The last few weeks have seen some of the biggest blows to the Labour Party. The fall of the Deputy PM by far being one of the most notable. Angela Rayner, at the time Housing Secretary, saw a meteoric exit out of the party when it became known that her tax affairs on a recent £800,000 property purchase in Hove were not in order. Under immense pressure and scrutiny from both the public and political opposition, holding her to the same high standards around tax avoidance she demanded from others, her hand was forced, and her resignation had to be signed.

To many, this seems to have felt like another high-profile tax scandal - something that will fade out of the minds gradually through a bombardment of more energetic or high-profile news cycles. To me however, her exit has really resurfaced some badly covered up cracks in both our political and taxation system. It is a weak point of a government when the person who oversees housing for the country cannot even abide by the right property law and taxation system. It is either an ironic mistake or a deliberate attempt of tax avoidance gone wrong.

Either way, if you need personal legal and tax counsel for a role you drive policy and law around - then the law and taxation system in this country is not at all accessible. This is not new news, and really, everyone should be calling for both: a taxation system that can be understood easily without feeling overwhelmed and having qualified and experienced MPs to lead governmental departments. The latter is somewhat of a technocratic approach, which is not what our democratic system is for, but perhaps an injection of this political style is needed to re-think how we jumpstart a stagnant economy and make the system more fair.

Not to stray into a full-on thought piece, just yet, I think it is important to lay out some facts and context about Angela Rayner’s case before proceeding further.

Angela Rayner’s story is one of graft and toil, one to be admired in fact. Leaving school at 16 while pregnant, she worked as a care worker, later becoming a trade union representative with UNISON before entering the political scene. With her straight-talking, off the cuff style, she gained popularity in her constituency of Ashton-under-Lyne before becoming elected as the Labour MP for the region. She quickly rose through Labour’s ranks, holding key roles including Shadow Education Secretary and Deputy Leader of the Labour Party. Rayner’s key focus has been to champion social mobility, worker’s rights, and educational reform, standing out as one of Labour’s prominent voices.

However, the summer of 2025 saw the unravelling of Manchester’s Red Queen.

The unravelling of the Deputy PM’s tax affairs begins in 2020:

2020:

2023:

Jan 2025

May 2025

28 August 2025

1st September 2025

3rd September 2025

4th September 2025

5th September 2025

Within a period of 1 week, the tax affairs of Angela Rayner had become public and led to her resignation. For Starmer’s Labour government, this was a huge political blow, pressured by opposition and media, culminating in the loss of one of the most prominent working-class voices the party had.

When it comes to property taxes, there are two key charges under current legislation people should be aware of – capital gains tax (CGT) and stamp duty land tax (SDLT). CGT for residential property is typically applied on the disposal of any assets that have appreciated in value and are set at 18% in the UK if you are a basic rate tax payer and 24% if you are a higher rate tax payer (gov.uk) (but only on the part of the gain that falls in each band). CGT is usually exempted if the disposal is of your main residence. This is known as Private Residence Relief (gov.uk) and is applied proportionally to the period of ownership of the primary residence.

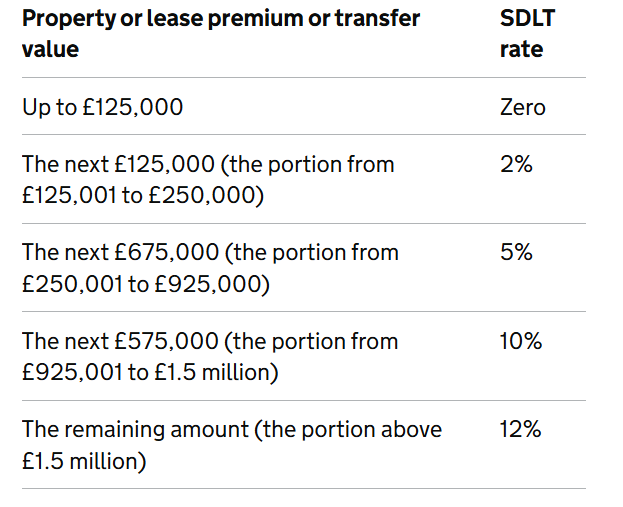

SDLT on the other hand is a tax due when you purchase a new property and is banded based on the property value and levels of property ownership. Figures 1 and 2 show these bands. Typically, second home purchases incur an additional 5% surcharge.

The disposal of the Ashton property to trust in this case would qualify for Private Residency Relief so CGT would not have had to be paid, as it was Angela Rayner’s main residence at that point in time. However, she should have declared to HMRC which new property was deemed to be her main residence for CGT purposes, especially as she continued to live with her children. When it comes to SDLT and with trust law being as complex as it is, the gain of her share by her Child’s trust did not release her from her status as “owner” of the property – especially as it’s a trust for minors below the age of 18. This essential information should have been given to the conveyancing and tax firm that was used. The 5% additional surcharge equates to £40,000 of additional tax. And with late payment costs accruing at an interest rate of 8%, and a “careless” error charge at 30% of the lost tax (HMRC Penalties), she could owe HMRC up to £53,000, which includes the principal sum of tax.

“In this world nothing can be said to be certain, except death and taxes,” wrote Benjamin Franklin. Yet why must tax - the one certainty we can influence - be so complex? Angela Rayner’s case demonstrates how even straightforward rules can become opaque when personal circumstances and family structures intersect with a complicated system. The guidance exists, but only for those willing or able to pay for specialist advice or to sift through HMRC’s dense manuals, which few non-experts realistically do.

In an age of AI and open data, governments should treat tax literacy as a policy priority. Democratising tax education strengthens economic freedom. When all citizens understand the rules governing saving, investment, and entrepreneurship, financial decision-making is no longer the preserve of the wealthy or well-advised. Policymakers could, for example, integrate basic tax education into secondary curricula, develop clear digital tools to simulate tax outcomes, and simplify reliefs to reduce reliance on costly advisers.

Broader tax efficiency among households may initially reduce receipts, but over time it can stimulate growth, improve capital allocation, and broaden the tax base as spending and investment rise. A policy framework that balances revenue stability with economic freedom (transparent rules, accessible guidance, and predictable reliefs) can create a fairer market environment and a more resilient economy. And create a bit more political stability!