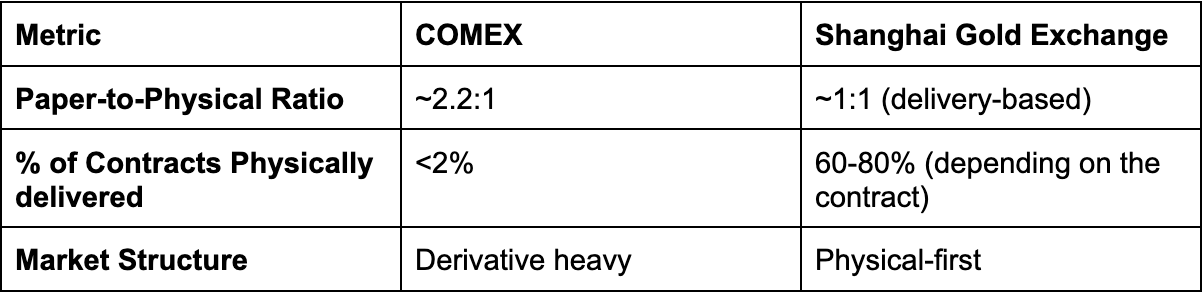

Western gold markets – COMEX in New York and the London OTC market – are dominated by derivatives and unallocated accounts, in which most positions are financial claims rather than physical metal. On COMEX and in London, the volume of gold derivatives and claims exceeds the actual amount of metal that is immediately available for delivery – the paper to physical ratio is 2.2:1 –, meaning that there are more paper gold trades than there is physical gold. Regulatory safeguards like margin requirements, delivery limits, and vault audits exist to maintain confidence and prevent systemic failure, but they do not require one-to-one physical backing. As long as most traders roll over or close positions before delivery, the system remains liquid.

Gold is often seen as the ultimate safe-haven asset, but the disconnect between financial exposure and tangible gold is rarely discussed, yet it underpins the entire system. What happens if confidence cracks?

COMEX vaults hold two categories of metal:

Over 98% of COMEX gold futures contracts are never physically delivered; instead, they are rolled over or settled in cash (traders close their expiring positions without taking physical delivery). As early as 2026, COMEX had over 1.26 million kilograms tied up in open future contracts, but the actual amount of physical gold available for delivery was much smaller.

This system functions smoothly as long as participants are content to settle financially. If a large group of contract holders requested physical metal, the system's leverage would be tested.

The fragility of paper-based gold markets is not theoretical; it has been tested before.

In the 1960s, eight Western central banks formed the London Gold Pool, combining reserves to defend the previous official $35/oz price and preserve confidence in the dollar.

This scheme collapsed when physical gold overwhelmed the London Gold Pool.

A similar stress emerged during the 2020 COVID liquidity shock; shipping issues caused a mismatch between gold futures in the COMEX and physical gold in the London OTC market. Prices drifted apart, delivery became tricky, and COMEX had to create a new type of contract for larger gold bars to ease the tension. This demonstrated how fragile the markets can get when physical gold becomes hard to move.

Over the past 12 months, gold has trended higher, reaching multiple record highs before a minor pullback in recent weeks. Spot gold prices climbed steadily throughout the year.

Presently, if demand for physical gold suddenly surges while the actual supply remains limited, the system could face a liquidity crunch, revealing how heavily the market relies on paper claims that aren’t backed by real metal.

If investors suddenly demanded physical delivery, gold prices could spike sharply, as converting vast paper positions into deliverable bullion requires time‑intensive refining, certification, and logistics that expose the system’s limited physical capacity.

Turning gold into its deliverable form takes time, and prices could skyrocket. Banks might struggle to meet demands, and trust in paper-based gold accounts could weaken. Over time, this would push gold prices higher and make people prefer gold that they can actually hold rather than promises on paper.

China has been the largest gold producer globally for years, and the largest consumer of gold, giving it a uniquely dominant position in the global bullion ecosystem. Their gold production reached approximately 380,000 kilograms in 2025, accounting for nearly 10% of global output and marking a 1.09% year-on-year increase.

This steady growth is only part of China’s advantage. By controlling the world’s largest LBMA-accredited refineries, China operated a fully vertically integrated gold infrastructure - from mining and refining to exchange trading and reserve accumulation. This integration not only ensures reliable physical supply for the Shanghai Gold Exchange but also strengthens China’s influence over physical gold flows at a time when Western markets remain heavily dependent on paper-based trading systems. Such dominance allows Beijing to quietly shape global price discovery and hedge against dollar volatility, reinforcing gold’s role as a cornerstone of its long-term financial sovereignty

When contrasted with Western paper-based systems like COMEX and the London OTC, where most trades are financial claims rather than physical metals. China’s production is strategically important because it reduces the reliance on foreign supply, and supports China’s long term receive accumulation strategy.

The Shanghai Gold Exchange is structured around physical bullion – SGE (Shanghai Gold Exchange) contracts are backed by metal in certified vaults, making China’s production capacity a critical pillar of market integrity. As global demand for physical gold rises (+4.5% YoY), China’s delivery-backed infrastructure is strengthened.

PBoC (The People’s Bank of China) has added over 1,600,000 kilograms of gold to its reserves over the past decade and has resumed visible buying recently. Gold accumulation is widely interpreted as a strategy to diversify reserves away from the dollar, build sanction-resistant reserves and strengthen monetary sovereignty.

If more trades and reserves are settled and priced through Shanghai’s physical gold market, London and New York risk losing their dominance in global price-setting.

China has already launched yuan-denominated benchmarks and is building a “gold corridor” with BRICS and other partners to prompt physical settlement. Meanwhile, documented delivery strains in London, where physical gold availability has repeatedly lagged behind paper claims, highlight how tight supply can undermine the illusion of infinite liquidity.

As these gaps become more visible, Western credibility in gold pricing could erode, especially if participants begin to favour markets like the SGE, where delivery is mandatory, and contracts are backed by real metal. This shift would erode Western credibility on gold pricing and reduce the influence of the COMEX and the London OTC market.