.png)

Arm does not make chips. Or rather - it didn’t, until last Tuesday.

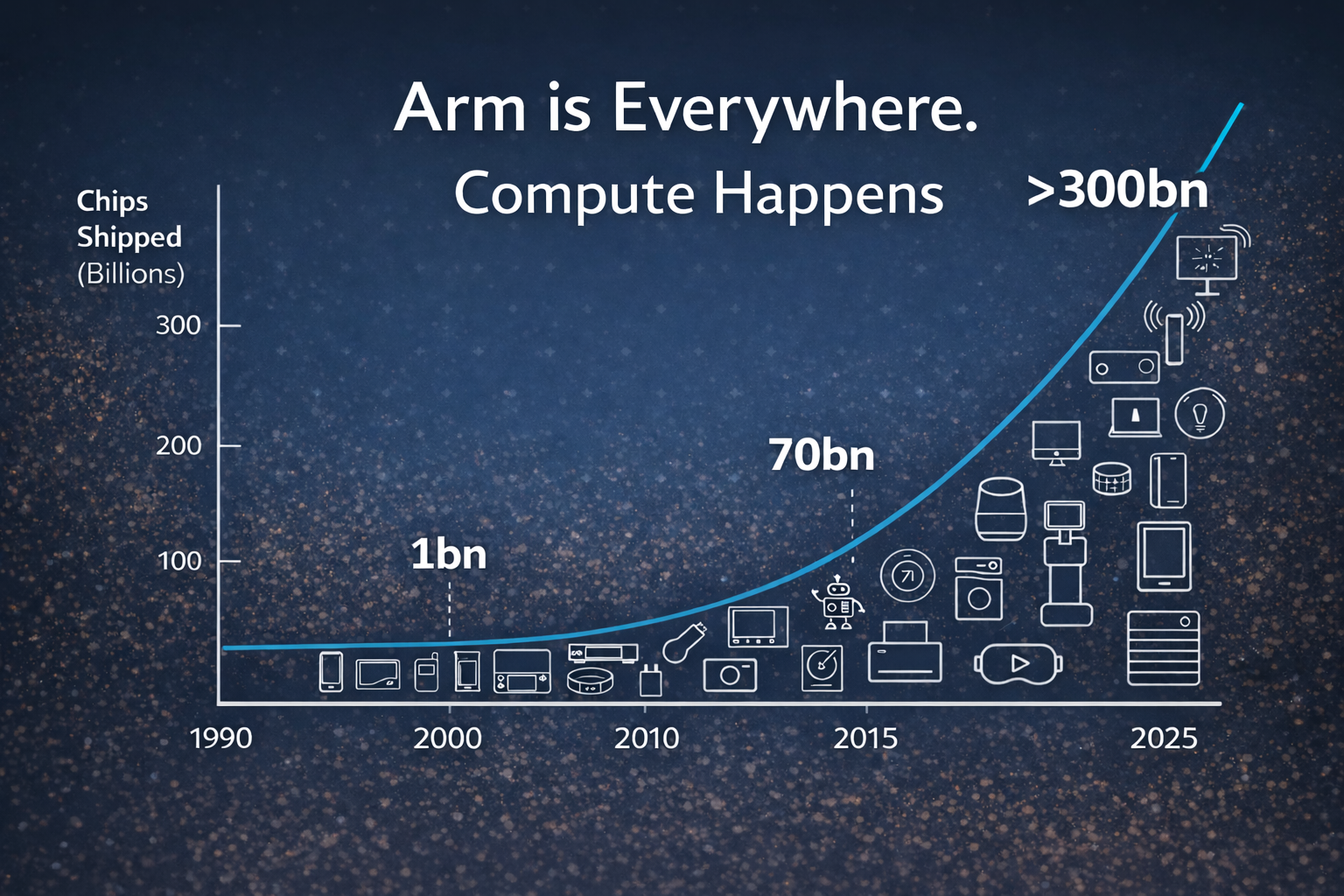

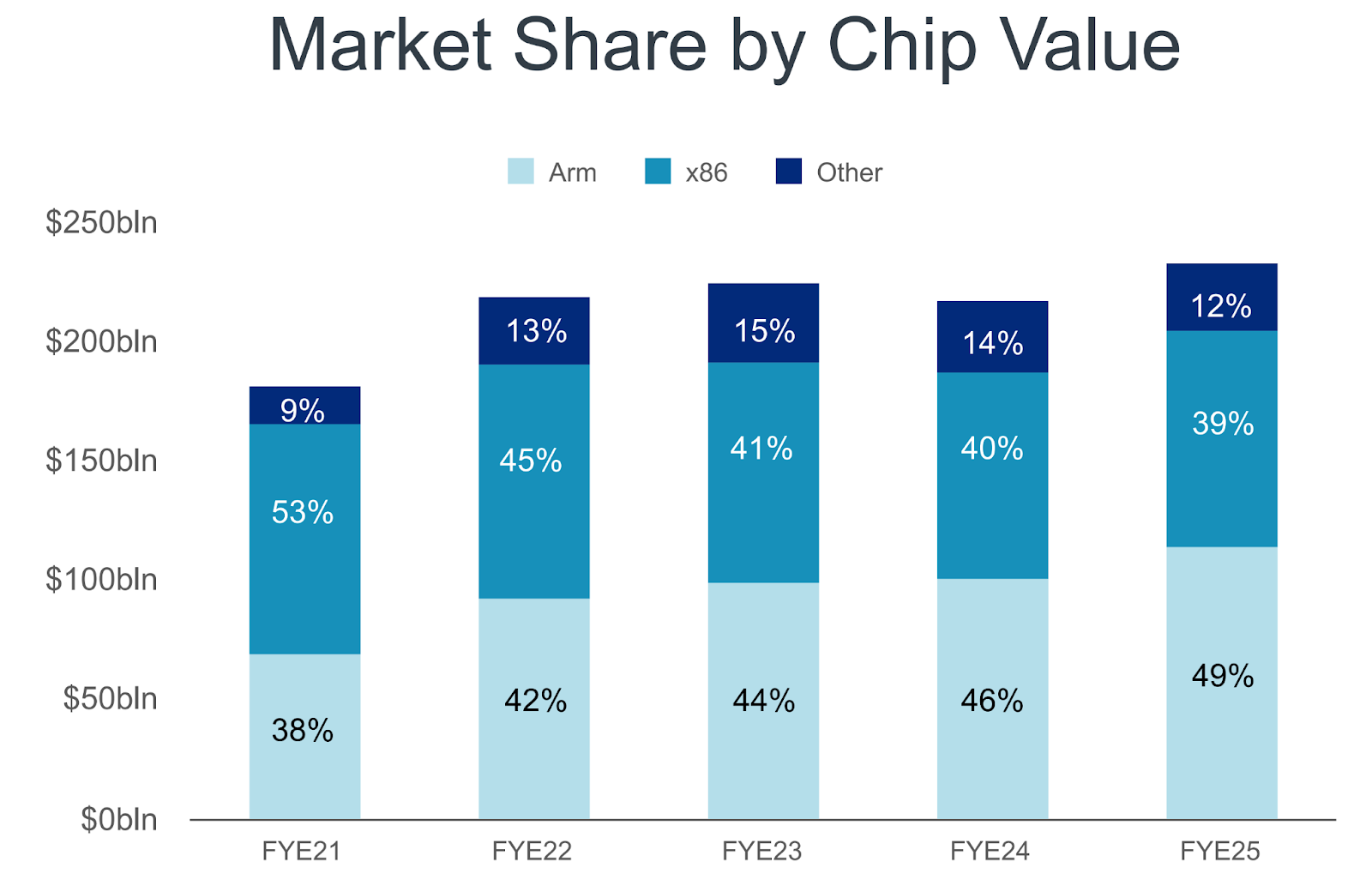

For 35 years, Arm Holdings operated as the semiconductor industry’s silent infrastructure layer. It designed the blueprints - the instruction set architectures and core designs - that other companies built into their chips. Apple’s M-series processors run on Arm. So do Nvidia’s Grace CPUs, Amazon’s Graviton, Google’s Axion and virtually every smartphone processor on the planet. According to Arm’s own Q4 FY2025 results, more than 310 billion Arm-based chips have shipped since 1990, with 30.6 billion shipped in FY2025 alone.

The model worked because Arm competed with nobody. It was the Switzerland of semiconductors - neutral, trusted by everyone precisely because it threatened no one. Apple and Nvidia could both use Arm’s blueprints without ever worrying that Arm would show up as a competitor.

On 24 March 2026, CEO René Haas announced that neutrality was over. Arm launched the AGI CPU - its first physical chip in 35 years of existence. This is not an incremental product announcement. It is a fundamental change in what kind of company Arm is.

To understand why this pivot is significant, you need to understand what the old model was and why it had a ceiling.

Arm’s revenue came from two streams. The first was licensing fees: upfront payments from chip designers - Apple, Qualcomm, Nvidia, Amazon - in exchange for access to Arm’s instruction set and the right to build chips using its designs. These are large, long-term contracts worth hundreds of millions of dollars each.

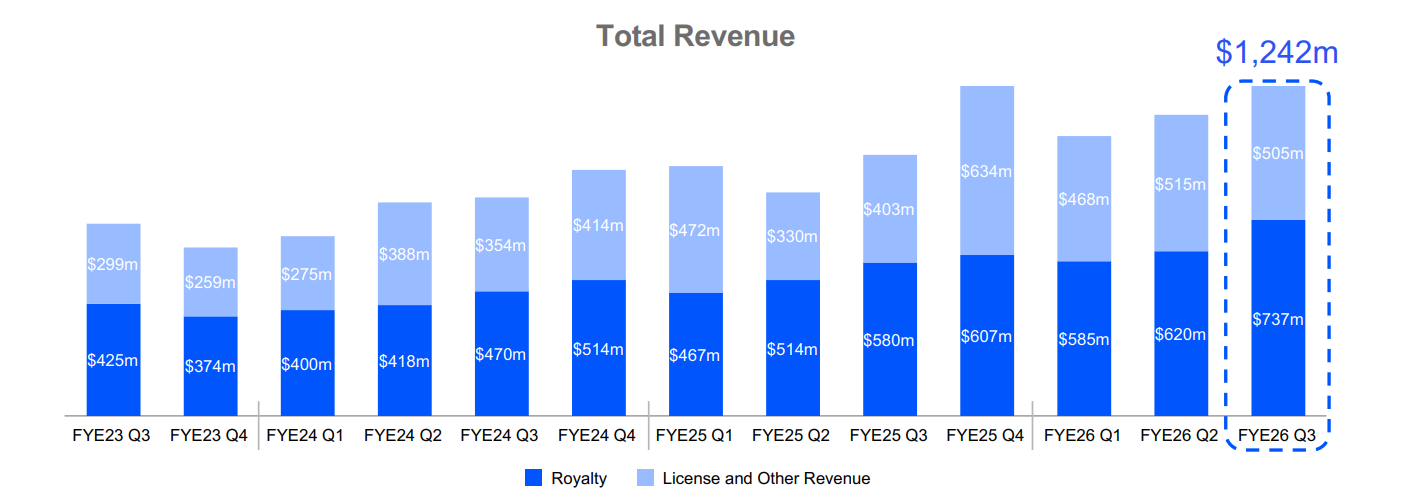

The second was royalties: a small percentage of the selling price collected every time a chip containing Arm technology shipped. Individually modest. Multiplied across billions of chips, compounding over decades, it becomes formidable. In FY2025, royalty revenue reached $2.17 billion, growing 22.7% year-on-year, driven primarily by the shift to the higher-rate Armv9 architecture which commands roughly double the royalty rate of its predecessor. Total company revenue hit $4 billion for the first time, up 25% year-on-year.

Arm’s CFO once described the royalty model as comparable to music: “when an artist has a hit, and that hit goes on for 30 years, you keep getting paid.” Arm’s investor presentation shows it is still collecting royalties on chips designed in the early 1990s. Roughly half of current royalty revenue comes from products launched more than ten years ago.

But the ceiling is structural. Apple charges thousands of dollars for a MacBook Pro built on Arm architecture. Arm collects a few dollars in royalties on the processor inside it. The gap between value created and value captured is the story of Arm’s entire commercial history. The AGI CPU is the attempt to close it.

The catalyst for Arm’s pivot is a structural shift in how AI data centres work specifically, the rise of agentic AI.

The public narrative around AI infrastructure has focused almost entirely on GPUs: the massively parallel processors that train large language models and run inference at scale. Nvidia dominates this market. But GPUs do not operate alone. They need CPUs to orchestrate them - to manage data movement, schedule workloads, handle API requests and coordinate the growing number of AI agents running simultaneously across a data centre.

This orchestration layer is the opportunity. CEO René Haas put the scale of it plainly at the launch: the shift to agentic AI is driving a four-fold increase in CPU demand from 30 million cores per gigawatt of data centre capacity today to 120 million. At that scale, CPU architecture stops being a technical detail and becomes a billion-dollar infrastructure decision.

The x86 architecture - Intel and AMD’s long-dominant standard - was not designed for this. It carries legacy complexity, consumes more power per core and requires larger physical footprints. Arm-based chips have already proven their advantage in cloud deployments: AWS, Google and Microsoft have all built custom Arm processors for their data centres, displacing x86 in new capacity. The AGI CPU takes that thesis and commercialises it directly.

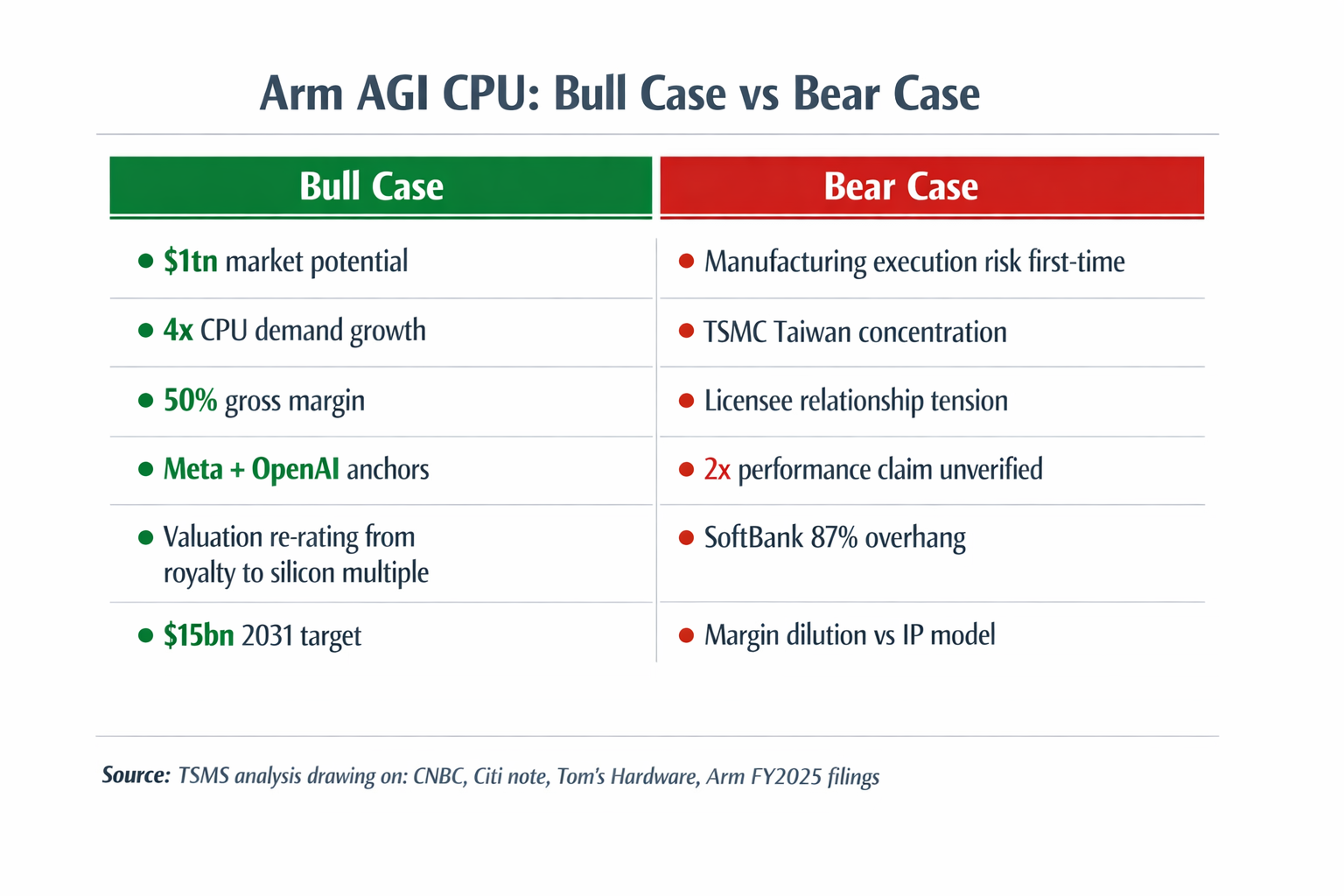

The chip itself: built on TSMC’s 3nm process, up to 136 Neoverse V3 cores, 300W TDP, 6 GB/s memory bandwidth per core at sub-100ns latency, and 96 lanes of PCIe Gen 6 for accelerator connectivity. Arm claims more than 2x performance per rack versus comparable x86 deployments, and up to $10 billion in CapEx savings per gigawatt of data centre capacity. The 2x figure is Arm’s own estimate and has not yet been independently benchmarked - a caveat worth keeping in mind.

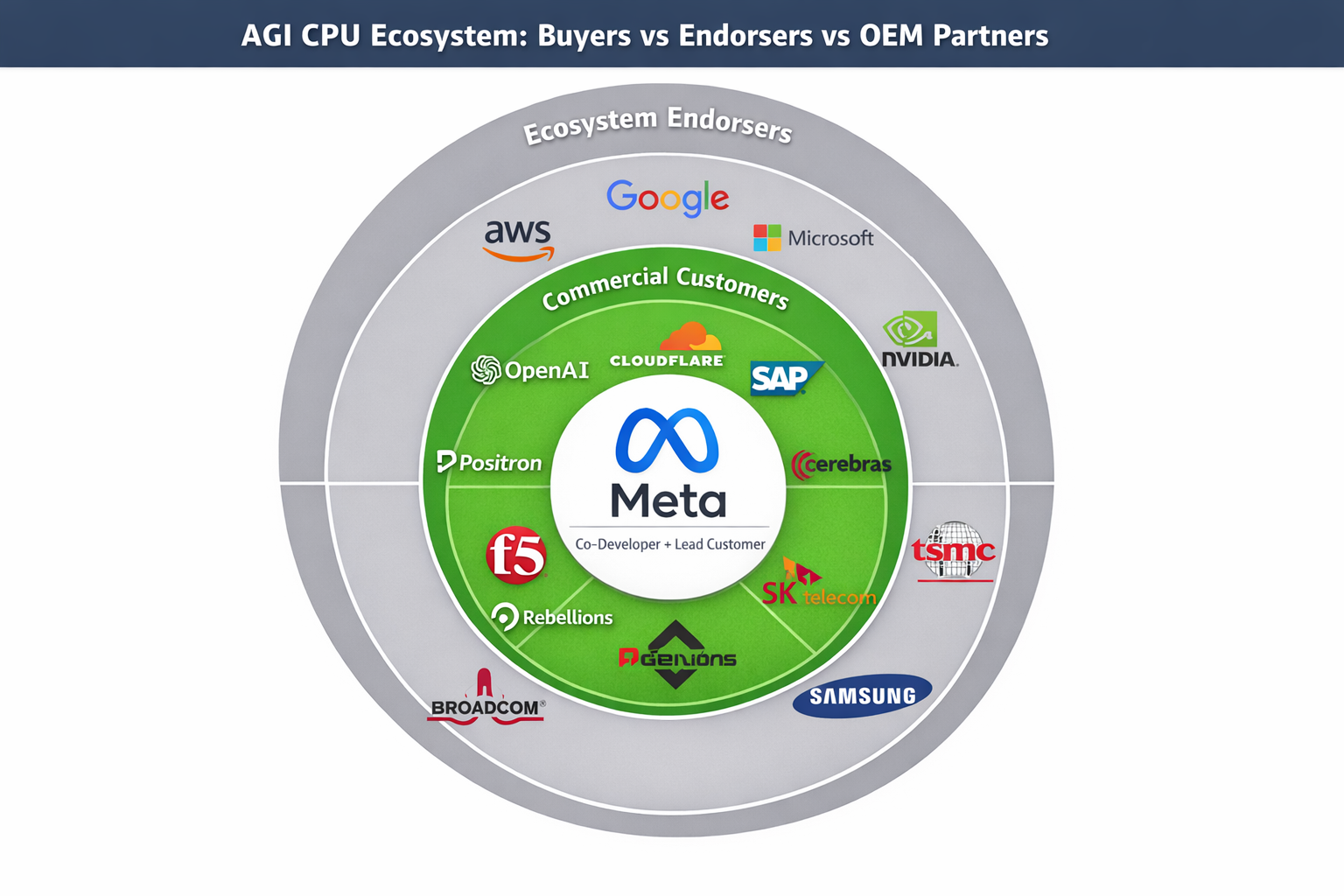

Meta is the lead customer and co-developer. The two companies worked together in Arm’s 1,000-person Austin chip lab for 18 months. Meta’s head of infrastructure Santosh Janardhan described the AGI CPU as a “full replacement, drop-in replacement” for Meta’s existing compute CPUs. The motivation is clear: Meta is committing $135 billion in AI-related capital expenditure in 2026 alone, building gigawatt-scale data centres across Louisiana, Ohio and Indiana. At that scale, 2x performance per rack is not a marginal gain - it is a multi-billion dollar saving.

Beyond Meta, confirmed commercial customers include OpenAI, Cloudflare, SAP, Cerebras, SK Telecom, F5, Positron and Rebellions. OpenAI’s head of industrial compute said the chip would strengthen “the orchestration layer that coordinates large-scale AI workloads” across ChatGPT’s infrastructure, which serves hundreds of millions of users daily.

The more interesting signal is the endorsement list. AWS, Google Cloud, Microsoft Azure, Nvidia, Broadcom, TSMC, Samsung and SK hynix all submitted supportive quotes at the launch. Every one of them is a current Arm licensee. Their public backing is a carefully constructed message: these companies are telling the market they are not threatened. Whether that holds as the AGI CPU roadmap expands into their territory is a different and more important question.

The commercial logic is straightforward. Arm’s CFO said at the launch the chip will be sold at approximately 50% gross margin - a step up from the royalty model, which, despite its elegance, captures only a sliver of the chip’s selling price. CEO Haas projected $15 billion in revenue from the AGI CPU product line alone by 2031, against total company revenue of $25 billion. For context, Arm’s entire revenue in FY2025 was $4 billion. Citi called it “the most significant shift in the company’s history” and noted forecasts were “well above even the highest speculated estimates.” The stock jumped 16% on the day.

The reward is clear. The risk is more subtle but just as real.

Arm’s neutrality was not just a principle - it was the commercial foundation of its licensing business. AWS has invested hundreds of millions building its Graviton CPU line on Arm architecture. Graviton is a key AWS competitive advantage. The AGI CPU does not directly compete with Graviton today - different workload profile. But Arm has confirmed follow-on products are already in development. As the roadmap expands, the overlap will grow. At some point, a licensee paying Arm for IP while watching Arm sell a chip that competes with what they built using that IP will start asking questions about their relationship.

The other structural risk is manufacturing. For 35 years, Arm never had to deal with supply chains, fab capacity, yield rates or hardware delivery timelines. That changes now. The chip is manufactured at TSMC in Taiwan - a geopolitical concentration risk that Arm previously carried only indirectly, through its customers. It now carries it directly.

CEO Haas addressed the competition question by arguing “the market is large enough for everyone” - a $1 trillion AI CPU market with demand growing at 4x current levels. That is probably true in the near term. The medium-term question is less comfortable.

The AGI CPU announcement changes how Arm should be valued and it requires investors to hold two ideas at once.

The first is that this is the right strategic bet. The agentic AI shift is real. The CPU demand it implies is real. The competitive advantage of Arm’s architecture at that workload profile is real, already demonstrated in cloud deployments at AWS, Google and Microsoft before Arm ever shipped a single chip of its own. Meta committing to co-develop the chip and deploy it across gigawatt-scale infrastructure is not PR. It is a multi-billion dollar vote of confidence.

The second is that this is not a risk-free transition. Arm is adding capital intensity, supply chain exposure and a structural tension with its largest licensing customers - all at once. The 50% gross margin on the silicon business is attractive, but it is lower than the near-100% gross margin of the IP licensing model. The $15bn 2031 revenue projection is ambitious enough that missing it materially would be a significant event for the stock.

For a student investor building their market knowledge, the most useful framing is this: Arm has identified the gap between value created and value captured, and it has found a product that closes it. The question is not whether the gap is real - it clearly is. The question is how much damage the closing causes to the ecosystem that made Arm worth closing it.

The stock’s 16% single-day jump reflects the market pricing in the upside before the execution risk is visible. That is usually when the most interesting conversations start.

The Switzerland analogy only stretches so far. Neutrality is a strategy, not an identity. When the most important infrastructure buildout in a generation demands a type of chip that nobody else is optimally positioned to deliver, staying neutral is itself a choice with consequences.

Arm’s leadership looked at the four-fold increase in CPU demand that agentic AI implies and decided the opportunity was too large to service only through other people’s decisions. For 35 years, Arm was the invisible architect of the computing industry - powering everything, credited for little. The AGI CPU is Arm’s decision to become visible.

Whether the companies it spent decades enabling remain comfortable partners or eventually become cautious ones - is the story to watch from here.