Bitcoin is said to have a supply cap of 21 million coins which is embedded and cannot be changed without consensus from its network. As a result, this cap creates digital scarcity for bitcoin, making it very similar to the likes of gold. Now, using simple economic principles, we can deduce that bitcoin’s limited supply coupled with strong demand is what is facilitating price appreciation. Additionally, scarcity also helps bitcoin retain purchasing power and protects investors from inflationary pressures, since central banks cannot expand the total supply of the coin. However, the more interesting aspect of bitcoin’s valuation is in its creation. Bitcoin is created through mining, which involves solving complex puzzles and miners are rewarded per mined block, however these rewards are halved approximately every four years by a process known as ‘halving’. As a result, this reduces the issuance rate until all 21 million are mined. The key element here is that the halving schedule creates a psychological feedback loop that affects investor behaviour and price action.

This loop reinforces bitcoin’s “digital gold” narrative: fixed supply cap + predictable issuance schedule = digital scarcity → price speculation → demand → price appreciation.

Investors anticipate the halving, knowing future supply growth will be reduced. Bitcoin is then bought resulting in reduced supply which will drive the value of bitcoin higher. The buying pressure often precedes the actual halving, creating price rallies even before the event occurs and the cycle repeats. Each halving has historically coincided with major bull runs around 2012, 2016, 2020, and 2024, with the effect being both fundamental, as the reward for mined bitcoin decreases, and psychological, as demand rises due to investors' fear of missing out on potential returns.

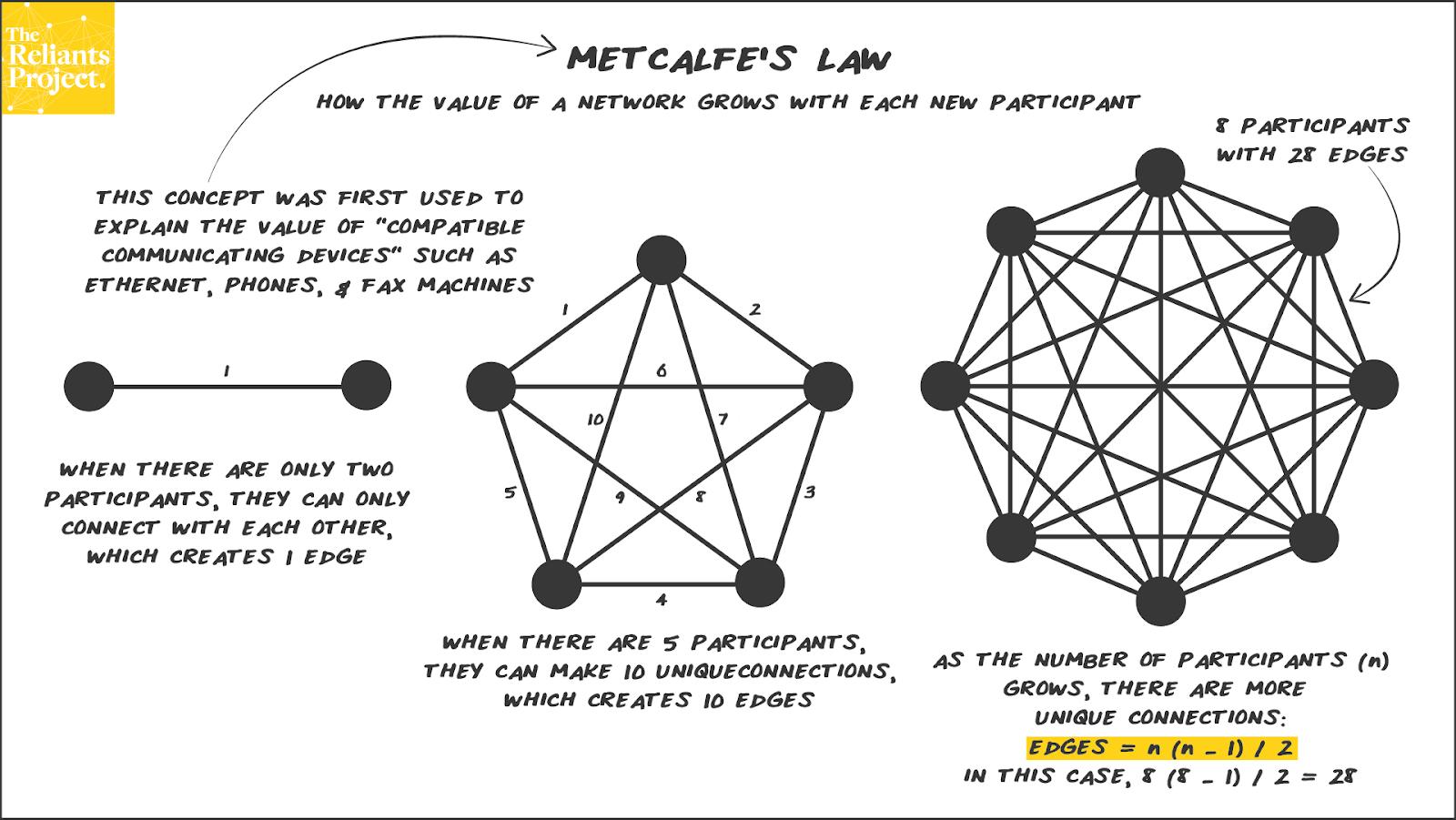

Beyond predictable issuance and scarcity, bitcoin’s value increases due to Metcalfe’s law. Metcalfe's Law states that a network’s value grows with each participant.

Now let's apply this concept to bitcoin’s market price:

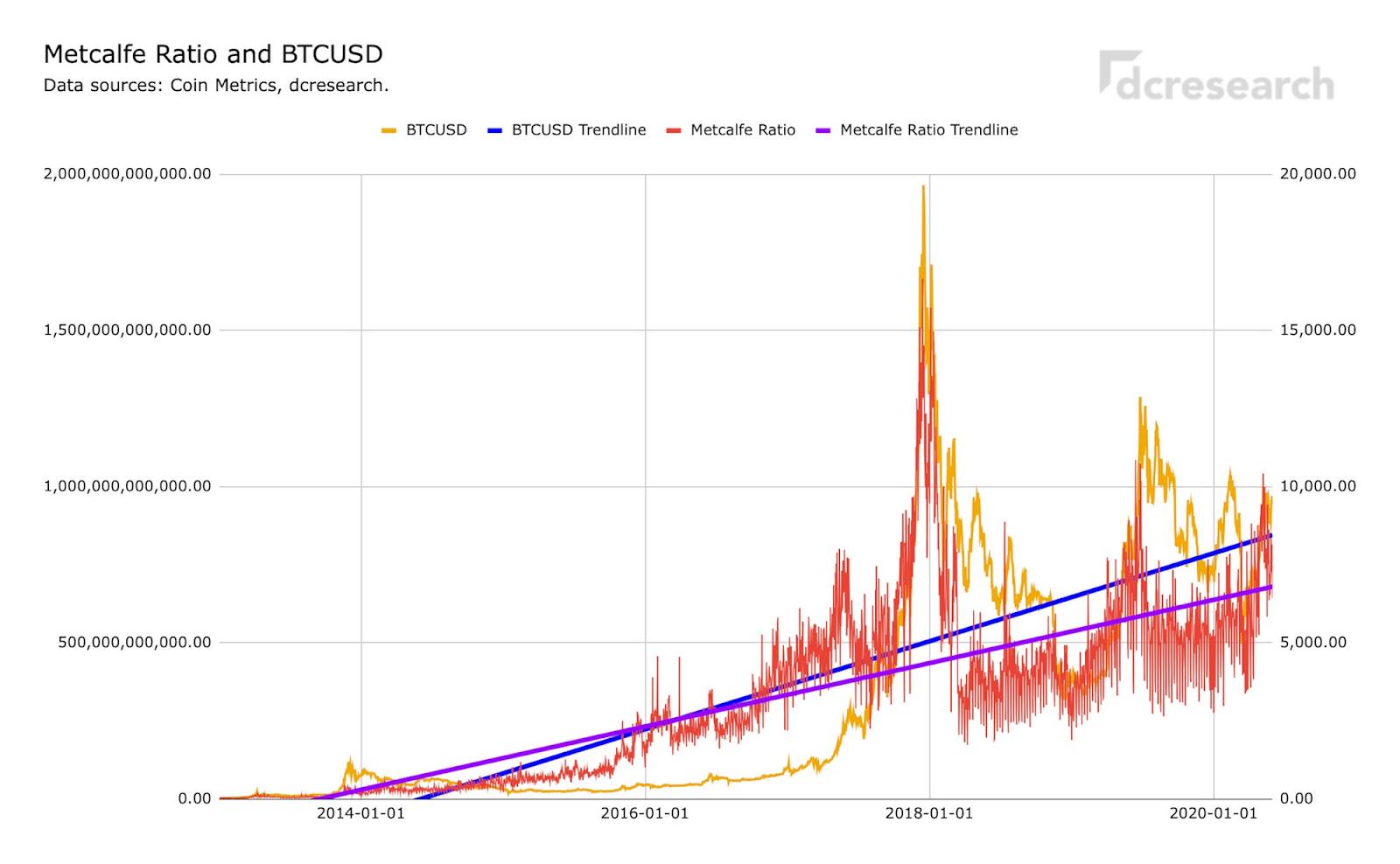

The red line (Metcalfe ratio) represents bitcoin’s theoretical valuation based on network growth. Meanwhile, the yellow line (bitcoin’s market price) represents how this relates to bitcoin’s spot market price. We can observe that over time, the two track each other closely, with a heightened Metcalfe ratio resulting in a strong rally for bitcoin and sharp declines resulting in sharp corrections in bitcoin’s market price. This relationship indicates that bitcoin’s spot market value is directly influenced by the growth of its network. As more users, wallets, and transactions enter the system, the network trust expands, supporting higher market prices. In this way, bitcoin’s price behaviour is not random but reflects the expansion of its digital network.

Decentralisation is the degree of the distribution of power, control and decision making across a network of independent individuals rather than being concentrated on a single authority. This is important because centralised systems have one single point of failure, making them more susceptible to attacks whereas decentralised systems have no single point of failure and cannot enact changes unless the majority of participating parties agree.

Firstly, it is in bitcoin’s nature to prevent centralised control to any party by evenly distributing power and control. However, control over the means of production and exchange of bitcoin is less distributed as these are designated exclusively for a handful of individuals who have the resources. This suggests that a small group practically has disproportionate influence which raises concerns over coordinated control, undermining the idea of equal distribution.

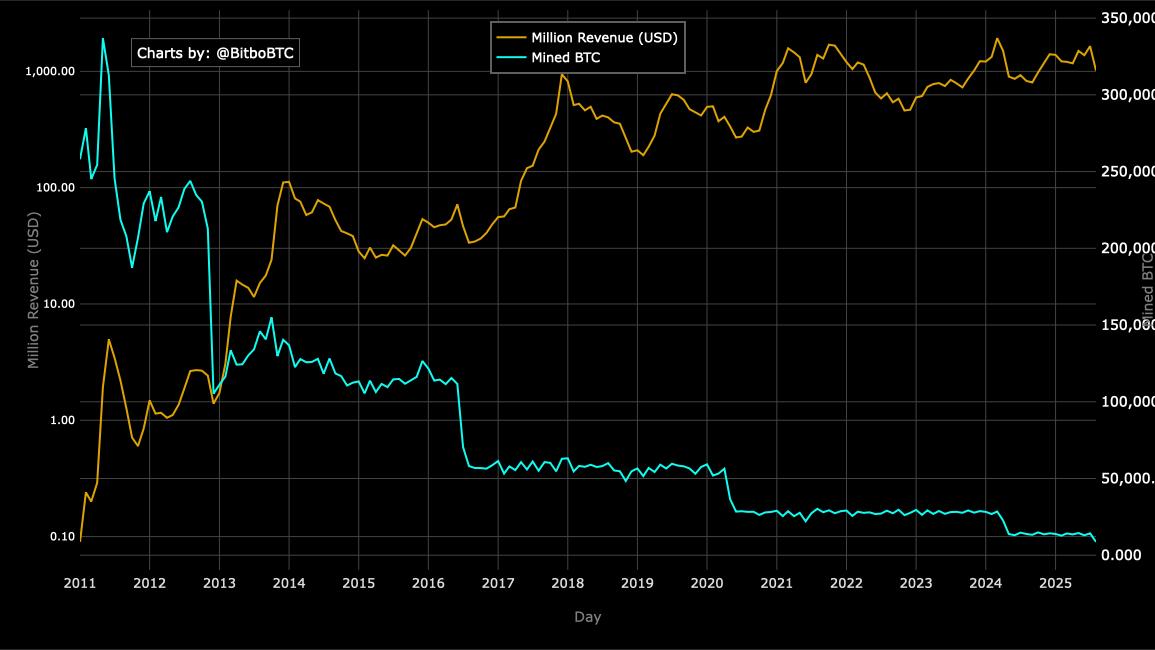

This graph illustrates “the Halving," marked by sudden drops in mined BTC and the psychological feedback loop: each halving decreases the flow of new BTC into circulation, strengthening the perception of scarcity. This often triggers rallies as investors recognise that the supply is gradually approaching the cap. Bitcoin’s economic incentives prevent collusions because self-interests keep participants aligned with bitcoin’s core principle of decentralisation rather than a centralised authority enforcing compliance. Furthermore, bitcoin’s decentralisation makes it sufficiently trustworthy to serve as a hedge against state control and censorship. However, its trustworthiness depends on investor confidence as users must accept some degree of concentration of power in miners, developers, and exchanges.

Secondly, one of bitcoin’s most popular strengths is its resistance to political or institutional seizure. The size and scale of the network, supported by global distribution with thousands of nodes makes any attempt to seize bitcoin a very expensive attempt. To do this, an entity would need to acquire control of the majority of the means of production which costs billions in hardware and electricity. However, if the state decided to regulate or nationalise major mining pools, then seizures could become more plausible.

Thirdly, open participation is one of bitcoin’s most interesting criteria because it sits at the boundary between theory and practicality. Bitcoin achieves a strong degree of open participation at the user level meaning anyone can transact however, at the infrastructural level involving issuance, participation is more restricted to individuals who have access to resources and expertise. Does this mean that “open” refers to anyone being able to join or many being able to join? Bitcoin leans more toward the former, which still makes it vastly more inclusive than centralised banking systems but partial to its feature of being “open”.

A hedge is an investment or strategy designed to protect against potential losses from adverse market movements, economic turmoil, or other financial uncertainties and gold has consistently demonstrated its role as a hedge during these periods.

Let's have a look at gold’s performance during the three biggest black swans in history:

Firstly, the 1929 Great Depression saw a major decline in the stock market after a bubble in equities which wiped out billions in wealth,bank failures, a massive unemployment rate of 25% and a decade long economic depression. Gold prices were fixed under the Gold Standard at $20.67 per troy ounce. However, gold retained much of its purchasing power while stocks and other assets collapsed and it was revalued to $35 per troy ounce under the 1934 Gold Reserve Act which effectively increased the wealth of individuals who held bullion bars.

Secondly, the 2008 Global Financial Crisis witnessed the collapse of Lehman Brothers and a worldwide banking and credit crisis triggered by the subprime mortgage market. As a result, the stock market lost 40–50% of value in some countries, unemployment surged, and governments had to bail out major banks. Gold rallied sharply as investors sought a hedge against this risk exposure. Prices rose from $800 per troy ounce in 2008 to over $1,000 per troy ounce by March 2009. In late 2008, some investors sold gold to cover losses elsewhere or meet margin calls, causing a short-term dip which shows that even gold isn’t completely immune to forced selling in acute financial stress.

Lastly, the 2020 Covid-19 Market Crash caused the fastest bear market in history. The stock market fell 34% in a month and as a result, gold initially retraced slightly in March 2020 due to liquidity crunches caused by market shock but quickly rebounded higher and by August 2020, gold hit a high of $2,070 per troy ounce, reflecting extreme uncertainty and central bank stimulus measures.

Across the three biggest black swans, gold either maintained purchasing power or rose in value, illustrating its long term reliability as a store of value.

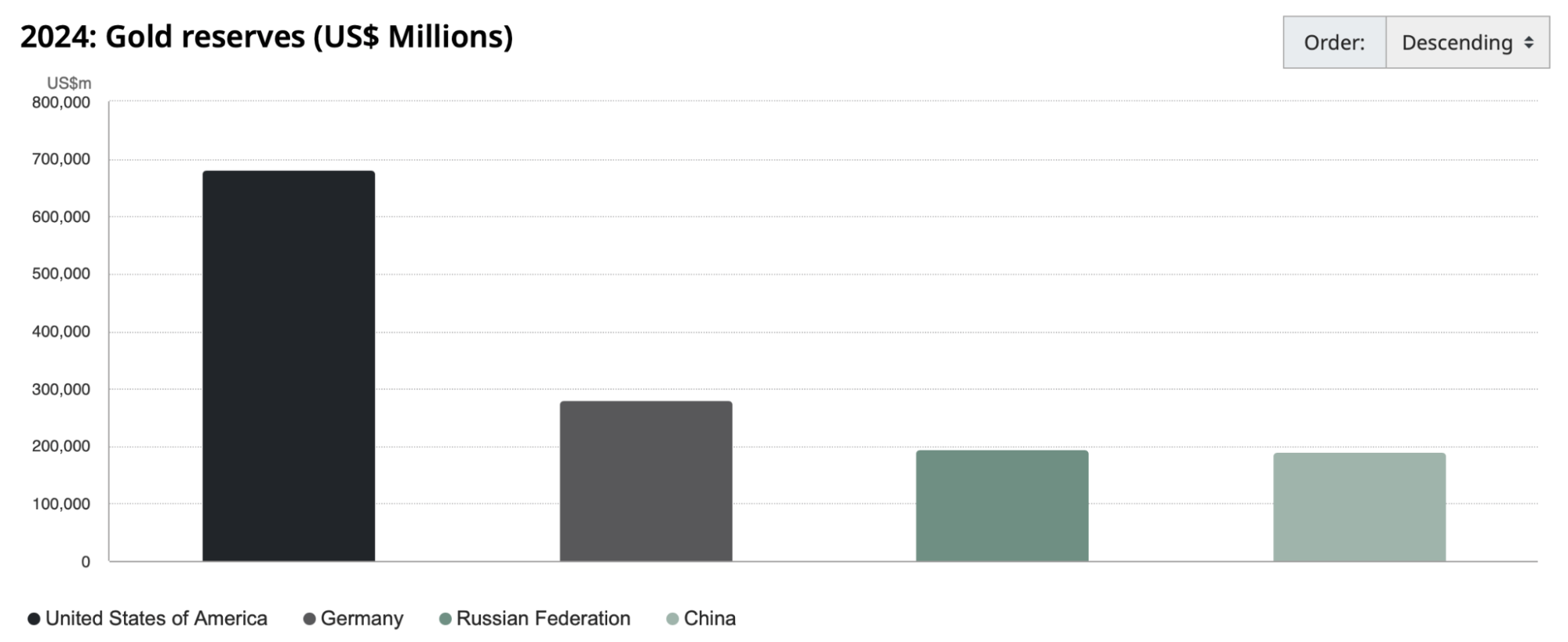

Central banks in developed economies such as the United States and Germany are among the biggest holders of bullion with wealth funds tagging along behind them reflecting gold’s role as a trusted monetary hedge and in emerging economies such as China and Russia, motivations include reducing reliance on the US dollar.

The shortcomings of the Bretton Woods in 1971 meant that central banks started using gold as a hedge against risk and this only accelerated after the 2008 financial crisis, as central banks reconsidered their position on the yellow metal and shifted from sellers to buyers. In 2024, central bank net purchases surpassed 1,000 tonnes for the third year in a row, outnumbering the previous decade's purchasing average of 400 to 500 tonnes which further emphasises gold’s elevated importance. It also offers liquidity benefits because high demand ensures high trading volumes even during periods of stress and in terms of security, gold provides sovereign level protection against counterparty and sanction risks. Finally, its aggressive buying highlights how institutions value gold not for yield but for its capacity to preserve wealth over time and during black swan events, reinforcing its role as the traditional institutional store of value.

To conclude, it is clear to me that bitcoin was developed to be a hedge from the system whilst gold is a hedge within the system. The former meets several of the formal conditions of a store of value such as decentralisation which has contributed to a largely successful distribution of power creating a truly open and censorship-resistant financial system whilst mitigating the risk of attacks and means no single entity can dictate the rules, reverse transactions, or freeze assets. Bitcoin’s fixed supply cap with a halving process offers inflation-resistant features and induces a psychological feedback mechanism to reinstate strong demand approximately every four years. This strong demand coupled with Metcalfe’s law creates a valuable market for bitcoin, granting it the ability to easily be bought and sold. Historically, its value has increased significantly over the long term and although short term volatility remains high, the predictable supply and network growth provide a framework for long-term value retention.

However, it falls short of true decentralisation because economic incentives concentrate power for mining pools and exchanges. If an entity decided to regulate or nationalise major mining pools, then seizures could become more plausible and the infrastructure level involving mining and development is more restricted to individuals who have access to resources and expertise. The latter meets all formal requirements for a store of value with fewer shortcomings compared to bitcoin. For example, gold does not depend on technical infrastructure the way bitcoin does and gold has no network to attack or mining pools to regulate or seize. Gold is a physical asset that has passed the test of time with thousands of years of decentralised ownership across many different banks, governments and investors which makes it hard for one entity to monopolise. If there is a scenario that the government does seize domestic gold, institutions still have access through ETFs and physical vaults worldwide. This ties back to liquidity, stability and security because gold markets are deep and liquid, less prone to technological or regulatory shocks and does not rely on a network of actors.