.png)

The usual carry trade would work similar to this: borrow a low-yield currency (funding currency: JPY), and use this cash to invest in high-yield assets, offering greater returns like US treasury bills (target currency: USD). The main incentive behind this maneuver is steady, stable profit - the difference between the two rates (interest rate on the loan, and yield rate on the bond). The monthly payment of the bond would be received, converted from USD to JPY, and then the loan would be repaid, leaving what’s left as profit. In the past, these high-yield assets would involve the Mexican Peso (MXN) and Brazilian Real (BRL), because of high real interest rates, as Mexican and Brazilian central banks not only had high interest rates, but had much lower inflation as well.

However, these currencies were traditionally high-beta assets, meaning when the market goes up, these investments tend to perform much better; however, they tend to fall by a greater percentage when there is risk-off sentiment. Generally, developed economies have lower interest rates, so when the Japan tightens its monetary policy for example, this has 2 major implications: 1) investor profit falls, as the interest rate differential narrows, potentially even leading to a loss 2) suggests higher rates of inflation, and by extension greater macroeconomic uncertainty. As a result, to protect their existing profits, and to hedge against further risk, capital is reallocated towards safe-haven assets, such as gold or US bonds, resulting in sudden fall in currency value.

So what does all this mean? The main reason investors bought Mexican and Brazilian assets wasn’t due to positive, structural changes to their respective economies, but rather, it was due to global risk-on appetite. Alas, the playbook has changed…these South American economies have experienced years of meaningful, purpose-driven, proactive change, positioning them as resilient stalwarts.

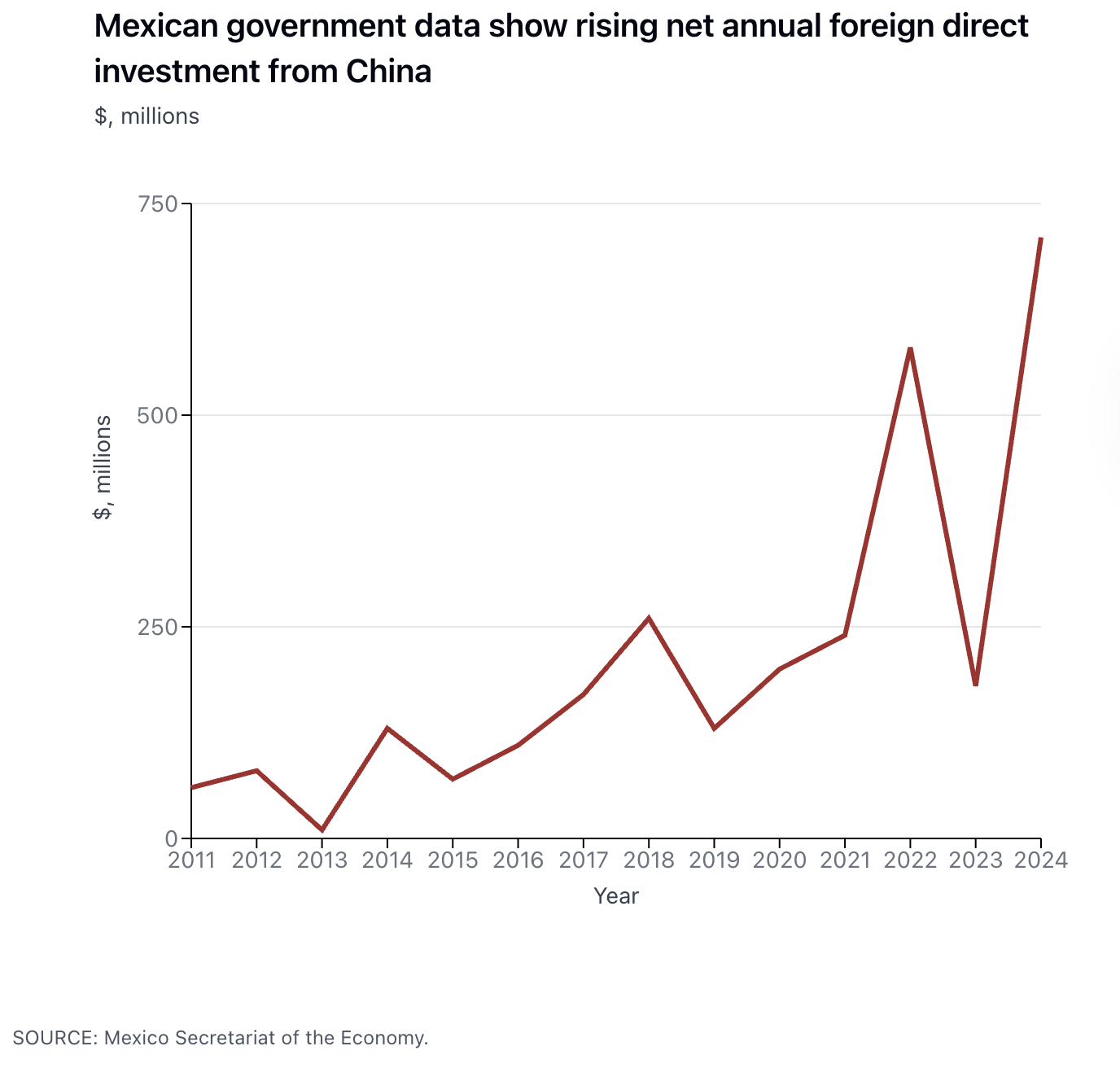

One of the key reasons behind MXN’s resilience and lower volatility comes down to China. The US-China trade war in 2018, under Trump’s first regime, posed a huge threat to Beijing, given the nation’s export-oriented economy, as the US was the largest partner to China. Such high tariffs would reduce exports (particularly electric vehicles), due to higher prices, meaning the US would likely purchase substitute goods from other lower-cost countries or even expand supply themselves, and revive their old industrial hubs. As a consequence, China decided to offset the effects of tariffs through investing heavily in Mexico, given its close geographic proximity to the US, relaxed labour laws, and cheaper wages. Due to the USMCA Agreement, if at least 75% of automotive manufacturing took place in North America, then the product would qualify for 0% tariffs. This proved vital for China, as it invested heavily in building factories and training workers to produce parts in Mexico to qualify for these exemption, whilst also gaining soft power in Mexico due to its involvement in improving living standards and providing employment, which raised government revenue through income and corporation tax. From Figure 1 (below), it is evident that Chinese investment in Mexico accelerated following the US trade war, and sharply increased further once the USMCA took effect from mid-2020.

Given that 75% of manufacturing must be done in North America to qualify for tariff exemptions, firms spent massive amounts of money in Mexico, including local wages, Mexican suppliers, and electricity. Hence, this constant spending keeps demand for the Peso high, thereby strengthening it, and making it more resilient to external shocks. As a result of foreign direct investment, or “sticky money”, this keeps MXN higher and more stable for longer due to long-term contract agreements, as these Chinese companies make it much harder for US policymakers to cut them off, as it would hurt the North American supply chain. Analysing this further, the benefits of investing in Mexico isn’t just financial, but also logistical. This is because nearshoring allows Chinese firms to rapidly respond to changing American consumer trends and demand surges without the risk of their goods being on a cargo ship for weeks, due to closer geographical proximity.

Whilst these Chinese firms could repatriate their profits back to China, brownfield investment makes the Peso even stronger. Interestingly, many of these companies would much rather strengthen their Mexican base further, given US demographic characteristics (large population with high levels of disposable income). Therefore, they often reinvest profits to enhance their operational capabilities, through purchasing more Mexican-produced machinery, land or constructing even larger factories. Finally, unlike hedge funds, which can sell Mexican currency or bonds in seconds, profit repatriation is a much slower and regulated process involving a longer term horizon, which prevents a massive sell-off (anchor effect) in times of economic turmoil. This protects the Mexican Peso, making it a volatility buffer, and lowering its beta.

Whilst Mexico’s location helped it attain currency strength, Brazil managed to attain the same outcome through its use of endogenous resources. In 1974, the US and Saudi Arabia struck a landmark agreement, whereby Saudi agreed that oil would be priced exclusively in USD, in exchange for US military protection. Consequently, this forced countries to hold large USD foreign currency reserves to purchase the oil. This deal sealed the Dollar as the world’s primary reserve currency, but proved an issue for Brazil. When oil prices increased, more USD had to be used to purchase the barrels, meaning USD strengthened, as many other countries would also be demanding this currency on forex markets. As this would weaken the BRL relative to USD, this represented a vast opportunity cost for the Brazilian government: rather than spending on improving infrastructure, healthcare, and education in the country, it had to spend more on buying USD, just to afford these oil imports.

In order to afford this spending, the government raised debt through sovereign bonds; however, as an emerging economy, it was not a very trustworthy and reliable country to lend money to. This resulted in bonds being sold in USD, given the Dollar is a safe haven asset, meaning investors were more willing to accept a lower yield rate on a Dollar bond than on a Real-denominated bond. Furthermore, the world’s largest institutional investors, from insurance companies to pension funds, mostly hold hard currencies such as GBP or USD, thus allowing the government to have better access to capital. Finally, from the 1960s through the early 1990s, Brazil experienced prolonged periods of hyperinflation, even approaching and stabilising at 100% per year, which posed a major threat to investors. Given the Real’s fragility, lending in BRL could lead to half of the currency’s value being lost in a few months, as the real rate of return may even be negative, making it a not worthwhile investment. As a result, this further constrained Brazil into dollar-dependence, and weakened the BRL further.

Not only was Brazil a net importer of oil, but also of food, and struggled with chronic insecurity, resulting in famine and malnutrition for large parts of the population. The key turning point emerged with the creation of Embrapa (the Brazilian Agricultural Research Corporation) in 1973, resulting in production increasing by over 500% in the following decades. How did this happen? Researchers adapted crops like soybeans, traditionally a temperate climate plant, to thrive in the Cerrado - a massive, acidic tropical savannah, once thought to be surplus to farming requirements due to the property of soil it contained. Through using lime to fix soil acidity, and using technology to adapt seeds (“tropicalisation”), these large productivity gains were achieved.

Due to these structural changes, Brazil has emerged as a global soft commodity powerhouse, now holding $360bn in reserves. This Dollar surplus acts like a barrier, helping to reinforce the BRL, as the USD from export revenue must be converted into local currency to pay workers and suppliers. Continuing to do this leads to BRL being exchanged constantly with USD, with the increase in demand for BLR resulting in appreciation of the domestic currency. Whilst this benefits imports, the high currency valuation makes exports less price competitive and can lead to a phenomenon known as the ‘Dutch Disease’. This is where a boom in one sector, like agriculture, makes the currency so strong that it inadvertently destroys other sectors like manufacturing, since Brazilian-made cars or clothes are now too expensive, relative to other countries’ exports of similar goods. As a result, the central bank often steps in to weaken the BRL against the Dollar, by selling some of its USD reserves to maintain international competitiveness, and stabilises the currency.

Furthermore, due to the large USD reserves, the government no longer needs to sell BRL to purchase dollars to pay back interest on its sovereign debt. This helps negate severe price fluctuations, and restores faith in the Real. However, dollar-denomated debt is becoming less of an issue now, as there is greater investor confidence in the Brazilian economy, resulting in more government bonds being issued with the local currency. This is beneficial as, in the worst case scenario, investors can always get their money back with interest, as Brazil has the option to simply print more of its currency and ‘inflate away’ its debt.

While the structural shifts in Mexico and Brazil are compelling, the most definitive evidence of their transformation lies in the quantitative data. For decades, the Brazilian Real (BRL) and Mexican Peso (MXN) moved in tandem with global fear, with this relationship measured by the VIX (CBOE Volatility Index), often called the market’s "fear gauge". Historically, a spike in the VIX (signaling global panic) triggered an automatic sell-off of these high-beta currencies. However, this correlation has significantly weakened due to the "Dollar Buffer" in Brazil and the "Sticky Money" situation in Mexico, which have allowed these currencies to decouple from global volatility. This has resulted in them no longer behaving like mirrors of US market conditions but as independent, resilient, long-term assets.

The Mexican Peso and Brazilian Real were high-beta proxies for the VIX, meaning a 10% spike in the VIX often triggered a 2-3% immediate sell-off in LatAm FX, due to exits in South American equity markets. However, current data suggests a shift: in 2024-2025, the correlation coefficient between the MXN and the VIX dropped from a historical average of 0.6-0.7 to below 0.35, signaling that this currency is no longer a reflection of exogenous events and but driven by its own government and central bank policies.

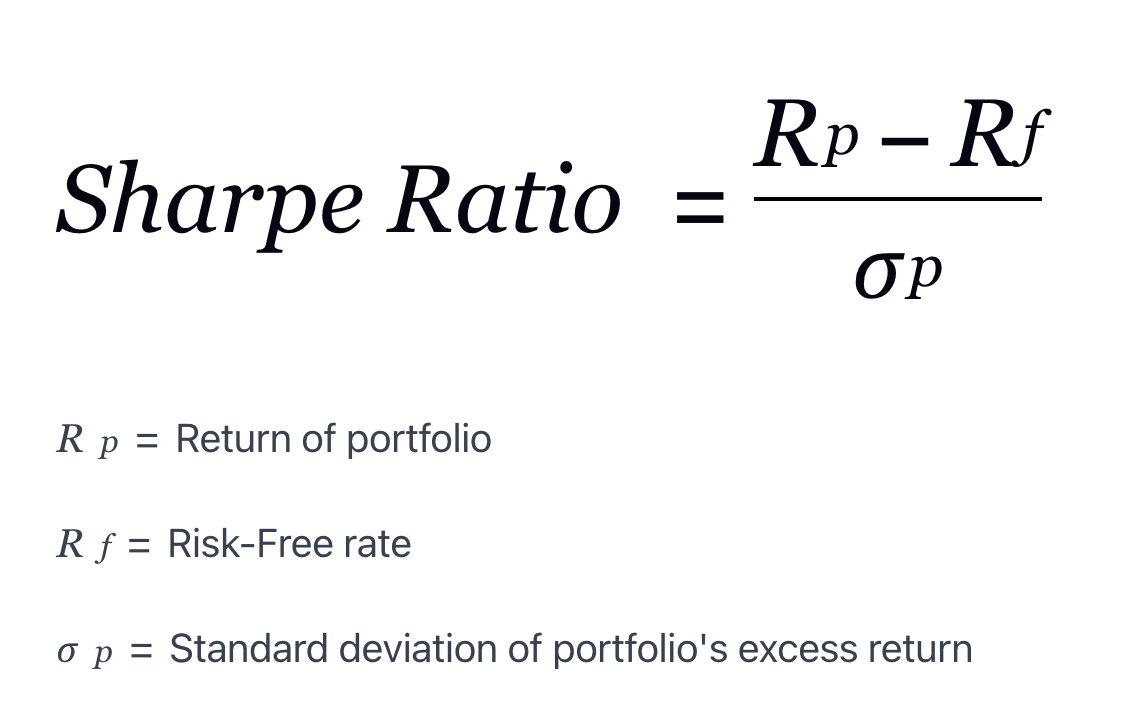

This reduction in volatility, combined with high real interest rates, has fundamentally altered the Sharpe Ratio for these trades. In finance, the Sharpe Ratio measures risk-adjusted return: how much profit an investor earns for every "unit" of risk they take. As the volatility (the "Risk-Free rate”) of the BRL and MXN decreases while their yields (the "return") remain high (see Figure 2 for full equation), their Sharpe Ratio improves dramatically, as the numerator value increases, assuming standard deviation remains constant. As a case study, Bank of America's BRL/MXN long position offers 5.6% annual positive carry with ~12% historical volatility, yielding a theoretical Sharpe Ratio of approximately 0.47. For comparison, this significantly exceeds typical G10 currency pair Sharpe ratios of 0.3-0.5 mentioned in academic literature on carry trades, suggesting greater investment returns. For wider global comparisons, ING's backtest analysis of Latam carry strategies (Brazil, Mexico, Colombia) showed these regional blocs "performed pretty well as carry trade strategies" with superior Sharpe Ratios compared to Asian alternatives as well. Overall, this shift of South American currencies becoming more stable, with favourable ROI is watched by institutional investors, as it is a magnet for algorithmic models, which prioritise mathematical efficiency over speculative gambles.

To conclude, by breaking the "chain" of high-beta dependency, these currencies have moved from the periphery of a portfolio to the centre, providing the "structural alpha" required in a modern, de-dollarising world. By taking advantage of endogenous natural resources, and geopolitical situations, all whilst maintaining prudent financial decisions, Brazil and Mexico demonstrate a clear template towards greater economic sovereignty.