.png)

• New Sanctions: The US imposed fresh restrictions on Russia’s largest oil producers.

• Price Pressure: Crude prices remain under pressure as global supply continues to outweigh demand.

• Storage Risk: Future oil storage capacity may become a concern if oversupply persists.

The global commodities market is shifting fast, and crude oil is at the centre of it. The US has introduced new sanctions on Rosneft and Lukoil, Russia’s two largest oil companies, as part of its attempt to push Vladimir Putin toward a negotiated settlement in Ukraine. These measures go far beyond diplomacy. They threaten to reshape how oil moves across borders, how prices behave, and how stable energy supplies remain.

Although the sanctions were designed to influence Russia’s actions in the war, their effects will not stay contained within that conflict. Any disruption to Russian supply has the potential to ripple across global markets, raising fuel costs, altering trade routes, and increasing the pressure on countries that rely heavily on imported energy.

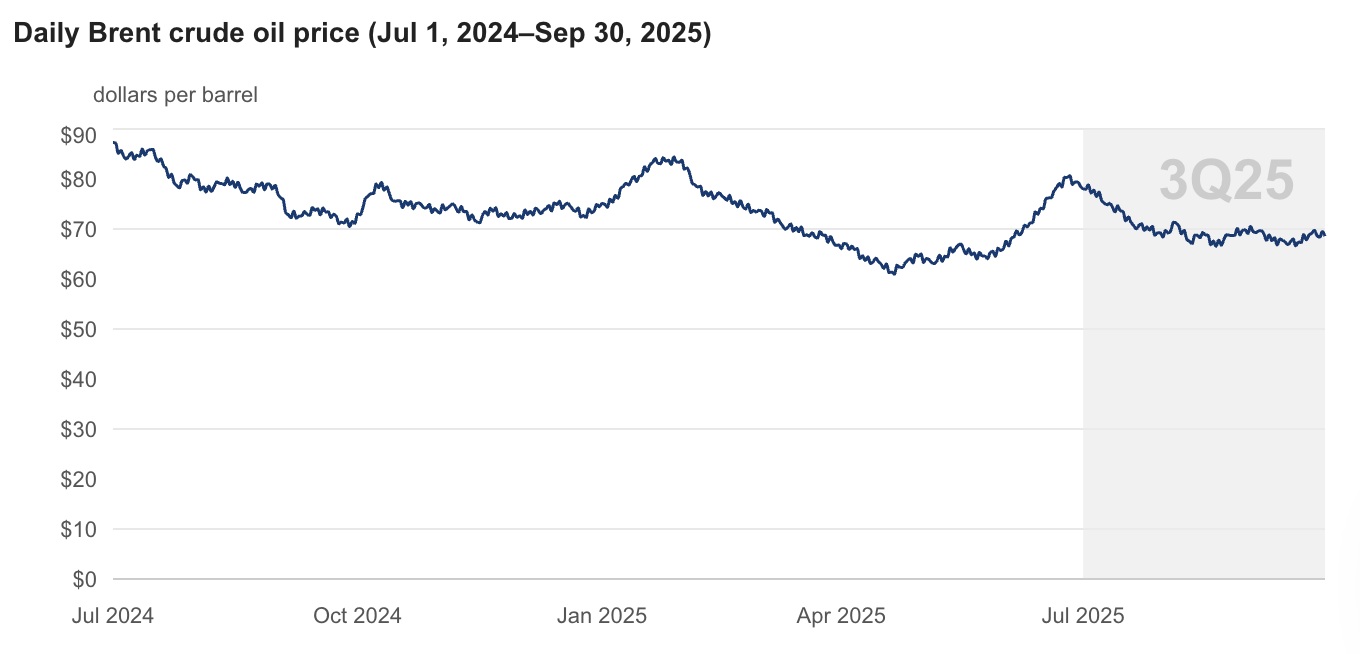

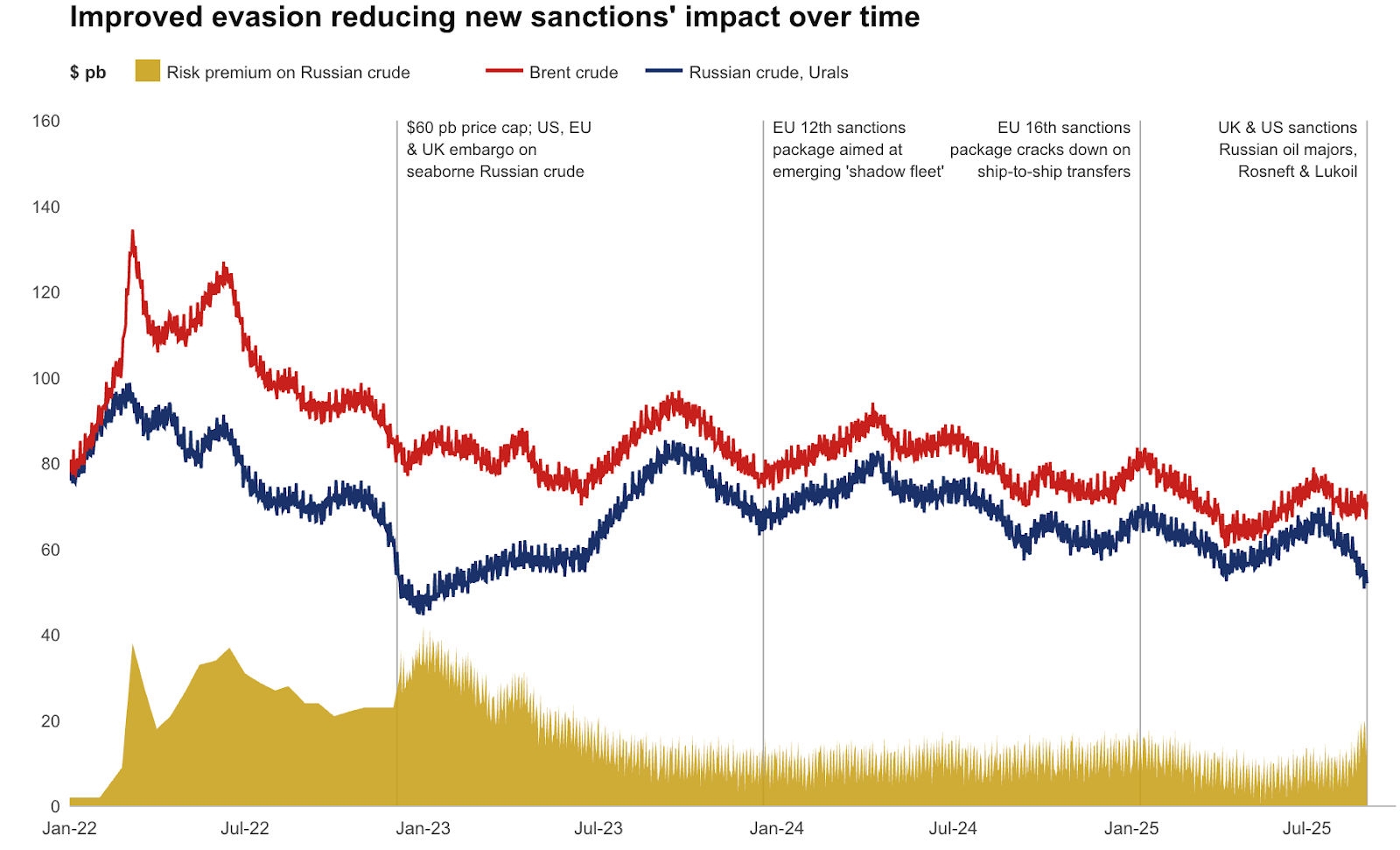

The two largest Russian oil producers, Rosneft and Lukoil, recently got hit with fresh US sanctions. Together, these two producers export about 3 million barrels of oil per day. For context, these two firms account for roughly 3% of global oil production. The most recent sanctions on Russian oil, particularly those targeting major oil producers in 2025, have had a diminishing impact on global oil prices. Despite the initial shock to markets when sanctions were first imposed in 2022, with Brent crude spiking above $120 per barrel, the market has since calmed. By mid-2023, prices began to stabilise around $80–90 per barrel, reflecting how the global oil trade adjusted to Russia's increased evasion tactics, including ship-to-ship transfers in international waters, hiding vessel locations by switching off transponders, and selling oil through intermediaries to disguise its true origin. The gap between Brent crude and Russian crude narrowed as sanctions became less effective at driving prices higher. Even with the latest restrictions on Russian oil exports, Brent prices have remained relatively flat, hovering around $70–80 per barrel from mid-2023 to late-2024.

This trend suggests that while sanctions still play a role in the market, their ability to disrupt global prices has weakened over time as supply chains and trade routes have evolved to avoid the restrictions. But why have these sanctions not caused oil prices to skyrocket? To compensate for the loss of Russian crude supply, it is expected that other OPEC+ producers, such as Saudi Arabia, will step up to plug the supply gap. However, this is not the only way the supply shortfall is being addressed. Some buyers of Russian crude are also granted exemptions through special licences. Trade networks often get reorganised in the aftermath of sanctions. It is very likely that some of the Russian crude supply will flow via non-sanctioned companies, for example refiners in countries such as India, which continue to process Russian oil, allowing the global flow of Russian crude to continue.

What is expected to happen to the price and supply of crude oil? According to Reuters, there are worries regarding the oversupply of crude, which is why prices are likely to remain under pressure. The main cause of this oversupply is the significant expansion of supply by OPEC+. The oversupply of crude oil will lead to supply outweighing demand in the market, assuming demand does not rise at the same pace, which subsequently leads to a decrease in price.

The World Bank suggests global oil demand growth is running at only about 0.7 million barrels per day, well below pre-pandemic averages of around 1.0 million. Volatility is likely to remain elevated due to ongoing geopolitical tensions and key drivers such as OPEC+ production decisions, conflicts in the Middle East, and fluctuations in global demand. While this volatility can create uncertainty, it is not necessarily negative, as financial institutions often use price swings to hedge risk and generate profit.

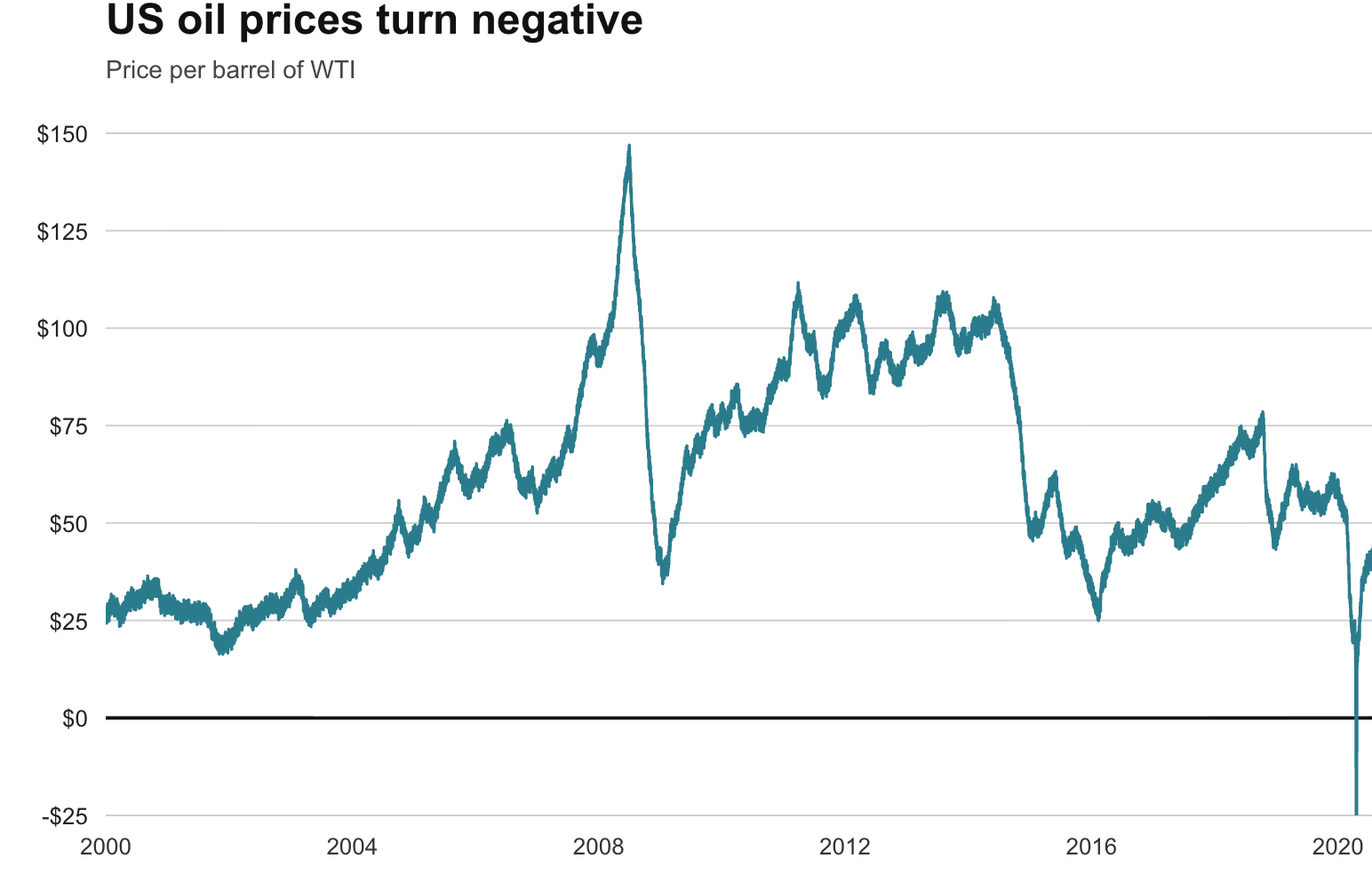

An issue often overlooked in the oil market is storage capacity. In 2020, crude oil prices famously dropped below $0 for the first time, largely because there was not enough storage available to hold the excess supply at a time when demand collapsed due to COVID-19. Looking ahead, demand growth is slowing. A slowing Chinese economy, weak industrial output in Europe, and more efficient use of electricity, such as electric cars, are all contributing to reduced consumption of oil. This would put renewed downward pressure on oil prices.

Given the wide range of factors acting on crude oil markets, volatility is likely to stay elevated in the near term. Geopolitical tensions continue to build, yet the market has become noticeably more resilient to sanctions and supply shocks. At the same time, non-OPEC+ producers, particularly the United States, Brazil, and Canada, are increasing production at a rapid pace, putting additional downward pressure on prices. Added to this is the ongoing transition toward cleaner energy, which is slowly eroding longer-term demand.

Collectively, these factors point toward a gradual but sustained softening in crude prices over the coming years. Ultimately, the future path of the oil market will be shaped by the tug-of-war between rising supply, geopolitical uncertainty, and the accelerating global move toward lower carbon energy.