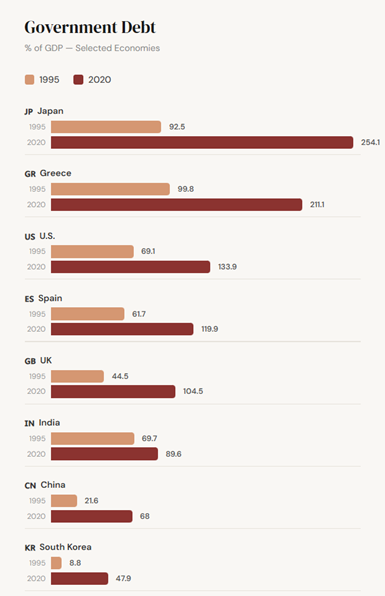

For more than two decades, Japan has ranked highest among developed countries in terms of the debt-to-GDP ratio. However, despite this, the Japanese economy has proven its resilience across numerous crises, ranging from the 2008 Financial Crisis to the COVID-19 Pandemic.

With its known predictability and stability, Japan’s debt-to-GDP ratio was tolerated by investors, as confidence in the Japanese economy was strong. However, credibility waned when Japanese Prime Minister Sanae Takaichi called for a snap election on the 20th of January. Following this, a $135.4bn fiscal expansion plan was unveiled, aimed at promoting economic growth and tackling Japan’s rising cost-of-living crisis.

Lacking a clear path on how this expenditure increase would be financed, Takaichi’s explosive spending bombshell, layered with a subsequent election bidding war, eroded credibility in the government, especially with Japan’s high debt-to-GDP ratio. This was preceded by a $7 Trillion bond selloff of Japanese Government Bonds (JGBs), resulting in a spike in the yield rate.

Preceding this mass selloff, the yields of long-term Japanese debt exploded, which saw some bond yield categories hit an all-time high, such as the 40Y (70 Basis Pts) and 30Y (60 Basis Pts). While in late February, the yield rate of these bonds had retreated from their peak levels, they remained above pre-event levels, emphasising the background investor concern surrounding Japan’s debt-to-equity ratio.

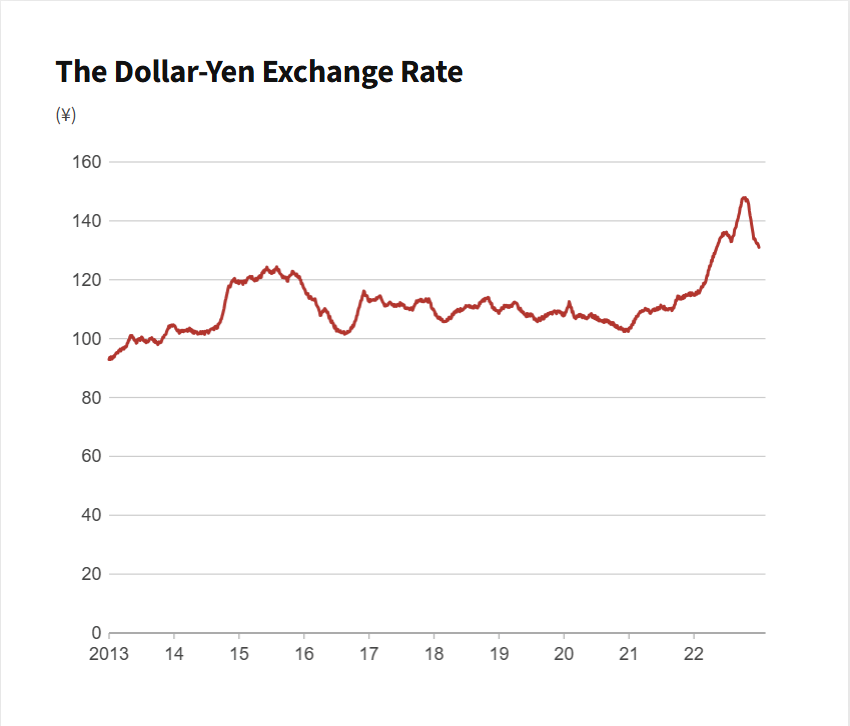

Before the bond market crisis, it was very popular for Japanese Investors to borrow low-yielding Yen and use it to fund higher-yielding foreign assets. However, now that domestic yield rates in Japan have increased, there are no incentives for investors to pay an exchange rate to convert Yen into Dollars to buy foreign assets.

With the rise in domestic interest rates, major waves of Japanese investor repatriation occurred. Historically, Japan has been one of the largest buyers of US financial assets, with over $1.1 trillion in US debt. As a result, a spillover effect was observed, with US and European treasury gilt demand decreasing, thereby inducing higher borrowing costs for other countries.

With Takaichi’s Liberal Democratic Party achieving a sweeping victory in the snap election last month, many wondered about the fiscal policy her government would adopt. What followed was the appointment of Ayano Sato and Toichiro Asada, who both favour low interest rates and a dovish outlook. This pathway Takaichi seems to be taking could imply investors might start asking for a higher risk premium, especially with the current lack of a medium-term consolidation roadmap.

Japan’s role in the world economy clearly has changed. From being the world’s “shock absorber” and funding hub, the JBMC has painted Japan in a new light. The more dovish outlook Tokyo is taking has shifted its position from the low-yield anchor supporter of the carry trade to possibly being treated similarly to other high-debt issuers such as Greece and Italy. This crisis has also emphasised the heightened emotions investors have shown towards loose fiscal plans, which may cause global yields to spike.