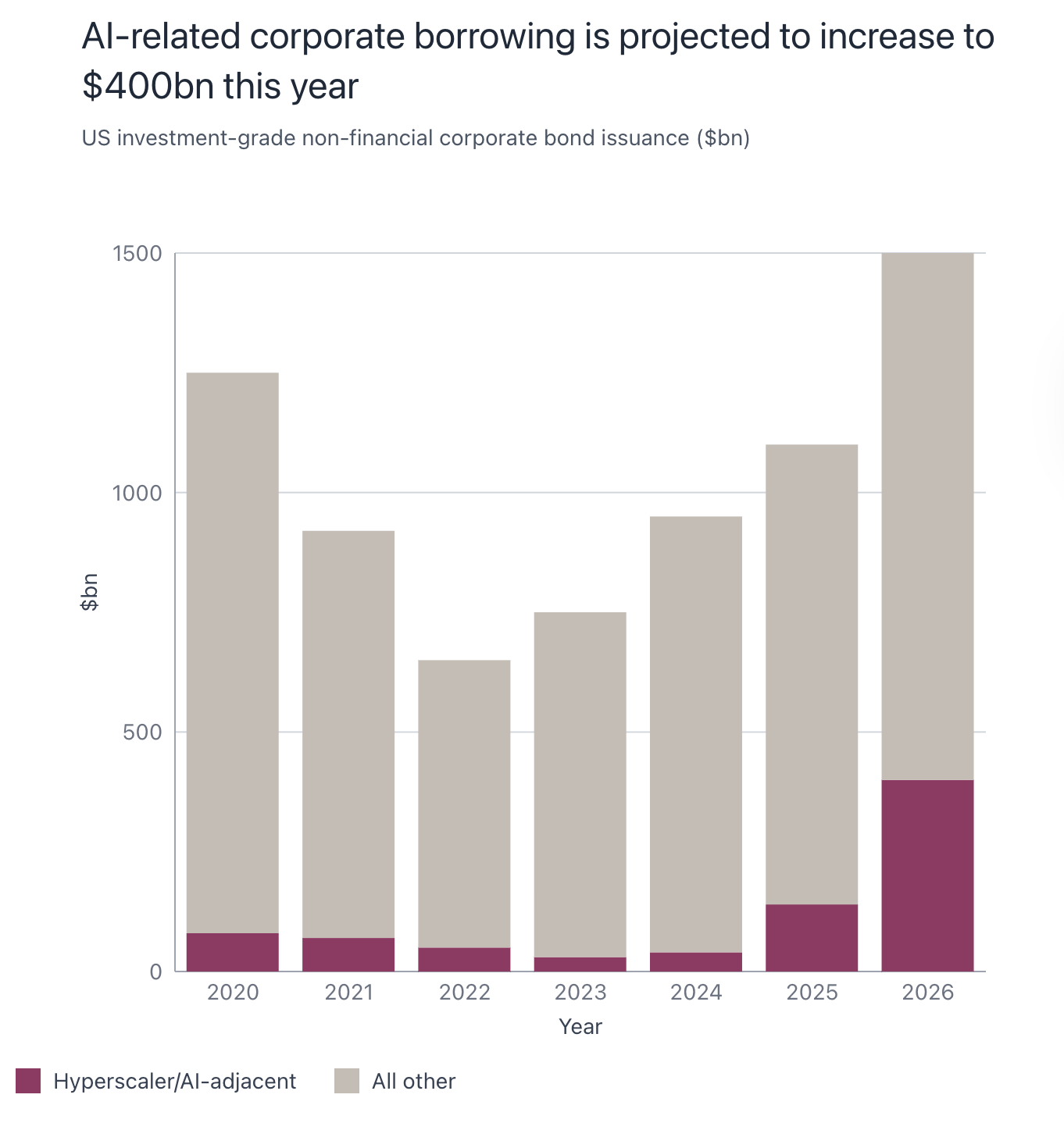

Until now, major borrowers in the US investment-grade corporate bond market have been mostly large banks and telecom firms, meaning creditor investors are largely insulated from shocks in the tech-dominated equity market. However, a notable change in the industry is taking place now. According to Apollo Global Management, by 2030, half of the 10 largest borrowers in this market will be hyperscalers, including Microsoft and Meta, who are building data centres to train and run their latest models. Evidently, credit markets are expected to play a key role in the development of AI assets, through enabling access to larger capital with the benefit of lower, fixed interest payments without restrictive covenants. The graph below (Figure 1) from Morgan Stanley estimates indicates there is a rapid increase in borrowing via fixed-income debt to finance this AI spending. In fact, looking more closely at the diagram, Morgan Stanley estimates that hyperscalers and their adjacent companies will raise $400bn from the US high-grade market this year - a sharp increase from the $170bn raised last year and $44bn in 2024.

Moreover, JPMorgan says the AI and data centre (hyperscaler) related sector now makes up 14.5% of the bank’s US Liquid Index (a benchmark for the nearly $10tn US investment-grade bond market) bigger than the share accounted for by banks. This suggests that we are in the midst of a structural shift in capital raising where fixed-income debt is playing an increasingly critical role in allowing for technological progress to take place. Alas, this surge in AI-related bond issuance has already raised borrowing costs for these firms. Oracle’s credit spread (the premium investors demand to hold its bonds over safe haven assets like US Treasuries) jumped more than 0.75% after it borrowed $18bn from the bond market last September, from S&P Global data. This reiterates investors’ growing concern over runaway capital expenditure on AI and the returns it generates, with the market moving away from blindly funding AI growth to demanding proof of financial returns, leading to higher yields.

Whilst in the short-term this isn’t an issue for hyperscalers’ credit rating due to robust cash flows and strong balance sheet, the inability to convert capital to commercial returns may undermine stock valuations, with optimism challenged by present-day reality.

Whilst borrowing from public markets via bond issuance is one source of income, private credit also makes a strong case for itself. Its growth is primarily driven by hyperscalers’ needs for bespoke financing arrangements for vast infrastructure investment. This is because flexibility in funding solutions is especially valuable for capex-intensive sectors due to their insatiable need for funding. Quantitatively, S&P estimates that spending on global AI information technology will grow between 28% - 36% annually over the next 5 years highlighting the crucial role credit plays in providing firms the opportunity to exploit the current tech trend. Earlier in 2025, Meta raised nearly $60bn to support its data centre build-out through a joint-venture between Meta’s affiliate and a private lender to create a tailor-made solution to support the project’s construction, alongside issuance of its AA- public bonds. Importantly, this indicates the necessity of broadening a firm’s funding base, by not only leveraging its strong credit rating in the public markets, but using private debt to create favourable, bespoke solutions for itself.

However, it is also important to analyse the broader relationship between these two funding mechanisms in the credit landscape, and its implications for investors. The private market is still populated by companies with sub-investment grade ratings, resulting in these firms having inadequate access to more traditional sources of credit through public bonds issuances. As a result, private credit absorbs much of the higher-risk demand, leaving ample investment-grade supply available for traditional credit investors. Therefore, within the wider finance ecosystem, private credit markets complement, rather than displace investment-grade lending available to traditional investors. By absorbing sub-investment-grade borrowing demand, private credit helps preserve depth and liquidity in public investment-grade bond markets through greater liquidity in public debt markets. This supports greater, more efficient price discovery and tighter credit spreads, thus allowing hyperscalers, such as Meta, to fundraise large capital expenditure projects at attractive terms.

With this being said, the growth of private credit can reduce transparency for public bond investors, as private loans involve less disclosure and can make it harder to assess a company’s true leverage and risk profile. In addition, more complex and bespoke private credit structures may complicate credit analysis and, in some cases, place pressure on credit ratings.These private-market risks can spill over into public markets by making it harder for investors to accurately assess a firm’s overall debt position, particularly when private borrowings are not fully visible or are structured off balance sheet. For firms, this may lead to higher funding costs or tighter credit ratings, while for investors it increases uncertainty, potentially widening credit spreads and reducing confidence in public bond valuations.

While the growth of private credit introduces some risks for public bond investors - particularly around transparency and complexity - these concerns appear manageable. The largest borrowers, including hyperscalers, maintain high-quality credit ratings , and public investment-grade fundamentals are broadly sound. Consequently, rather than crowding out public markets, the expansion of private credit reflects a diversification of funding sources, helping to spread the cost and risk of large-scale investment, as seen with Meta’s $60bn fundraising deal. As a result, the public investment-grade bond market remains well supplied and liquid, supporting efficient trading and reinforcing its resilience as the broader credit landscape evolves to provide solutions for tech companies to fund long-term growth initiatives.

A third way to raise capital is through structured financing, where loans or other receivables are pooled together and then categorised into different levels of risk for bond investors. Although traditional funding sources such as bank loans, private debt, and corporate bond issuances remain viable options, firms are turning to alternative fundraising strategies with greater frequency. In particular, securitisation transactions, including asset-backed securities (ABS), have become an attractive financing tool as they offer advantages like reduced refinancing risk, lower borrowing costs, and enhanced financial flexibility. ABS can also be issued to securitise the future cash flows from unsecured borrowings, such as student loans, credit card debt, or lease obligations. In the case of data centres, ABS are collateralised by tenants’ future lease payments and by the owner’s equity interest in the data centre. Together, this provides investors with reassurance that should the tenant default on payments, the underlying data centre asset has value that can be used to recover losses, making ABS more secure.

As a case study, Meta’s Hyperion data centre is being financed through Beignet, the name of a $30 billion deal to engineer the construction of a Meta data center in Louisiana. From a creditworthiness perspective, investors aren’t worried about this massive spending commitment given the very profitable existing lines of business these blue-chip companies operate in. Despite this, the nature of ABS means that the $30bn debt is not on Meta’s balance sheet. Instead it’s payable by a separate entity - a special purpose vehicle (SPV) set up for the deal - which will pay back the loan from its long-term lease with Meta.

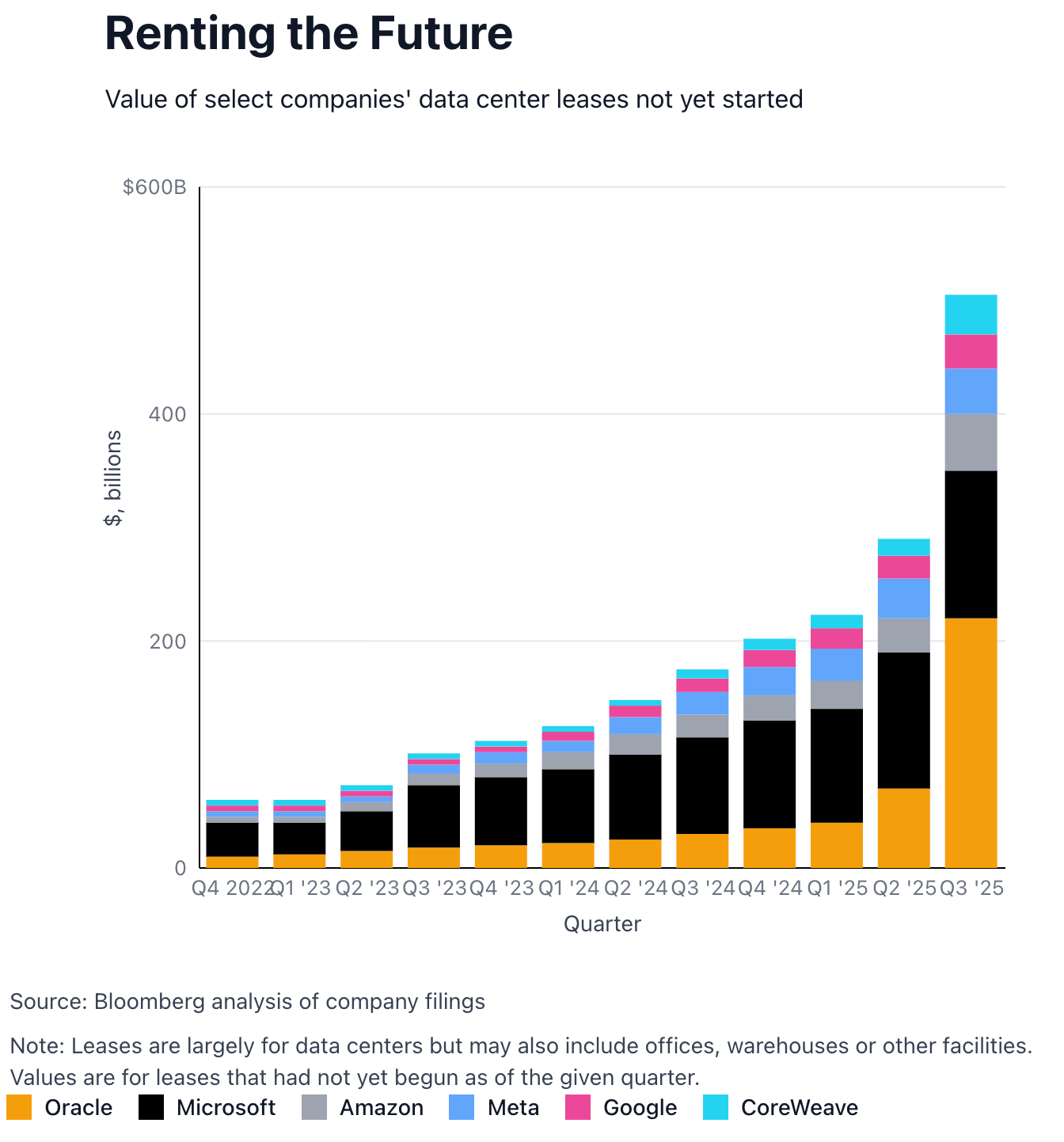

The Figure 2 chart shows that large tech firms, led by Oracle, Microsoft and Amazon, are committing to rapidly growing amounts of future data-centre leases, highlighting both strong expected demand for computing capacity and increasing long-term financial obligations. Despite healthy credit ratings, there are still some concerns, such as renewal risk. Large data-centre financings rely on long-term leases to match debt maturities, but if tenants leave and there is an oversupply of data centres, landlords may struggle to replace them, increasing lease renewal risk for lenders, leading to loan repayment issues. Secondly, another key issue is counterparty risk, which is particularly a large issue as lenders may be overexposed to just a handful of companies. This is already an issue with Oracle, after the company backed tens of billions of dollars of project finance loans with leases. However, portfolio managers typically want only so many of their investments to be with a single business or sector, resulting in concentration risk becoming a serious threat to the alternative financing space. Focusing more on Oracle, the firm is considered riskier compared to other hyperscalers, as it is more indebted relative to its earnings, hence it is rated only two steps above junk status, yet it’s investing so much in AI that it’s burning cash. Consequently, the cost and volume of traded insurance contracts (credit default swaps) against its debt spiked at the end of last year, as banks and other investors hedged their exposure. Taken together, these dynamics suggest that although alternative financing has supported the rapid expansion of data-centre infrastructure, its growing dependence on a concentrated group of leveraged hyperscalers could amplify downside risks if growth expectations falter or market conditions tighten.

The rapid expansion of AI infrastructure is reshaping not only the technology sector, but also the global credit landscape that finances it. This form of financing is especially important given projections that global AI-driven data-centre capital expenditures between 2025 and 2030 could reach between $3.7tn and $7.9tn. As Matt MacQueen, Global Head of FICC Micro Products at Bank of America observes “The numbers [level of funding required] are like nothing any of us who have been in this business for 25 years have seen”. This is because the scale of funding required is unprecedented, forcing market participants to “turn over all avenues” to support this infrastructure build out. Public bonds, private credit and structured finance have therefore become complementary tools in enabling hyperscalers to meet extraordinary capital demands. However, as reliance on these funding mechanisms grows, so too do risks related to leverage, transparency and concentration. Ultimately, while innovative financing structures are essential to sustaining the AI growth narrative, their long-term success will depend on whether hyperscalers can convert vast capital investment into durable, long-term cash flows, justifying both investor confidence and the expanding role of credit markets in funding the next phase of technological progress.