, particularly if macro conditions deteriorate or rate cuts are delayed.

Blackstone's confident expanding pipeline signals a meaningful shift in private equity sentiment, underpinned by easing monetary conditions and improving market stability. But this is not 2021 redux.

As Jonathan Gray's 2013-2014 comparison suggests, post-crisis recoveries favour quality over exuberance. The firms finding exits will be those with "real kind of companies" - profitable, scaled, defensible - not those chasing inflated valuations on stretched narratives and speculative growth plays.

For investors, the lesson is clear: scrutinise rigorously, diversify thoughtfully and resist the temptation to assume that all sponsor-backed IPOs are created equal.

The ice is thawing. But only the disciplined will benefit when it melts.