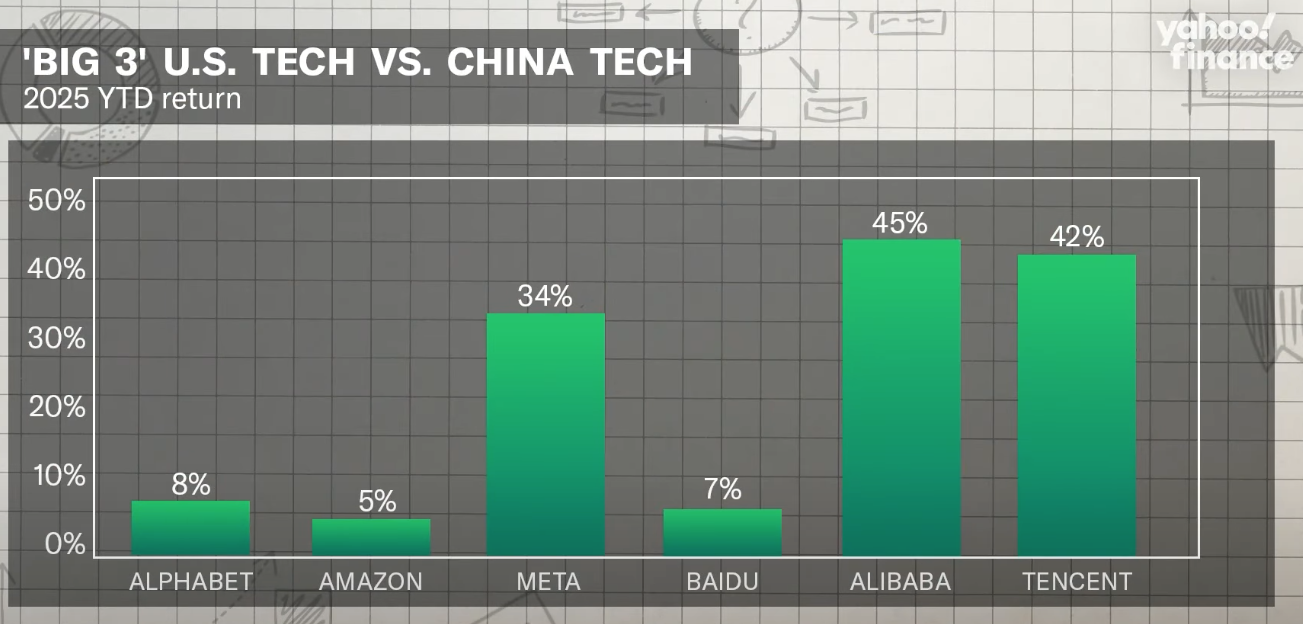

So far in 2025, U.S. tech stocks have posted mixed results. Alphabet (the parent company of Google) and Amazon have returned under 10%, while Meta has been the standout U.S performer at 34%. Chinese giants, meanwhile, are racing ahead - both Alibaba and Tencent have delivered returns above 40%, comfortably outperforming their American rivals. The KraneShares CSI China Internet ETF (an exchange-traded fund that invests in leading Chinese internet companies) has also outpaced the Nasdaq 100 ETF (an index representing the 100 largest non-financial U.S companies listed on Nasdaq) by more than 13 percentage points since early 2024.

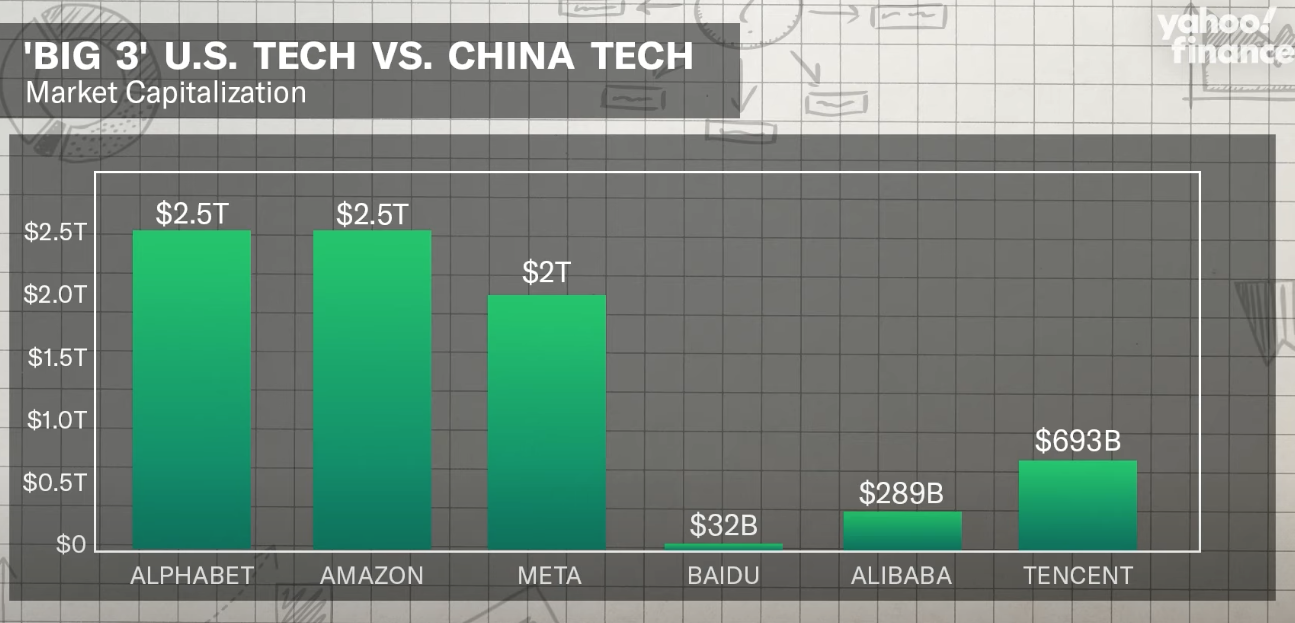

Yet performance only tells half the story. When looking at market capitalisation (the total value of all a company’s shares combined), U.S firms still dominate, with Alphabet, Meta, and Amazon each worth around $2 trillion. Chinese firms, by contrast, are valued in the hundreds of billions. This gap matters: American companies benefit from deeper cash reserves, greater flexibility in share buybacks (when a company repurchases its own shares to reduce supply and increase value), and larger budgets for research and development. Chinese firms, while growing faster, remain more dependent on domestic cycles and consumer confidence, making them agile but more exposed.

The face-offs between U.S. and Chinese firms highlight both similarities and differences. In search and advertising, Alphabet remains the global leader, but its dominance is under threat from an antitrust ruling (a legal challenge related to anti-competitive practices) that challenges its Google Search and Chrome operations. Baidu, meanwhile, continues to dominate Chinese search while pivoting heavily toward artificial intelligence (AI, the simulation of human intelligence by machines) as a new growth driver.

In e-commerce and cloud, Amazon continues to rely on Amazon Web Services (AWS) as its profit engine, giving it financial stability. Alibaba is also leaning on its cloud operations, integrating AI to boost growth. But whereas Amazon faces antitrust rumblings in the U.S, Alibaba’s fortunes are more directly tied to Chinese consumer sentiment and government stimulus cycles (the government efforts to boost the economy).

In social media and entertainment, Meta’s global reach through Facebook, Instagram, and WhatsApp has given it a vast advertising scale. Its push to monetise messaging (turning services like messaging into revenue) represents a promising new revenue stream. Tencent, on the other hand, is building out an entirely different ecosystem with WeChat - the “super app” (an all-in-one platform offering messaging, payments, social media, and more) that integrates messaging, payments, gaming, and social media all in one. With its gaming division rebounding, Tencent continues to dominate China’s digital landscape in a way Meta cannot replicate in the West.

Beyond company matchups, China’s digital market itself offers extraordinary growth potential. In 2023, online retail sales reached $2.1 trillion, nearly double the U.S.’s $1.1 trillion. Online shopping already makes up 32% of China’s total retail sales compared with about 15% in the U.S. With 1.09 billion internet users (over three times the U.S’ total) China’s scale advantage is clear, even with lower per capita penetration.

Another factor is valuation. China’s so-called “Dragon 7” (the seven largest and most influential Chinese tech companies, similar to the U.S. “Magnificent 7”) trade at far lower valuations despite strong cash reserves and growth prospects. For investors, this combination of discounted prices and a vast consumer market is an attractive entry point, particularly when seeking investment diversification outside the U.S. In fact, as one analyst put it, the rally that began in the U.S. AI sector has “broadened out” into Chinese stocks because their cheaper valuations make them a logical next play for investors chasing growth.

No investment story is without risks, and Chinese tech is no exception. Domestically, companies remain vulnerable to regulatory intervention, as seen in past crackdowns on gaming, data security, and fintech. While Beijing’s stance has softened recently, the possibility of sudden policy changes lingers. Geopolitically, U.S-China tariffs also add volatility, with shifting trade agreements often influencing investor attitudes.

Meanwhile, the U.S tech giants face their own challenges. Anti-trust scrutiny threatens Alphabet, Amazon, and Meta, potentially reshaping their dominance in search, e-commerce, and advertising. This creates a parallel risk dynamic: Chinese firms contend with government oversight, while U.S. firms navigate the courts.

But overlaying all this is artificial intelligence, the single most important factor shaping the next decade. Both sides are racing ahead, and capital expenditures (CapEx, the money companies spend on physical or technological assets) on AI are staggering. U.S. hyperscalers (large tech companies providing cloud computing services) have already increased expected 2025 AI spending from $280 billion to $360 billion, a figure projected to rival U.S. defence spending in the coming years. This surge reflects an arms race toward artificial general intelligence (AGI, AI capable of human-level thinking), with firms like Meta hiring engineers at extraordinary costs and refusing to scale back.

China, however, is also making strides. Companies like Alibaba are beginning to show visible returns on AI investment, and Baidu has doubled down on AI to reaccelerate growth. Meanwhile, DeepSeek has demonstrated that advanced AI can be developed without access to U.S. top-tier chips, a breakthrough that could reduce China’s vulnerability to American export restrictions. Importantly, AI workloads are shifting: more than 50% are now “inference” (the stage where AI is applied to generate revenue) rather than “training” (the stage where AI models are being built and refined), suggesting that real revenue is finally being unlocked from AI rather than just capital sunk into development.

To conclude, Chinese technology companies remain smaller in scale but are currently outperforming their American peers in returns. With a massive consumer base, booming e-commerce market, and relatively low valuations, Chinese tech presents an appealing entry point for investors looking beyond U.S. mega caps (large, dominant companies in the stock market).

While regulatory risks and geopolitical tensions remain, the sector is insulated from China’s real estate and banking challenges and is viewed as strategically vital by the government. If AI adoption continues to accelerate, particularly as inference-driven monetisation ramps up, and valuations stay attractive, Chinese tech could represent a generational opportunity, much like U.S. tech stocks in the aftermath of the 2008 financial crisis.

"Clearly the U.S. and China trade tensions abound, but investors are looking past this and trying to make bets on Alibaba and the China tech market, a smart move in our view," said Wedbush's Dan Ives. (Investor Business Daily, 2025)

For investors seeking growth and diversification, the “Dragon 7” may indeed prove to be the next big bet.