More recently, however, there are indications that this long-standing narrative may be shifting. Rather than attempting to replicate the consumer-platform growth models that have dominated American technology expansion, Europe’s renewed momentum has emerged in capital-intensive and strategically significant industries. These include semiconductors, artificial intelligence infrastructure, advanced manufacturing, and defence-linked technologies. This evolution suggests a structural recalibration in how private investment and policy priorities are aligned across the region.

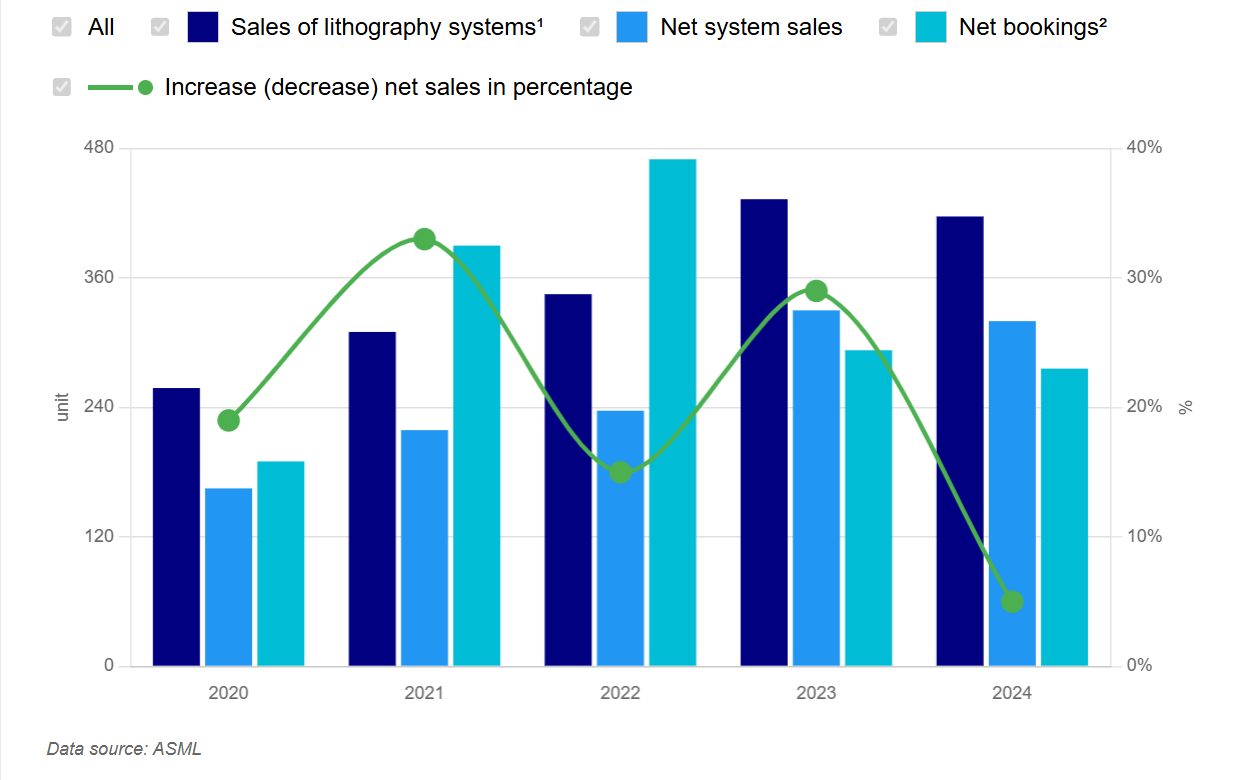

ASML Holding (NASDAQ: ASML) occupies a central position in this transformation. As the sole global supplier of extreme ultraviolet (EUV) lithography systems, the Dutch semiconductor equipment manufacturer plays a decisive role in the production of advanced chips. Its position provides a useful lens through which Europe’s emerging technology revival can be assessed.

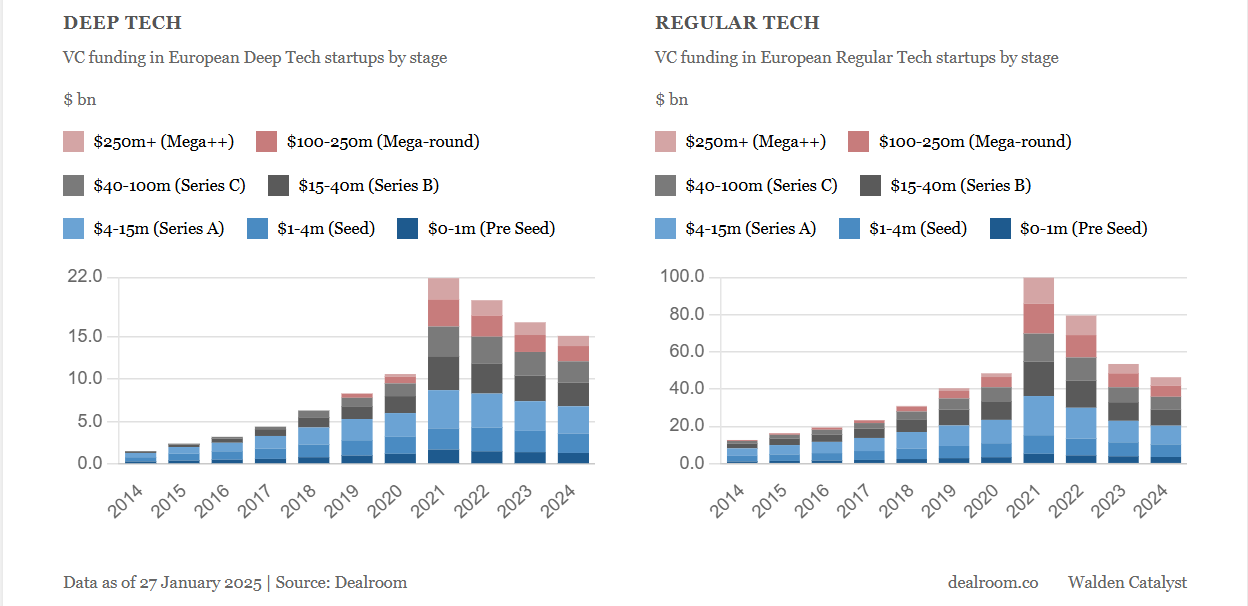

The changing nature of technology investment in Europe is best understood as a reallocation of capital toward specialised technologies rather than a simple revival of overall funding levels. While total venture capital raised in Europe has yet to return to the peak levels seen in the early 2020s, the distribution of that capital has shifted meaningfully.

According to Atomico’s State of European Tech 2025 report, 36% of European venture capital dollars flowed into deep tech companies, up from just 19% in 2021. This deep tech category includes hardware, semiconductor design, AI infrastructure, quantum technologies, and industrial software — areas that are inherently capital‑intensive and characterised by higher technical barriers to entry.

Moreover, Europe sustained approximately $44bn in total technology investment in 2025, an amount that compares favourably with prior years and signals stability in capital allocation despite global macro pressures.

This reallocation reflects a structural preference for firms with durable intellectual property and long‑term strategic relevance. Unlike sectors defined by consumer engagement metrics and short product cycles, capital‑intensive technologies promise defensibility and alignment with national economic imperatives.

European policy responses have broadly aligned with this market shift. Rather than primarily promoting platform competition or digital services, policymakers have focused on industrial strengths and capacity building in sectors seen as material to economic sovereignty. The European Chips Act and expanded public funding mechanisms represent a recognition that market forces alone may not generate sufficient capacity in strategically important technologies.

While the Chips Act has been critiqued for its narrow focus on advanced fabrication facilities, industry groups have called for a broader approach encompassing equipment, materials, and design ecosystems. According to Reuters, SEMI Europe — representing hundreds of European semiconductor firms — has urged the European Commission to revise the policy framework (so-called “Chips Act 2.0”) to support these wider segments and close the competitive gap with the United States and Asia.

This policy evolution suggests that Europe’s strategy is not purely reactive but structural and forward-looking, designed to anchor production, intellectual property, and supply chains in critical domains. Nevertheless, challenges in implementation, including fragmented regulation and slower permitting processes, underline that policy alignment has not eliminated structural constraints.

Founded in 1984 as a joint venture between Philips and ASM International, ASML’s ascent from niche supplier to global strategic linchpin was neither rapid nor assured. Much of the company’s competitive advantage stems from its investment in extreme ultraviolet (EUV) lithography, a technology once dismissed by many in the industry as economically impractical.

Today, ASML is the sole commercial supplier of EUV lithography systems, machines that are essential for manufacturing chips at the most advanced process nodes. These tools, which can cost in excess of €150 million each, are required to produce semiconductors at scales and densities demanded by leading-edge logic and memory applications. As a result, no competitor has matched ASML’s capability at scale.

ASML’s importance is underscored by its customer base, which includes global leaders such as TSMC, Samsung, and Intel, all of which depend on EUV systems for cutting‑edge fabrication. Without ASML’s machines, the ability to produce chips at the most advanced nodes would not be commercially feasible with current technologies.

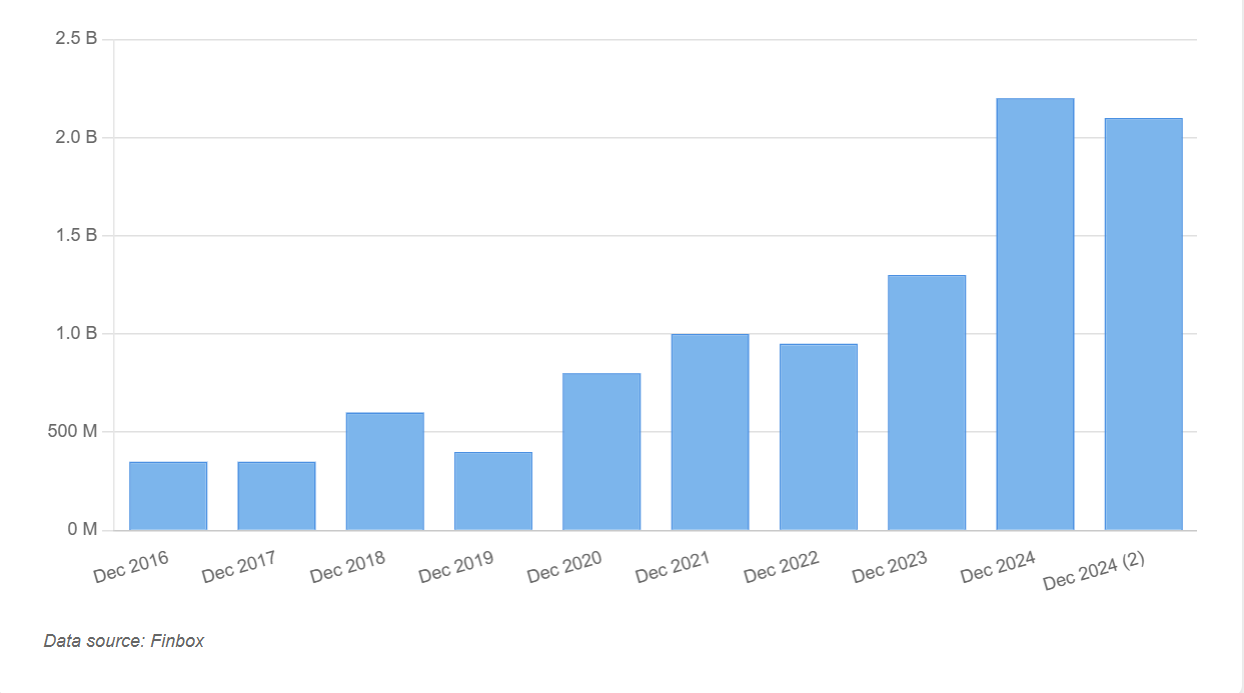

ASML’s financial trajectory reflects its structural role. The company has delivered consistent revenue growth over the past decade, supported by sustained capital expenditure commitments from major semiconductor manufacturers. Forward guidance from ASML’s investor communications projects potential revenue growth into the mid‑decade driven by EUV technology and the expanding role of artificial intelligence across the industry. These projections estimate annual revenue between €44 billion and €60 billion by 2030, with continued double‑digit spending growth in advanced logic and DRAM segments.

One of the most notable features of ASML’s business model is its long order backlog, which offers multi‑year visibility into future demand and mitigates short‑term cyclicality. Unlike more consumer‑dependent segments of the technology sector, ASML’s demand correlates with strategic capital investment cycles in semiconductor fabrication, a dynamic that aligns the company’s performance more with macro‑industrial spending than with quarterly product trends.

ASML’s prominence has also placed it at the intersection of geopolitical competition. Export controls imposed by the United States and allied governments have restricted the company’s ability to sell its most advanced EUV systems to certain markets, particularly China, unless strict export licenses are secured. These controls form part of a strategic effort to limit the spread of leading technology capacity to geopolitical rivals, and they reflect how industrial technology has become integrated into broader foreign policy frameworks. At the same time, these restrictions illustrate a broader structural reality: no region is entirely independent in semiconductor technology. Europe’s strength in advanced equipment coexists with weaknesses in high‑volume chip fabrication, a segment dominated by Taiwanese and South Korean firms such as TSMC and Samsung, increasingly supported by state subsidies in the United States under the CHIPS Act and related initiatives. As a result, Europe’s technology revival remains interdependent on global alliances, particularly with the United States, even as it seeks to build sovereign capacity where feasible.

Reflecting this strategic reorientation, ASML has pursued alliances that extend beyond its core equipment business. Notably, ASML led a €1.7 billion funding round in French AI startup Mistral AI, investing approximately €1.3 billion and becoming its largest shareholder. This move represents a deliberate alignment between advanced industrial capability and frontier AI development — an effort to foster a European‑centric technology stack and reduce reliance on U.S. platforms.

The strategic intent here resembles broader ecosystem ambitions. According to the Atomico State of European Tech data, large strategic funding rounds in European deep tech are contributing to an expanding innovation base oriented toward infrastructure and systems rather than solely consumer applications.

ASML’s success has generated tangible spillovers across the European technology ecosystem. The company anchors a dense supply chain of highly specialised component makers, research collaborations, and engineering partnerships, especially in the Netherlands and Germany. These linkages help attract talent, deepen industrial expertise, and reinforce Europe’s comparative advantages in precision engineering and advanced manufacturing.

Investor sentiment has also shifted. The validation of Europe’s ability to produce a world‑class industrial technology has catalysed increased allocation to infrastructure‑oriented startups and technology platforms. Institutional capital, including pension funds and long‑horizon investment vehicles, has shown greater willingness to consider European technology as a source of durable value creation rather than purely speculative growth. This momentum is reflected not only at the equipment level but also in emerging downstream industries and adjacent technologies that rely on semiconductor supply chains.

Despite these positive developments, it would be misleading to interpret ASML’s success as evidence that Europe’s technology challenges have been fully resolved. The company remains an outlier in a landscape where many technology segments still face significant barriers to scaling. Persistent issues include fragmentation of markets across national borders, slower access to late‑stage capital relative to Silicon Valley, regulatory complexity that can impede rapid product rollout, and talent mobility constraints. These factors continue to temper Europe’s ability to generate large platform or infrastructure firms outside of specialised niches.

In addition, Europe’s share of global semiconductor production (approximately 10%) remains low relative to ambitions articulated in policy frameworks. Industry voices and independent auditors alike have questioned whether current policy targets are achievable without more decisive scaling initiatives.

Europe’s technology revival is best characterised not by sudden exuberance or headline valuations but by structural recalibration, deeper industrial orientation, and strategic policy alignment. The continent’s recent progress reflects a deliberate shift toward technologies that are foundational to future economic resilience and global competitiveness.

At the forefront of this revolution, ASML’s dominance in EUV lithography demonstrates Europe’s capacity to anchor global industrial value chains where technological depth meets sustained investment. While constraints remain and structural dependencies persist, the region’s focus on strategic industrial capability suggests a more sustainable trajectory for long‑term technological relevance. Hence, if these orientations are extended across complementary technologies and supported by calibrated policy and funding mechanisms, Europe’s role in shaping the global technology landscape may continue to strengthen over the decade ahead.