• Peace Premium Effect: The October 2025 Gaza ceasefire has reduced regional uncertainty, leading investors to cautiously reprice Gulf assets higher as stability, foreign inflows, and cooperation expectations improve.

• Sector Rotation Signals: Early capital is moving toward banking, consumer, and tourism sectors, supported by strong fundamentals such as rising credit growth, tourism expansion, and long-term diversification plans like Saudi Vision 2030.

• Uneven but Growing Optimism: While market gains remain modest, sentiment across Saudi Arabia, the UAE, and Qatar shows that easing geopolitical tension is strengthening confidence and laying the groundwork for longer-term, non-oil-driven growth.

This dynamic is supported by larger studies from the International Monetary Fund, which find that geopolitical tensions and conflict tend to weigh heavily on markets by suppressing valuations and raising sovereign risk premiums, particularly in emerging economies. When those risks decline, the opposite effect often occurs: improved stability attracts capital and lifts asset prices as investors begin to discount the likelihood of contagion through trade and financial markets.

As of right now, the Gulf markets have not yet skyrocketed, yet there is a cautious sense of optimism that under this US-backed peace framework, Saudi Arabia and the UAE could emerge as key beneficiaries of a more stable post-conflict environment. This report explores how that optimism is shaping Gulf equities, and whether it can truly last.

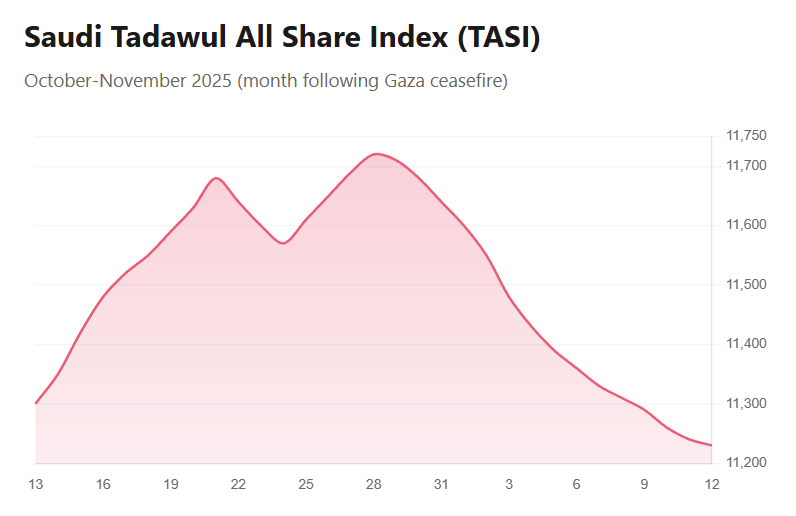

In the weeks following the ceasefire, Gulf equities displayed a modest but telling rebound. In Saudi Arabia, the Tadawul All Share Index rose from 11,494 on October 12 to 11,753 by the end of the month, an increase of roughly 2.3%. Meanwhile, in the UAE, the Abu Dhabi Securities Exchange edged up from 10,106 to 10,212, gaining about 1.0% over the same period.

While these movements may appear insignificant on the surface, they carry symbolic weight in a region where markets are highly elastic as a result of fluctuations in geopolitical risk. Even a small rally suggests investors are tentatively repricing regional assets in line with expectations of stability and renewed cooperation. The brief pullback that followed at the start of November likely reflects profit-taking and the natural recalibration of markets still wary of lingering political uncertainties, rather than a rejection of the emerging optimism.

Interestingly, while Saudi and Emirati markets registered only tentative gains, Qatar’s QE Index kept rising, from 10,846 on October 12 to 11,141 by mid November. This resilience comes despite Qatar itself hosting a major Israeli strike in its capital in September, suggesting that investors may be distinguishing short-term geopolitical risk from longer-term economic fundamentals. In that sense, while the “peace premium” is uneven across the Gulf, it remains a shared undercurrent shaping sentiment in the region’s major markets.

This growth was predicted by analyst Nigel Green, who noted that the world has been conditioned to price in war risk for two years. If the Trump-brokered deal marks a credible path to lasting peace, that risk premium collapses. Capital will flood back into markets that have been sitting in a holding pattern. This has come into fruition with notable foreign inflows and signs of renewed investor confidence, showing that investors are responding to the shifting geopolitical landscape. In practical terms, this optimism is reflected in increased attention to key financial, infrastructure, and consumer firms, with investors slowly rotating into sectors poised to benefit from domestic demand and restructures.

Additionally, the recovery is consistent with longer-term, more comprehensive narratives in the area. Vision 2030 is still driving diversification initiatives in Saudi Arabia, boosting tourism, tech, and manufacturing. In a similar vein, government programmes in the UAE to grow non-oil industries and draw in international capital seem to be boosting investor confidence. Taken together, these policy frameworks explain why even modest market gains, as seen in the weeks following the Gaza truce, can be viewed as early indicators of a gradually stabilising, reform-driven market environment rather than brief spikes.

Energy continues to be the major engine of Gulf economies, but investors are turning their attention more towards non-oil sectors. This is a significant indication that the peace premium is permeating core market standpoints. One such beneficiary is banking. According to a recent sector-outlook analysis, banks in the Ernst & Young GCC banking study produced an average return on equity of 13.2% in the first half of 2025, with non-performing loan rates dropping from 2.8% to 2.4%. Furthermore, Mayur Pau, MENA Financial Services Leader at EY, stated that credit growth remains solid, supported by strong corporate and retail demand. These figures show that real-world banking fundamentals encouraging confidence are aligning with even slight changes in market sentiment.

Likewise, in the consumer and tourism arena, the Gulf’s peace premium is beginning to show real traction. Dubai has already seen a 6.1% increase in tourism compared with 2024, a figure likely to rise further now that conflict has subsided. Meanwhile, a McKinsey study highlights the depth of untapped consumer potential, with Saudi consumer spending expected to grow significantly as the population increases and income levels shift.

While these figures predate the ceasefire, they highlight the appeal of consumer and tourism sectors, which are now receiving renewed attention as geopolitical risk eases. But caution is still advised. A measured approach to risk in a region where geopolitical events may quickly shift sentiment is reflected in the fact that many investors are still holding off on making significant bets until there is continuous peace and policy continuity. Nevertheless, the Gulf consumer and tourism industries are now receiving more attention due to the combination of solid sector fundamentals and decreased regional tension, which is a clear example of the so-called peace premium.

In conclusion, the early indications of increased capital flows, sector rotation, and investor interest highlight the creation of a peace premium, even though Gulf markets have not yet produced notable post-ceasefire gains. A cautious but growing optimism is being fostered by the UAE’s diversification initiatives, structural reforms like Vision 2030, and the reduction of geopolitical tensions. These elements could support longer-term growth in banking, consumer, and tourism sectors, indicating that Gulf stocks are gradually shifting towards a more stable and diverse economic future. If peace endures, the Gulf’s markets may finally start to reflect the potential of this new stability.