• Inflation Expectations: Shifts in expected inflation influence when consumers choose to spend, motivating them to delay purchases in hopes of maximising income value during periods of lower inflation.

• Cost-of-Living Pressure: Rising unemployment, higher household bills, and growing media scrutiny are amplifying anxiety about the UK’s economic outlook and reinforcing precautionary saving.

• Sector-Specific Strain: Inflation does not impact all industries equally, with energy-intensive and low-margin sectors such as food manufacturing facing heightened pressure from the post-2023 energy crisis, COVID-19 effects, and recent minimum wage increases.

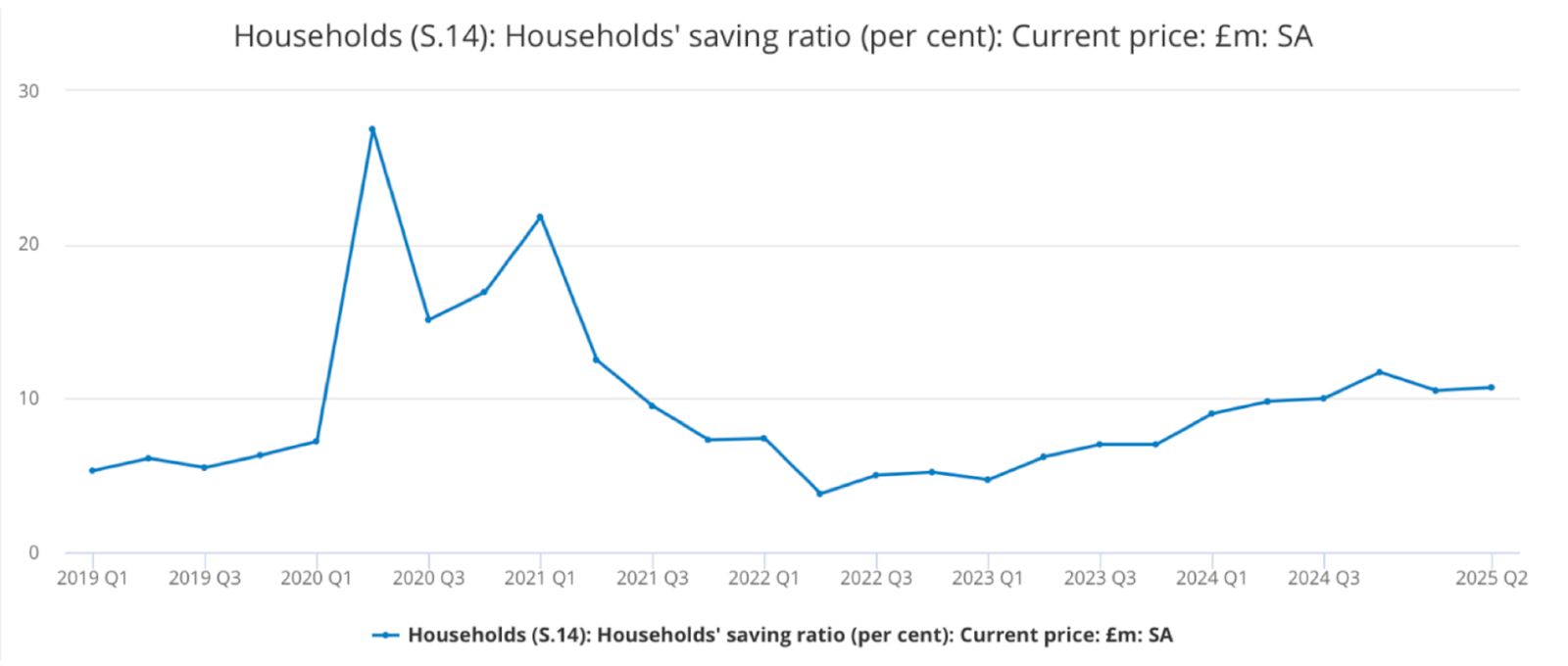

Over the past decade there has been a significant shift in consumer saving habits. The changes in household savings ratios before and after COVID-19 are notable. This has led to industries associated with non essential spending, such as hospitality, travel, and leisure, facing a sharp decline as essential spending on food, energy, and housing has been prioritised. With saving ratios ranging from 5.3 percent in 2019 Q1 to a peak of 27.5 percent in 2020 Q2 and 10.7 percent in 2025 Q2, the question arises as to what underlines these major shifts in consumption behaviour in the UK (Office for National Statistics).

This article explores three main concepts that could explain the changing behaviour of consumers, including inflation expectations, rising concerns about the cost of living and production cost changes across several industries following the 2023 energy crisis.

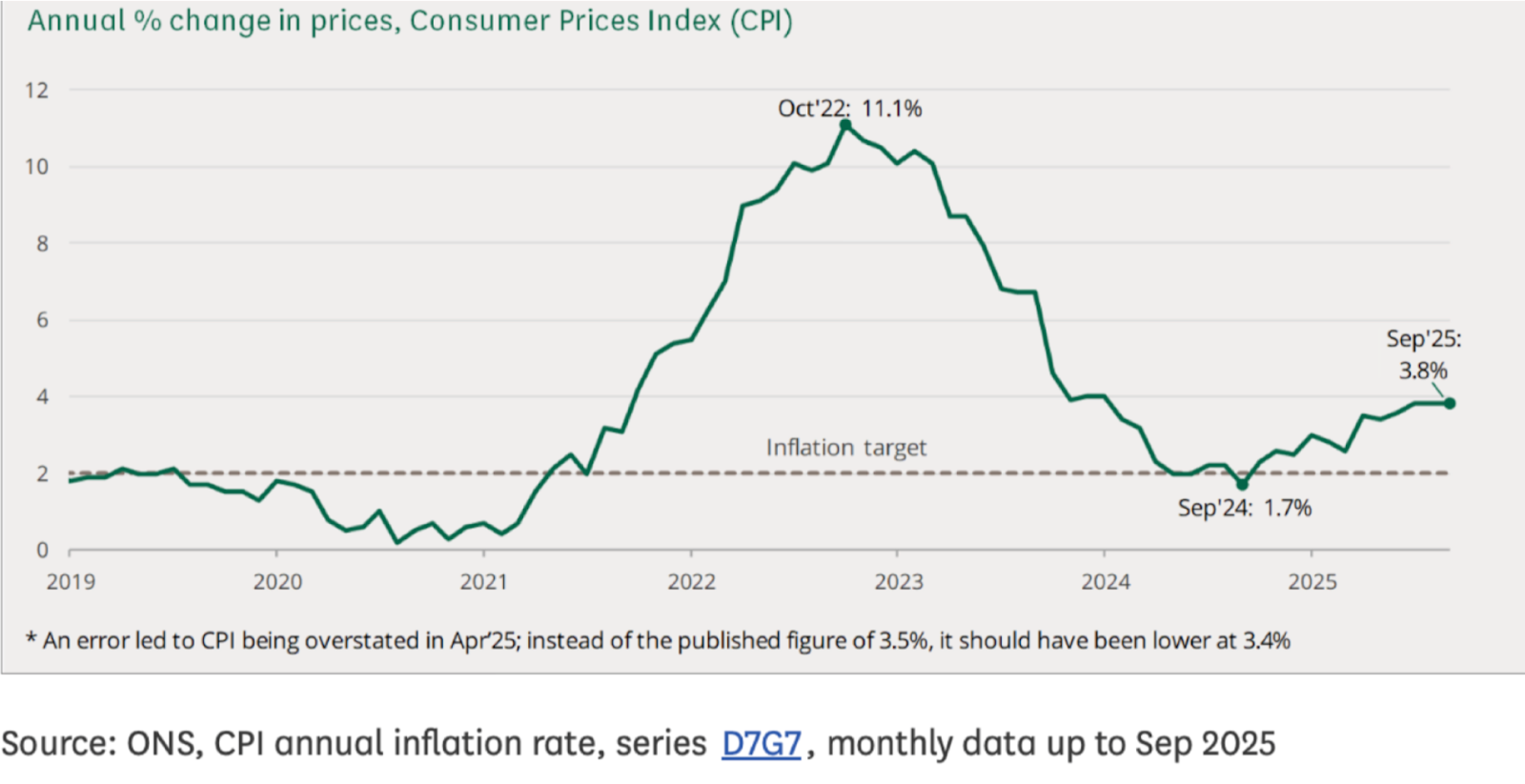

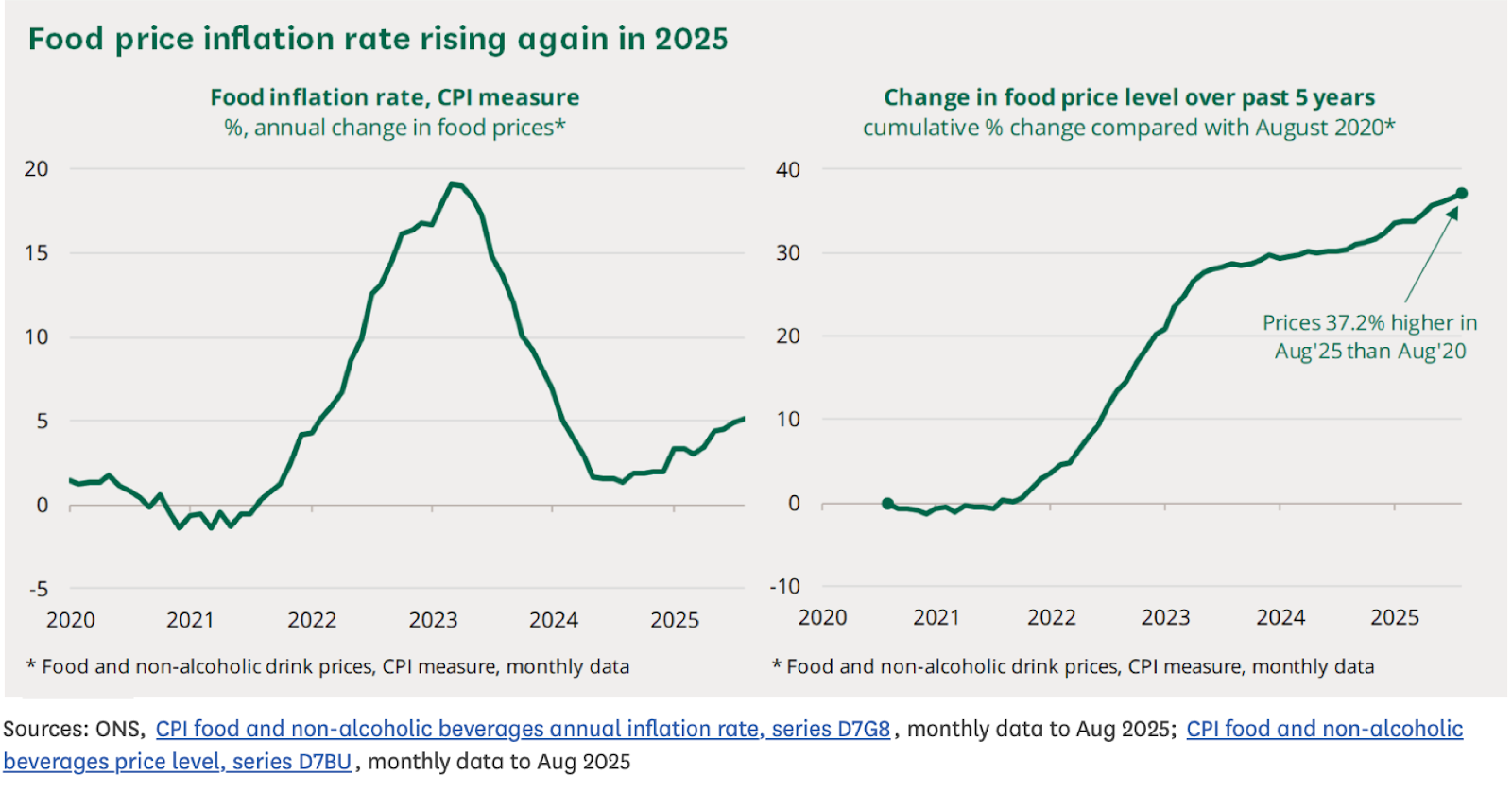

One reason for the shift in the saving behaviour of households can be linked to the rise in inflation rates over the past year. As of September 2025 the inflation rate was reported as 3.8%, as opposed to the target rate of 2% (Bank of England). This rate has been calculated using the Consumer Price Index measure, which approximates the change in cost of living standards using a representative basket of goods and services bought by households.

One possible reason for a higher post COVID saving ratio, in comparison to before, could be that consumers are delaying their consumption in anticipation of a period of lower inflation. Lower inflation rates allow the same basket of goods purchased now to cost less for the consumer and increase the value of their income in real terms. This theory of utility maximisation helps explain why the saving ratio is on the rise as inflation increases, since consumers are often motivated by self interest and reaching the highest utility associated with their income.

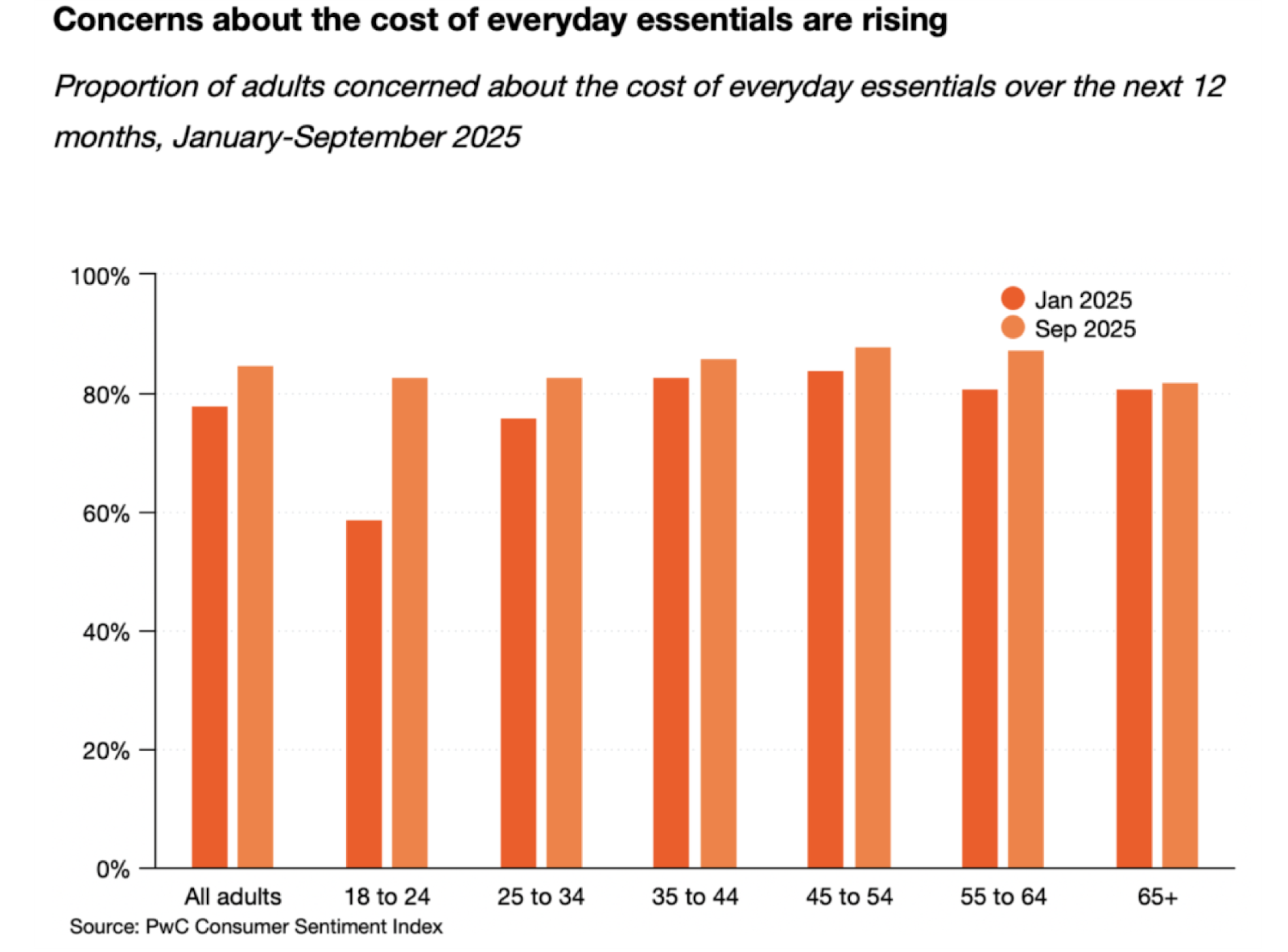

Alongside the uncertainty of inflation rates, concerns about the cost of living and everyday household essentials are significantly on the rise. This is exemplified by a hike in average annual bills for gas and electricity consumption of 42% in 2025 compared to winter 2021 to 2022 (House of Commons Library). This added pressure on UK households helps explain the shift in consumer behaviour and the trend of reduced consumption.

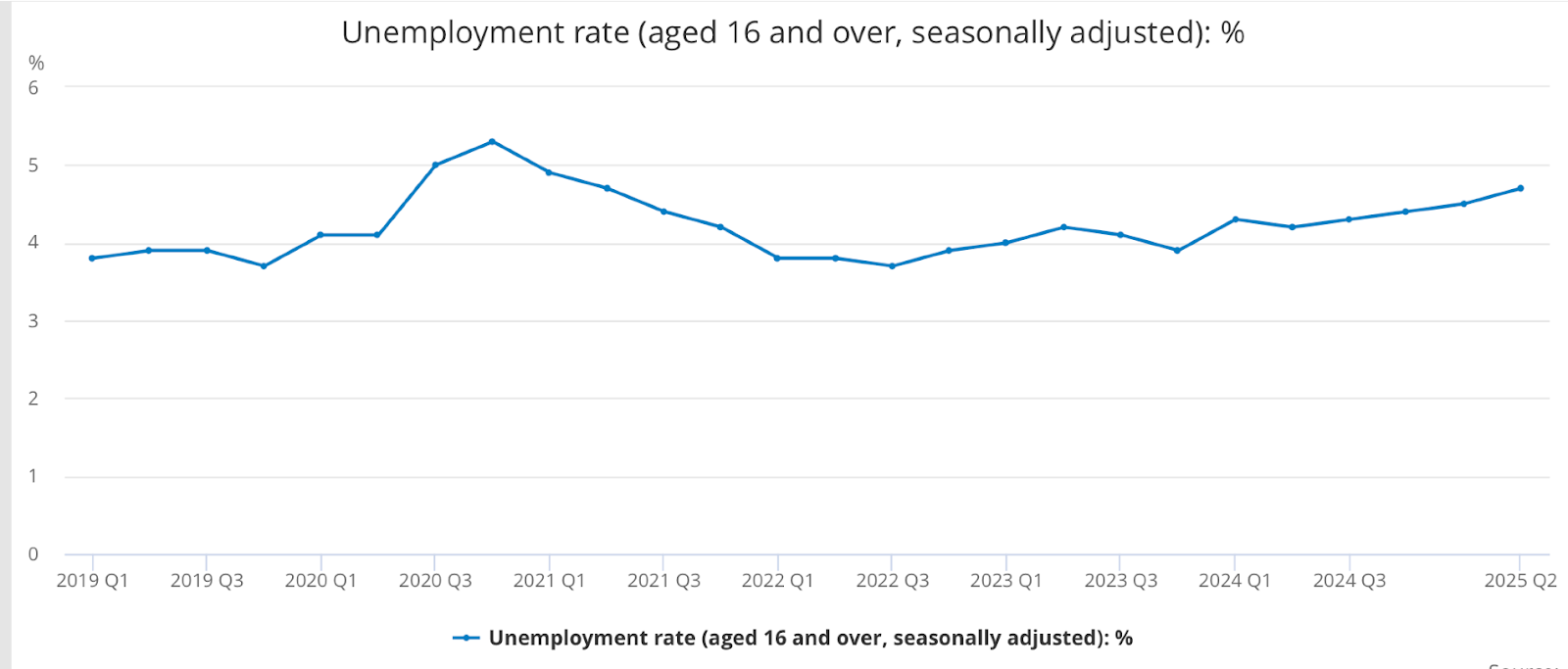

Additionally, other factors that could contribute to this concern about the cost of living may include the rise in unemployment from 4.2% in 2024 Q2 to 4.7% in 2025 Q2 seen above. This could reflect uncertainty in the job prospects and labour market, and this lack of stability also contributes to the concerns of households, who may prepare for the future by saving more of their income.

This links to the consumption smoothing concept identified by economists, which claims that consumers often prefer to maintain a consistent standard of living across their lifetime as opposed to fluctuating spending behaviour. Thus, saving for uncertain times ahead is likely to be a strategic choice for individuals to maintain their current quality of life and living standards.

However, it is important to recognise that while the rise in the cost of living and unemployment are undoubtedly key factors in the anxiety of UK consumers, it is likely that media coverage also plays a role. After all, with the increase in downloads of social media platforms such as TikTok and Instagram surging to a record high during COVID-19, reports of rising prices, redundancies, and financial strains have been amplified.

This heightened anxiety may have contributed to a form of ‘herd behaviour’ where households imitate the consumption patterns of others as panic about the market spreads. As online platforms continue to highlight concerns about the economy, individuals are likely to cut back on spending accordingly.

With the increase in gas, electricity, and energy costs compared to pre-COVID levels, consumers are not the only ones struggling to keep up. Energy-intensive industries and businesses with tight margins have also been finding it difficult to compete with high operating costs and input prices. For example, the food manufacturing industry in particular has seen significant rises in prices for consumers. This can be explained by two major policy changes, which include the rise in national insurance contributions and the minimum wage (Economics Observatory).

As the farming industry often relies on manual labour, the rise in minimum wage to £12.21 (by 6.7%) in 2025 means that labour costs within this sector have been significantly affected, with production costs rising considerably (UK Government). Due to this rise in operating costs and the added pressure of small profit margins within the food industry, these additional costs are often passed on to consumers to maintain the required margin for the business model to continue.

Thus, with the rise in minimum wage, while the income of many minimum wage workers may have increased in nominal terms, their spending capacity may not have increased proportionally due to the coupled rise in food prices. This means that, in real terms, individuals are unable to consume additional goods since their income holds less value with the inflation of prices. This may cause a rise in precautionary savings among consumers.

Following COVID-19 and the major energy crisis of 2023, it is evident that the UK economy is in a period of transition. With unstable inflation rates, a rise in unemployment, and growing domestic household bills, consumers are in a period of uncertainty as the market adjusts to the lasting effects of these economic fluctuations. Thus, increasing savings and reduced consumption may be a form of precaution for consumers.

As the economy stabilises, it remains to be seen whether savings patterns will return to pre-pandemic norms. With anticipation surrounding the upcoming release of the UK budget on the 26th of November 2025, consumer spending is likely to be restrained in the weeks leading up to the announcement. This may be the beginning of a rebound in consumer spending if the budget is successful at restoring UK consumer confidence through reassurance, grants, and employment incentives. If, on the other hand, the budget reintroduces consumer anxiety by cutting public services, increasing job insecurity, or raising taxes, consumer confidence and spending are likely to deteriorate. Hence, as we approach the first quarter of 2026, it is clear that the upcoming budget will play a significant role in steering the direction of consumer spending.