.jpeg)

Building on the funding landscape and the emerging strengths of Saudi Arabia’s clinical trial ecosystem from my first article, this part examines how these strategic advantages translate into long-term competitiveness within the global biotechnology sector. As the Kingdom expands its research capacity, deepens international partnerships, and aligns regulatory frameworks with leading global standards, the central question becomes whether these developments can position Saudi Arabia alongside established biotechnology hubs such as the United States and the United Kingdom.

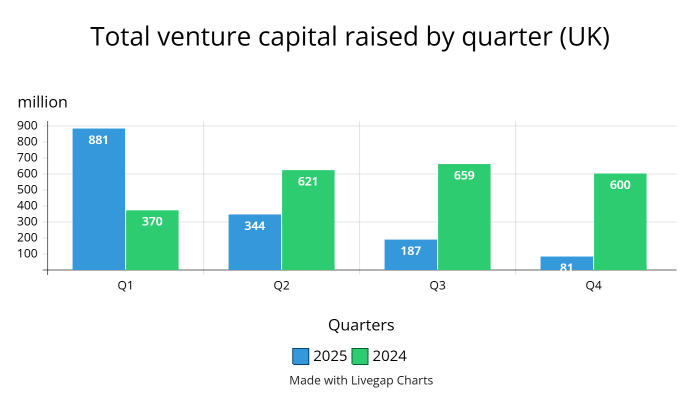

Venture capital remains the leading funding source for the U.K.’s biotechnology growth; in Q1, it was reported by the BioIndustry Association (BIA) that the U.K.’s biotech financing reached £924 million, with £881 million coming from venture capital investments and the rest from follow-on financing. Venture capital investment has raised a total of £1.41 billion YTD.

For the US, the main source of funding is a combination of venture capital investments, which have raised $16.6 billion YTD, and federal grants from the National Institute of Health; with a budget of $49 billion, the majority of it allocated to biotech research.

Similarly, China’s funding stems from government funding, with CNY 20 billion (£278 million) allocated to public biotech and R&D, as well as some international venture capitalists' investments.

While global biotech hubs rely on diverse funding models, Saudi Arabia’s biotechnology sector is funded primarily by the government. The Kingdom currently holds the highest clinical trial market value in the MENA region, accounting for around $176 million (26.38%) with a projection to reach $200 million by 2025, whilst the UAE accounts for approximately $150 million and Qatar $70 million.

With support from the government, healthcare infrastructure investment, global partnerships and regulatory reforms by the Saudi Food and Drug Authority (SFDA), the kingdom is becoming an international pharmaceutical company magnet. Saudi Arabia’s research is being sponsored by major international pharmaceutical players like Pfizer, GSK, AstraZeneca, and Nordisk.

By attracting foreign investment, Saudi Arabia gains both financial resources and cutting-edge technology, enabling research advancement, industry growth, and reduced dependence on oil revenues.

Furthermore, collaboration with global pharmaceutical experts strengthens the kingdom’s biotech knowledge base and enhances its international reputation, which in turn attracts more sponsorship. Saudi Arabia becomes the go-to destination for clinical trials in the M.E.N.A region, outpacing their competitors.

The main research focus areas are Oncology, Cardiovascular diseases, Endocrinology, and Metabolic disorders; most of the trials (48%) are taking place in King Faisal Specialist Hospital & Clinical Research Centre (KFSHRC).

Saudi Arabia primarily sources its clinical trials support and medical equipment from the United States (U.S.), as well as Germany and China. In 2025 alone, imports from the U.S. amounted to approximately $1.53 billion in medical instruments and $9.15 billion in pharmaceutical products.

The Saudi Food and Drug Authority (SFDA) aligns closely with the U.S. FDA standards, and under the Vision 2030 policy, many clinical trial imports benefit from tariff exemptions or reductions. This deliberate policy is designed to attract international pharmaceutical companies and reinforce Saudi Arabia’s role as a leading regional hub for clinical trials across the M.E.N.A region.

To understand the Kingdom’s competitive position, it is appropriate to compare its capabilities with those of established global leaders.

The U.S has earned its reputation through an extensive clinical trial infrastructure, the FDA’s globally trusted regulatory standards, an efficient lab-to-market pathway, and a deep pool of top-tier researchers from institutions such as Harvard, MIT and Stanford. Meanwhile, the U.K. has built its reputation from over 4,000 active life sciences companies and academic excellence from universities like Cambridge and Oxford. It also has the unique advantage of the NHS providing a large patient database. The current clinical market value of the United Kingdom is $3.5 billion, and the U.S sizes up as $47.18 billion.

Saudi Arabia’s market is expanding, presenting significant opportunities for investors in healthcare, biotechnology, and related sectors such as logistics, medical divisions and Contract Research Organisations (CROs).

Unlike the U.S. or U.K., where large pharmaceutical companies are publicly traded and accessible through direct share purchases, Saudi Arabia’s clinical trial activity is not currently available on the public market. Instead, investors can gain exposure through Saudi-listed healthcare companies on the Tadawul exchange, for example, Saudi Pharmaceutical Industries & Medical Appliances Corp (SPIMACO), which indirectly benefits from the growth in clinical trials.

Looking ahead to Vision 2030 and 2050, Saudi Arabia is explicitly positioning itself as a global biotech and clinical trial hub. Strong government backing provides investors with stability and reassurance, ensuring they are not navigating the market alone. This makes Saudi Arabia an attractive destination for international pharmaceutical companies seeking faster access to Middle Eastern populations.

Moreover, the Kingdom offers a unique clinical environment: high prevalence rates of diabetes, obesity and cardiovascular diseases create a larger, more diverse patient pool, in contrast to the slower recruitment often seen in the U.S. or U.K.

Whilst risks remain, such as the relatively smaller market size, reliance on government execution of Vision 2030 and 2050, and the need to further build global credibility, early investors stand to benefit if Saudi Arabia delivers on its ambitious growth goals. If the Kingdom continues to execute its strategy effectively, it has the potential to emerge as one of the most dynamic biotech markets.