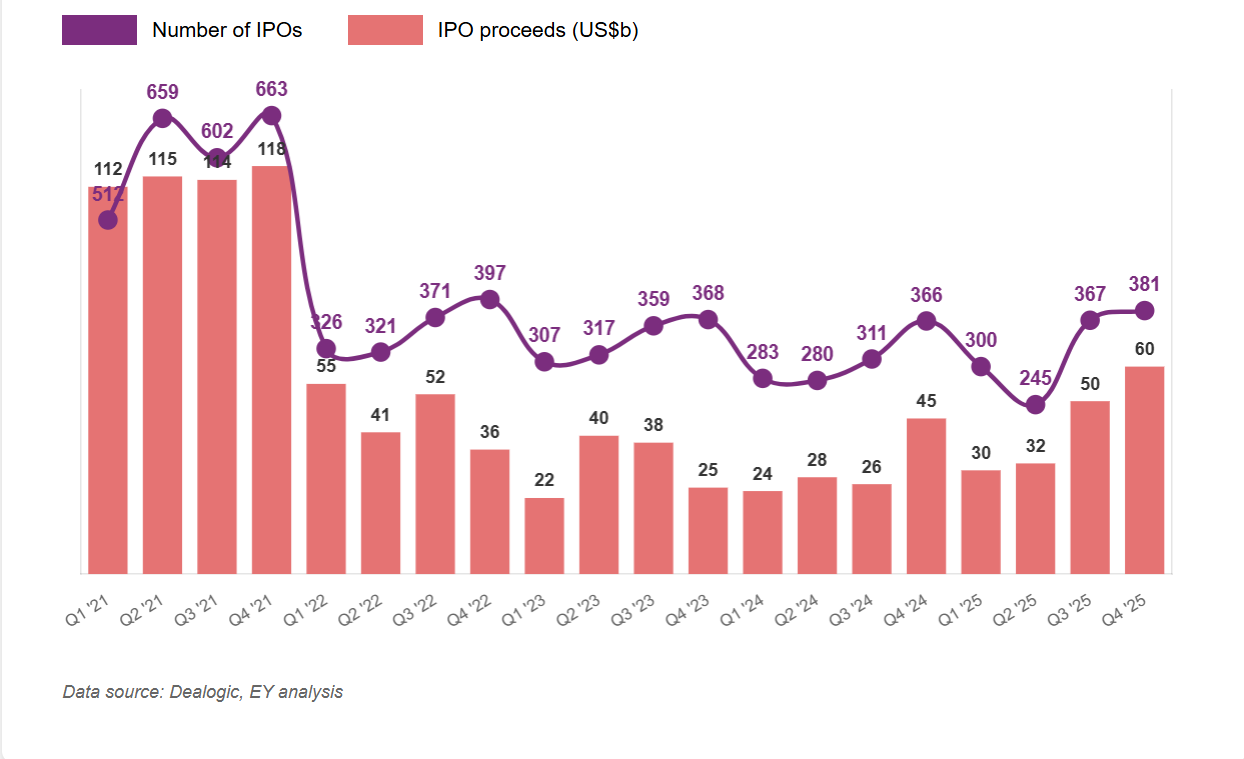

The Hong Kong stock market’s top index, the HSI, rose 27.8% in 2025, outpacing the US, UK, and Japan. What stood out the most, however, was the surge in IPO activity on the Hong Kong Stock Exchange (HKEX). Ranked as the top global IPO venue, it facilitated a total of 119 companies, raising US$37.22 billion in 2025, a 229% increase from US$11.3 billion in 2024. The rise in IPO fundraising symbolised the underlying valuation normalisation, targeted policy easing, and revival in Southbound liquidity. However, while headline activity suggests renewed confidence, the sustainability of this recovery over the next 12 months remains conditional rather than assured. It is challenging to provide a definitive conclusion largely due to the market’s vulnerability to external macro and geopolitical shocks, risking the deterioration of capital discipline. Nevertheless, valuations continue to trail historical norms, along with sustained elevations in IPO breaks, contributing to the general optimistic outlook.

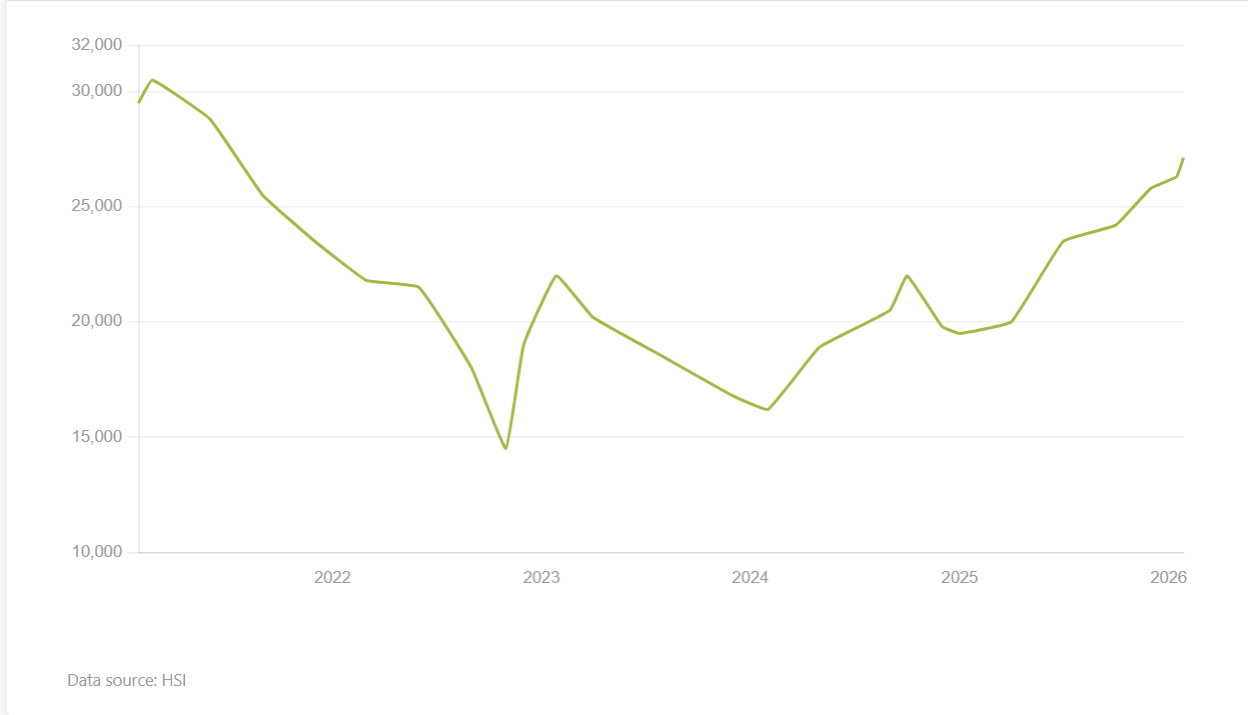

Referencing Figure 1, the scale of Hong Kong’s drawdown over the last cycle was severe in both magnitude and duration. Between 2021 and early 2024, the HSI fell by approximately 40%, with the tech sector taking an even greater hit (67%), one of the worst performances among major global equity benchmarks. The significance of the decline was echoed in the sharp fall in valuation multiples: the average forward P/E ratio fell from 16x to near 10x at the trough, reflecting earnings downgrades and an expanding risk premium.

This collapse was driven by a confluence of shocks. The 2020-21 regulatory reset in China, particularly targeting tech, tutoring, and property markets, fundamentally altered investor perceptions of policy predictability. A simultaneous property-sector crisis also eroded household wealth and undermined financial stability. Hence, when the risks of US-China decoupling and economic sanctions became increasingly pronounced, capital outflows accelerated to drain liquidity from Hong Kong equity markets. The result was a forced valuation reset that, while painful, laid the groundwork for the current opportunity set.

The recovery gained traction following a series of incremental but targeted policy measures, culminating in the September 2024 stimulus package. The PBOC cut rates, lowered home-loan down payments, and established a CNY 500 billion swap line to encourage liquidity injections into equity markets. On the fiscal side, Beijing signalled increased local government bond issuance, the swap of off-balance-sheet debt, and the use of special bonds to purchase unsold housing. These measures spurred a sharp equity rally: the Hang Seng jumped 37% from Sept 11 (16,964) to Oct 7 (23,241).

Hong Kong instead pursued specialised structural reforms in its capital markets with a clear objective of incentivising IPO fundraising. These included the expansion of the Technology Enterprises Channel (TECH), refinements to IPO pricing and allocation mechanisms, and broader use of confidential filings to reduce execution risk for issuers. Hence, the increased market activity has been a reflection of the improved process efficiency and pipeline visibility. What remains policy-dependent is the durability of Mainland support, particularly whether regulatory tolerance and capital channel openness persist through potential future downturns.

From the perspective of equity valuation, Hong Kong still offers an attractive forward multiple at a discount to its long-term average, and at levels much below US and Indian equities. As the 5th largest stock exchange globally, Hong Kong is home to an abundance of large-cap, liquid equities supported by strong mainland capital inflows. Hence, even though one might cite inflated risk premia in geopolitical contexts, the valuations remain favourable for continued buying activity.

Sector dispersion, however, is equally pronounced. Financials and utilities trader nearer to historical averages, whereas consumer discretionary and internal platforms present an embedded policy risk discount. New-economy IPOs in AI and biotech are nevertheless priced at premiums to the broader market while remaining cheaper than their US-listed peers. This uncovers the reality of continued uncertainty rather than a full normalisation in risk and confidence.

Liquidity has been the most tangible driver of the rebound. Southbound Stock Connect flows now regularly exceed HK$200 billion in daily turnover, representing a material share of Hong Kong’s free-float market capitalisation. Mainland institutional investors have become marginal price-setters in several large-cap names, reversing the outflow dynamics of 2022–23.

In the IPO market, metrics are more mixed. Subscription rates have rebounded sharply, and average first-day returns in 2025 rose into the high-30% range following pricing reforms. However, IPO break rates remain close to 40%, a level historically associated with weaker aftermarket confidence. Importantly, both the SFC and HKEX have issued guidance letters warning sponsors and issuers against aggressive forecasting and low-quality listings—an explicit signal that headline liquidity is not synonymous with healthy market depth.

There is credible evidence of capital rotation from property into equities, particularly among Mainland and Hong Kong family offices. Transaction data and bank disclosures suggest reduced incremental property allocation alongside rising equity trading activity. Beneficiaries of this rotation have been technology hardware, consumer brands, and dividend-yielding financials (CNOOC, China Mobile…). The transition away from tech bids through 2025 has allowed sectors tied to consumption and dividends to deliver cyclical outperformance. On the other hand, new tech and biotech issues (AI chipmakers, genomics) have been market darlings: several early 2026 IPOs (Biren Tech, MiniMax, Zhipu AI) rocketed on debut. Whether this flow-driven rotation persists depends on central policies. For now, tech/AI segments and recovery-themed consumer plays lead inflows, while defensive sectors get less attention.

Hong Kong’s booming IPO market, therefore, reflects investor confidence rather than creating it. After 2020–21’s drought, 2025 saw a resurgence: KPMG reports 316 active IPO applications as of Dec 7, 2025 (39% in TMT, 21% healthcare), and notes “a steady influx of tech and biotech firms opting to list in Hong Kong” drawn by supportive policy. Furthermore, it is confident of the 2026 IPO outlook, referring to Chinese tech companies scheduled to release in Q1. Indeed, HKD4.2 billion had already been raised in Jan 2026, with deals generating over HKD10 billion individually (Muyuan) to come in Feb and beyond. Wider market sentiment resonates with optimism, projecting a total fundraising that exceeds the 2025 amount. PwC further states that the overall trend of falling interest rates will boost investor confidence. This will be complemented by favourable government policies, making Hong Kong’s IPO market likely to continue its robust performance. At the same time, the market discusses potential reforms such as further reviews on the regimes for dual primary and secondary listings, deepening collaboration between HKEX and Southeast Asian exchanges, and establishing more targeted pathways to facilitate overseas companies seeking a Hong Kong listing.

The Hong Kong stock market is fundamentally constructive and complex. Policy “tailwinds” have returned, yet have not fully de-risked the space. Similarly, the trend of IPO activity is well evidenced to continue into 2026, especially if regulatory innovation and Southbound liquidity continue to ease the fundraising process. Still, the geopolitics and China-linked macro factors serve as decisive catalysts for Hong Kong markets, positing a constant consideration towards underlying uncertainties.